Has it been the bankruptcy of the Sillicon Valley Bank he nuevo “Lehman Brothers”? Are we at the gates of a new financial crisis? What will happen to interest rates? Will we see drastic drops in the price of money again? There are many questions that arise after the financial earthquake that has shaken the markets since the Silicon Valley Bank declared bankruptcy just under two weeks ago.

The first thing to say is that the trigger, the symptoms, the disease and the treatment of the 2008 crisis that unleashed the bankruptcy of Lehman Brothers does not have much to do with what is happening these days. Although the essence is the same: at that time it was necessary to drain the excesses that caused lax interest rate policies and now it seems that the same thing is happening: that a crisis is called to drain the excesses of more than a decade, no longer of low rates. , but from a monetary experiment that has brought the price of money to rates 0 for years.

At that time the excess was committed above all in private mortgages. The famous subprime, a credit bubble that he burst when Lehman Brothers burst. On the other hand, the situation in 2008 hardly resembled the one we live in today. At that time we were coming from an expansive period of economic exuberance that made economic agents think that economic crises were a thing of the past.

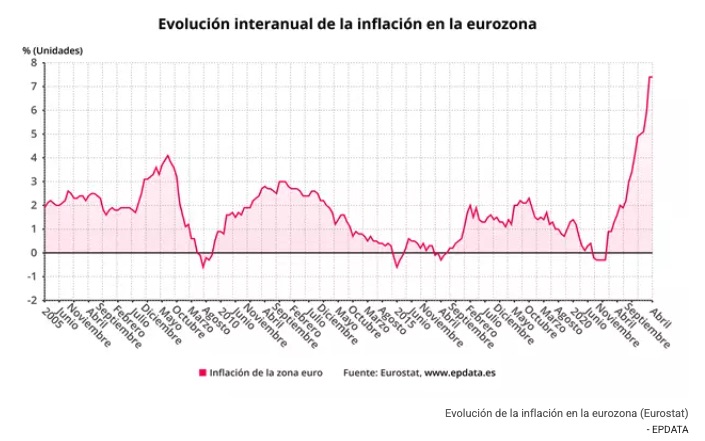

Excesses are paid for and many have been committed in the last decade. “I don’t know how this monetary experiment is going to end,” some market analysts said in conversation with Libre Mercado in 2019, when we added almost 10 years with rates close to 0%. “We enter the terrain of the unknown“, they said. However, the years passed and the fearsome inflation that everyone feared was not unleashed. Finally, the supply crisis that caused the collapse of the coronavirus in 2019 ended up catalyzing inflation… and the leviathan is enormous. So much so that it has We have caused the fastest rise in interest rates in living memory, and we have also suffered the biggest rise in inflation in 40 years.

Interest rates and financial stress

And it is precisely this rapid rise in interest rates that is causing strong tensions in the financial markets. But, Does raising interest rates by itself slow down inflation? No. What causes the rise in interest rates is the sudden increase in the cost of money and financing, which slows down consumption and investment. The economy “freezes” Demand slows down with respect to supply and causes prices to moderate.

This is the theory. Therefore, the rise in rates seeks to slow down the economy, seeks recession and crisis. What it basically does is withdraw the money that is left over and that has been injected into the economy: it “drains” that excess.

The rise in interest rates and its effect on inflation

But what we are seeing is a rapid rise in interest rates with zero interest due to the arrival of the recession. Interest rates rise, in the US and in Europe, but in Europe, while they rise, at a slower pace than in the US, Liquidity continues to be injected into peripheral economies such as Hispaniola through the approval of the famous Next Generation aid plans and the purchase of debt by the ECB. Therefore, consumption does not stopand the economy continues to grow forcing central banks to continue tightening their rate hike policies.

The storm that is plaguing banks these days, with the disasters at Silicon Valley Bank and Credit Suisse, has to do with the rise in interest rates and the gigantic bubble that has fueled the zero-rate monetary experiment: public debt.

The origin of the liquidity problems of these banks has to do with the effect of the rise in interest rates on long-term debt securities. An effect that caused the fall in fixed income in 2022 and that threatens to do the same in 2023. And the problem is that in the last 10 years the public debt of the US and Europe has flooded the markets and the balance sheets of the banks. Let us remember that the new regulation that was born after the Lehman Brothers crisis rewarded banks with lower provisioning requirements if they bought public debt securities. And boy did they.

So, just like in 2008, we have an identified problem: in 2008 they were mortgages that were not going to be paid. In 2023 we have public debt. The difference with 2008 is that if this debt is brought to maturity, that loss is not such. The return of these investments in the long term is known. However, currently, those titles in the market are worth less and less and the banks have real problems if they are forced to sell that debt to face liquidity tensions, because then the losses become effective.

Let’s imagine a family that bought a house at the height of the urban bubble for 500,000 euros and that in 2010 its market price was 200,000. If the family did not need to sell it, their situation hardly changed. He kept her waiting for her to recover her courage sooner or later. However, if the family became unemployed in 2010 and was forced to sell the house to face the liquidity tensions they had due to the lack of work, then the losses materialized and their liquidity problems became problems of solvency.

The big problem: the public debt bubble

Let’s change family for financial system, let’s change mortgages for long-term fixed income securities and Let’s change mortgages and houses for public debt.

There are many economists who, like Nouriel Roubini, have been warning in recent years of a major public debt problem. A debt that not only fills the balance sheets of the banks in the long term, but currently serves as a guarantee or collateral for countless financial products. It is the great bubble that could burst in the midst of the current financial storm.

Will a public debt bubble burst? When? With what consequences? Time will tell. But one thing seems clear: regardless of the effects caused by rate hikes, the desired one, which is to curb inflation, is not taking place. And that, inflation, is, let us not forget, the great concern, the disease that can bring down an economy.