Credit Score Landscape: A State-by-State Look and Emerging Challenges

American credit scores remained remarkably stable in 2024, averaging 715 according to experian data. however, recent shifts in reporting practices and the increasing popularity of “Buy Now, Pay Later” (BNPL) services are poised to introduce new pressures on creditworthiness in the coming months.

credit scores are a critical factor in financial life, utilized by banks, landlords, credit card issuers, employers, and utility providers to gauge an individual’s likelihood of timely payments. A strong credit score typically unlocks favorable loan terms and lower interest rates, while a weaker score can restrict access to credit.

Several key developments are impacting the credit score environment. FICO, a major credit scoring provider, has begun incorporating data from Buy Now, Pay Later (BNPL) plans into its scoring system. BNPL allows consumers to spread purchases into interest-free installments, provided payments are made on schedule. While offering convenience, financial experts caution that managing multiple BNPL plans requires careful tracking to avoid overspending and accumulating debt.

Furthermore, reporting of federal student loan data resumed after a multi-year pause implemented during the COVID-19 pandemic.Payments were suspended for several years, and missed payments were generally not reported to credit bureaus during this period. The reporting “on-ramp” period concluded in October 2024,leading to newly missed payments and delinquencies impacting credit scores once again.

By February 2025, these changes contributed to the average FICO score holding steady around 715, but with critically important individual variations. data from the Federal Reserve Bank of New York revealed that over two million borrowers experienced credit score drops of 100 points or more in the first quarter of 2025, and more then one million saw declines of 150 points or more. borrowers with initially higher scores were often most affected, though those with lower scores also experienced decreases.

FICO reported that the percentage of the population with a delinquency of 90 days or more in the past six months increased from 7.4 percent in January 2025 to 8.3 percent in February 2025 – a 12 percent rise – directly following the resumption of student loan delinquency reporting.

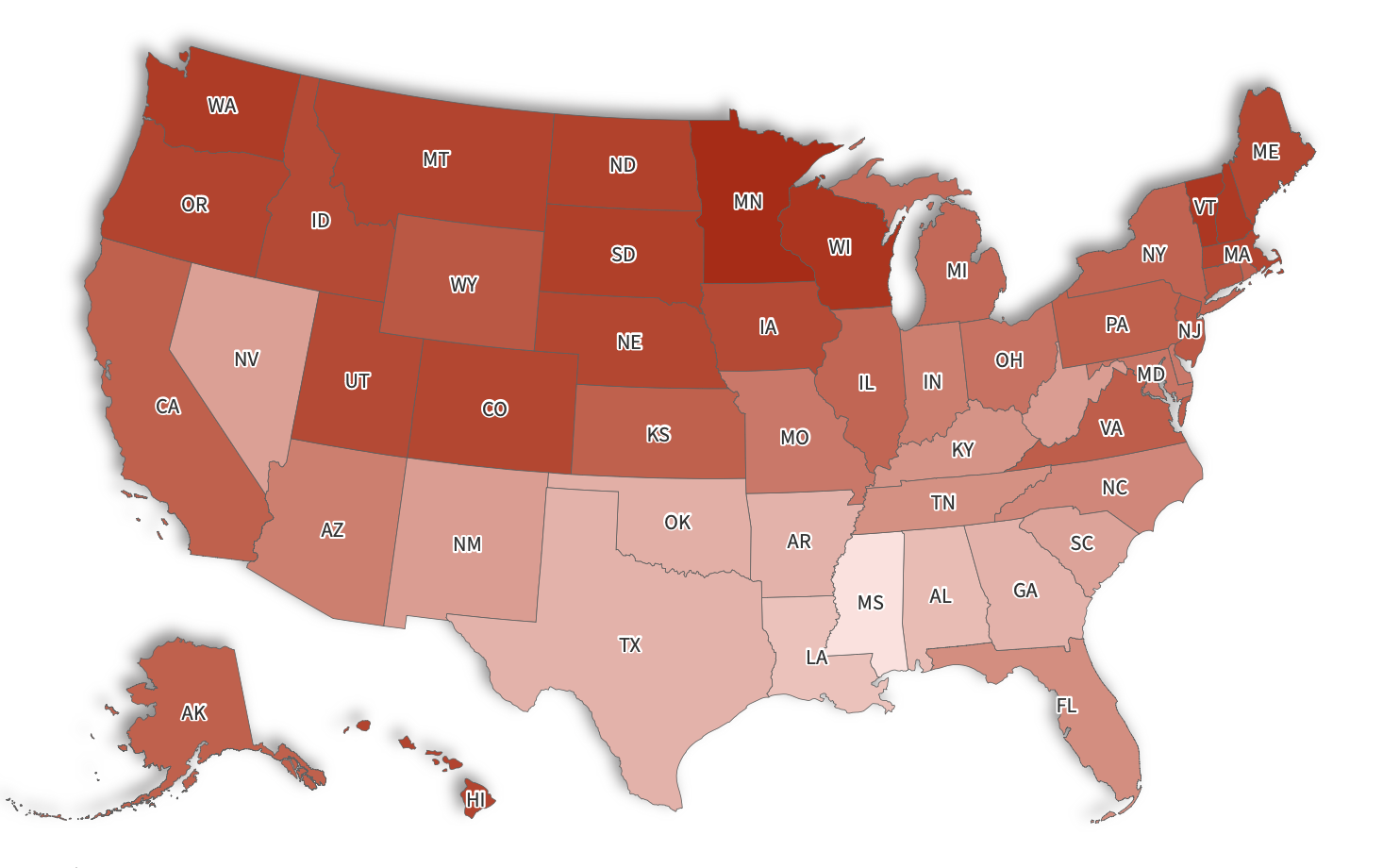

State Credit Score Averages (2024)

Significant regional variations exist in average credit scores. In 2024,Wisconsin boasted the highest average score at 738,followed by Vermont (737),New Hampshire (736),Washington (735),and North Dakota (733).

Conversely, the lowest average scores were found in Mississippi (680), Louisiana (690), Alabama (692), Arkansas (695), and a tie between Georgia and Texas (both 695). A concentration of states with lower average credit scores is observed in the south.

while a majority of Americans currently maintain credit scores within the “good” range, the evolving reporting landscape and the growing integration of BNPL services into credit metrics suggest potential shifts in the credit score distribution throughout 2025 and beyond.