Money Today Reporter Hwang Ye-rim | 2023.12.25 06:48

/Photo = Design Reporter Lee Ji-hye This year, as the funding situation worsened due to high interest rates, the maturity structure of bonds issued by capital companies appeared to have become shorter. Bonds maturing within the next six months alone amount to 26 trillion won. In the fourth quarter of this year, the capital company raised over 1 trillion won with a maturity of less than one year.

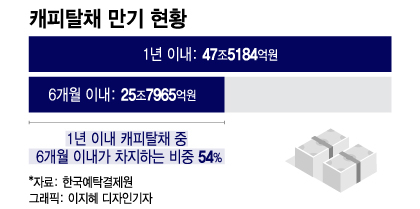

According to the Korea Securities Depository on the 22nd, the balance of capital bonds maturing within June of next year is 25.7965 trillion won. The balance of capital bonds with one year remaining to maturity is 47.5184 trillion won, of which 54% will mature within the next six months. At the end of last year, the proportion of bonds maturing within six months among bonds with one year remaining to maturity was around 45%. The proportion of short-term bonds increased rapidly in the past year.

When 26 trillion won worth of loans mature in June next year, the interest burden on capital companies is expected to increase. Capital companies do not have a receiving (deposit) function, so their funding options are limited. As a result, when the existing bonds mature, new bonds are issued to repay the existing bonds. Among the bonds that are nearing maturity, many were issued when interest rates were relatively low, so the interest burden may increase if new bonds are raised in the future.

The simple average interest rate of capital bonds with 6 months left until maturity is 3.30%. On the other hand, as of the 22nd, the average 1-year interest rate for credit grade A+ specialized credit bonds (still bonds) is 4.93%, and the average 1-year interest rate for credit rating AA- is 4.06%. In order to repay bonds with interest rates in the 3% range, new money must be borrowed at an interest rate close to 5%.

The burden of procurement for capital companies is expected to continue for the time being. Capital companies continued to issue short-term bonds after the second half of this year. In the fourth quarter of this year, the balance of bonds issued by capital companies with a maturity of less than one year amounted to 1.02 trillion won. The simple average interest rate amounts to 5.24%.

The reason why capital companies have no choice but to raise funds in the short term is because the demand for capital bonds is decreasing. From the perspective of purchasing bonds, they believe that the longer the maturity, the greater the risk, so they prefer short-term bonds if the interest rates are similar. The gap between short- and long-term capital bond interest rates is gradually narrowing. As of the 22nd, the average interest rate for 5-year credit rating AA- capital bonds was 4.34%, and the gap with the 1-year bond was only 0.28 percentage points (p). In early 2021, when market conditions were favorable, this gap was 0.84%p.

Concerns about insolvency due to real estate PF (project financing) loans are also growing. According to the Financial Services Commission, the balance of real estate PF loans from domestic financial companies at the end of September was 134 trillion won. Among these, the real estate PF balance of capital companies is 26 trillion won, accounting for 19% of the total. NICE Credit Rating analyzed that at the end of September this year, the subordinated proportion of real estate PF bridge loans of capital companies was 30% of the total, which was about three times higher than the subordinated proportion of savings banks (11%). When issuing a real estate PF loan, there is a high possibility that both principal and interest will be covered if you take the senior position, but a loss of principal is inevitable for junior creditors.

Jeon Se-wan, senior analyst at Korea Credit Rating, said about capital companies’ outlook for next year, “Demand for capital bonds is decreasing as concerns about the deterioration of soundness are emerging, especially in real estate finance.” He added, “In the process of refinancing the bonds raised from 2020 to last year, “There is a burden of high interest rates,” he said.

[저작권자 @머니투데이, 무단전재 및 재배포 금지]