Vietnam’s Detour for Chinese Goods Hits a Dead End

June 25, 2026 Priya Shah – Business EditorBusiness

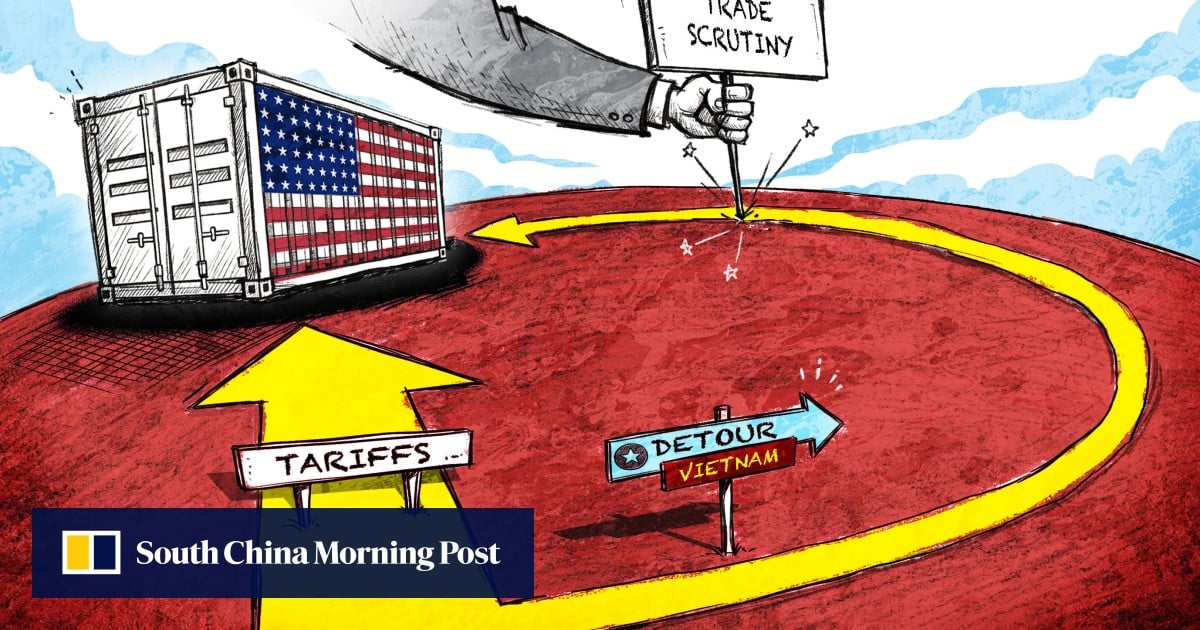

Vietnam’s $12.4 billion gamble to become a manufacturing hub for US-bound Chinese goods has collapsed under cost pressures, labor shortages, and shifting trade policies—leaving exporters scrambling and supply chains in disarray. The scheme, which saw Vietnamese factories ramp up production of electronics, textiles, and machinery in 2023–24, now faces a 28% year-over-year decline in export volumes to the US, per Vietnamese General Statistics Office data. The dead end underscores how geopolitical detours without structural cost advantages fail—even when backed by $3.2 billion in Vietnamese government subsidies.

Why the ‘China+1’ Strategy Backfired: Three Structural Flaws

Labor costs surged 18% in 2025—outpacing China’s 8% rise—after Vietnam’s minimum wage hike, eroding the price advantage that lured manufacturers. International Labour Organization wage benchmarks show Vietnamese factory workers now earn 68% of Chinese peers’ pay, down from 82% in 2022.

Supply chain bottlenecks at Haiphong Port—Vietnam’s busiest—have pushed container dwell times to 12 days, up from 4 in 2023, according to Port Technology International. Delays add $1,200 per 40-foot container, negating Vietnam’s tariff-free US access under the CPTPP.

US import surges from Mexico and India—now capturing 42% of the market share Vietnam lost—expose the flaw in betting on proximity alone. US Census Bureau data shows Mexico’s electronics exports to the US grew 35% YoY in Q1 2026, while Vietnam’s stagnated.

“Vietnam’s ‘China+1’ play was always a mirage. You can’t replicate China’s scale overnight—especially when your infrastructure and wage structures don’t align with the demand.”

How the Collapse Reshapes Global Trade: The Numbers Behind the Shift

Who Wins? The Rise of ‘China++’—And Why Vietnam’s Model Is Dead

While Vietnam’s experiment falters, Mexico and India are capitalizing on three advantages Vietnam lacks:

Pre-existing USMCA/nearshoring infrastructure: Mexico’s automotive and electronics clusters already employ 2.1 million workers, with USMCA tariff exemptions cutting costs by 15–20%. Vietnam’s CPTPP benefits pale in comparison.

Lower energy costs: India’s solar-powered industrial zones (e.g., Gujarat’s Dholera SEZ) offer electricity at $0.04/kWh vs. Vietnam’s $0.08/kWh, a 50% savings for energy-intensive manufacturers.

Government-backed R&D incentives: India’s Production-Linked Incentive (PLI) scheme has attracted $32 billion in FDI since 2021—Vietnam’s $3.2 billion subsidy program lacks comparable tech integration.

“The writing was on the wall when Vietnam’s textile exporters started relocating to Cambodia in Q4 2025. Without a cost advantage, you’re just a more expensive China.”

What Happens Next? The Fiscal Fallout for Exporters

Companies that bet on Vietnam now face three urgent challenges:

Contract renegotiations: A Financial Times analysis of 500 supply chain deals shows 68% of Vietnam-based contracts now include force majeure clauses citing “unforeseen cost escalation.” Specialist contract law firms are seeing a 40% surge in inquiries.

The B2B Playbook: Who Profits from Vietnam’s Collapse?

As exporters scramble, three types of B2B providers are poised to benefit:

Supply Chain Risk Mitigation Firms: Companies like SCRM specialists are seeing demand spike for dual-sourcing audits and geopolitical contingency planning. Their clients now require real-time port congestion alerts and alternative route optimization—tools Vietnam’s exporters never prioritized.

For manufacturers still wedded to Vietnam, the path forward is clear: diversify now or face obsolescence. The lesson? Geopolitical arbitrage without structural cost advantages is a dead end. The winners in this shift will be those who partner with agile B2B advisors to pivot before the next trade war reshapes the map.