US Inflation Expected to Continue Slowing, Paving the Way for Potential Rate Cuts

Bloomberg – The pulse of US inflation likely continued to slow at the start of the year, helping to feed expectations that the Federal Reserve will find interest-rate cuts more palatable in the coming months.

Continued Slowing of Inflation

The core consumer price index, a measure that excludes food and fuel for a better picture of underlying inflation, is seen increasing 3.7% in January from a year earlier. This would mark the smallest year-over-year advance since April 2021, underscoring the inroads Fed Chair Jerome Powell and his colleagues have made in beating back inflation. Economists forecast Tuesday’s report would show that the overall Consumer Price Index (CPI) probably rose less than 3% for the first time in nearly two years.

While progress in beating back inflation has been acknowledged, policymakers have been cool to the idea of reducing rates in the near future, rooted in an economy that’s displaying positive indicators, predominantly in the labor market. Durable employment growth has been supporting consumer spending, and an anticipated separate report on retail sales is expected to show another increase, excluding motor vehicles and gasoline.

The cooling of inflation, along with the expectations of lower borrowing costs this year, have contributed to an improvement in consumer confidence as well. A University of Michigan survey, forecasted to be released on Friday, is expected to show an index of sentiment holding near its highest level since July 2021.

Investors will closely monitor Fed officials speaking in the days following the CPI data, aiming to gauge the timing of any potential rate cuts. Among those scheduled to speak are regional bank presidents Raphael Bostic of Atlanta and Mary Daly of San Francisco, who both play a significant role in shaping policy decisions this year.

Global Highlights for the Week

Asia

Japan’s economy is expected to rebound after a dismal performance over the summer, signaling the Bank of Japan’s potential end to its negative rate policy. Figures released on Thursday are also expected to confirm that Japan has slipped to the fourth-largest economy in the world, falling behind the US, China, and Germany.

China’s markets will be closed for Lunar New Year celebrations, and no major releases are scheduled.

Reserve Bank of India Governor Shaktikanta Das, who maintained a hawkish stance at the rate meeting on Thursday, may witness progress in the fight against inflation at the start of the week, with consumer prices expected to have grown at a slower pace in January. However, it may not be slow enough to prompt discussions of a policy pivot.

The Philippine central bank is anticipated to hold rates steady on Thursday, with prices continuing to weaken.

Australian jobs figures earlier in the day are expected to show a return to growth after the losses in December.

Singapore will revise its gross domestic product figures ahead of trade data the following day.

RBNZ Governor Adrian Orr will present his latest position on policy and 2% inflation in a speech on Friday morning, with the week concluding with the release of Malaysian GDP numbers.

Europe, Middle East, Africa

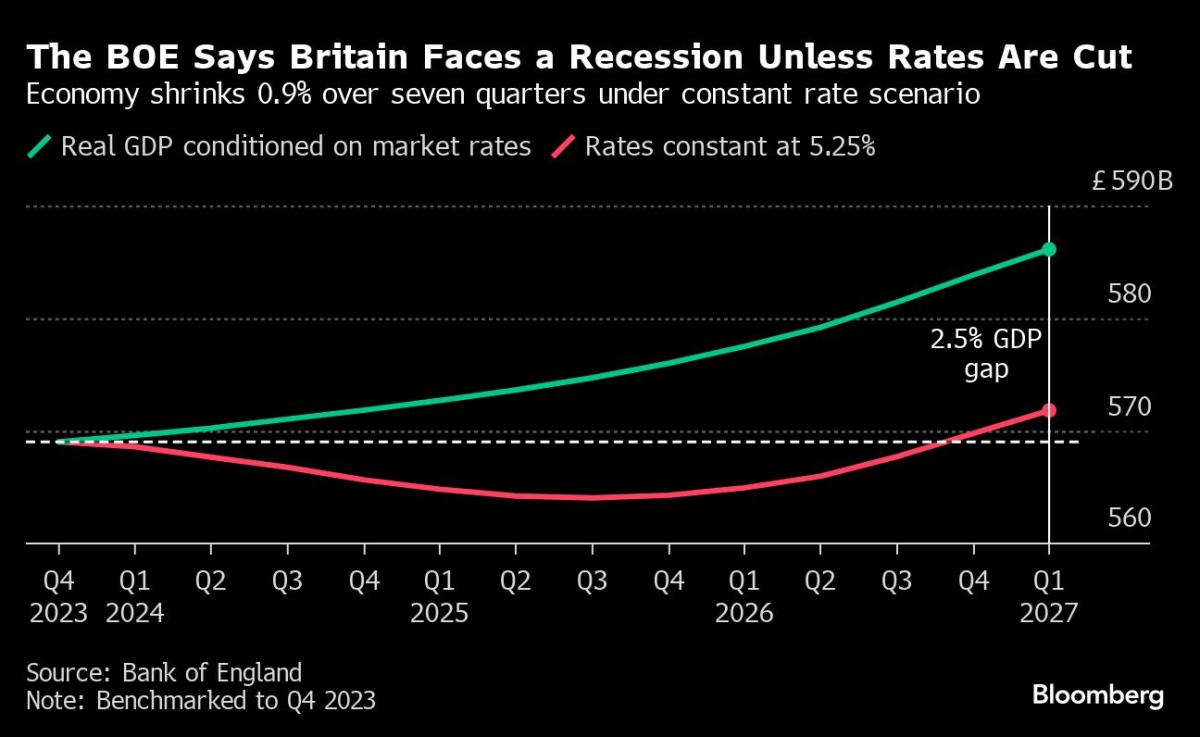

UK data will take the limelight this week. Wage numbers on Tuesday may indicate the weakest pay pressures since 2022, which would serve as good news for Bank of England officials who are increasingly considering rate cuts.

An anticipated blip higher in inflation on the headline gauge, as well as the core measure that excludes volatile elements such as energy, will be scrutinized in the data released on Wednesday.

Additionally, GDP numbers on the following day will provide insights into the impact of BOE tightening on growth. Economists believe the UK economy stagnated in the fourth quarter, narrowly avoiding a recession.

Januaray inflation data will be released in the wider region as well:

- Swiss consumer-price growth is expected to have slowed to 1.6%, while Denmark will release equivalent numbers.

- In Eastern Europe, inflation is anticipated to have weakened significantly in Poland and the Czech Republic, while edging higher in Romania.

- In Ghana, the rate is likely to have eased from 23.2% a month earlier, while Nigeria’s reading may have accelerated from 28.9% amid currency weakness.

- In Israel, inflation is expected to have slowed to 2.7%.

Fourth-quarter GDP numbers in Eastern European economies and Norway are expected to remain subdued.

In the euro-zone, industrial production on Thursday will likely show a fourth monthly drop in December amid falling factory output in economies including Germany.

Multiple events featuring European Central Bank officials are scheduled throughout the week, including President Christine Lagarde’s testimony to lawmakers on Thursday. Speaking this weekend, ECB Governing Council member Fabio Panetta suggested that “the time for reversal of the monetary policy stance is fast approaching” and issued a warning against waiting for too long on rate cuts.

In Norway, Governor Ida Wolden Bache will deliver her annual address to Norges Bank’s supervisory council.

Rate decisions are expected in Romania, where the central bank will likely keep the rate at 7% while investors look for clues on potential future cuts. Zambian officials, on the other hand, are expected to raise borrowing costs to support a battered currency and curb mounting price pressures. Namibia’s policymakers are likely to leave borrowing costs unchanged, following South Africa’s decision to pause rate changes. The Bank of Russia, meanwhile, is likely to remain on hold, as Governor Elvira Nabiullina indicated in December that the key rate will remain elevated to tackle high inflation.

Latin America

Argentina will post its January inflation report as the country returns from the Carnival holiday. Economists anticipate a month-on-month rise of 21.9% in consumer prices, down from 25% in December, but with an expected annual rate of over 250%, higher than the 211% rate at the end of 2023. President Javier Milei’s devaluation of the peso and elimination of price controls on consumer products has led to an inflation surge.

In Colombia, a range of negative data is expected, indicating a significant slowdown in the post-pandemic period. Industrial output, manufacturing, and retail sales have all been negative since March, and the fourth-quarter output is projected to have contracted. Full-year GDP growth is expected to be slightly over 1%, a significant decline from the 2021 and 2022 figures of 11% and 7.5%, respectively.

Brazil will release December GDP-proxy figures, preceding the quarterly and full-year report scheduled for March 1. Peru will publish December economic activity data and January unemployment for its capital city, Lima.

Finally, Chile’s central bank will release the minutes of its January decision to implement a 100 basis-point cut, lowering the rate to 7.25%. Economists surveyed by the central bank predict that the rate will reach 4.75% by the end of the year, with inflation returning to 3%.