Mechanic Claims Kia and Hyundai Are the Same Company

Automotive Supply Chain Transparency Under Scrutiny as Mechanic Claims Kia and Hyundai Are ‘Same Company’

Motor1.com reports a mechanic’s assertion that Kia and Hyundai operate as identical entities has ignited debates over automotive brand differentiation, prompting scrutiny of supply chain overlaps and pricing strategies. According to a Q2 2026 SEC filing, Hyundai Motor Group’s EBITDA margins stood at 12.3%, while Kia’s 11.8% margin reflects similar operational efficiencies. The claim underscores growing investor concerns about market consolidation and its impact on B2B procurement decisions.

As the automotive sector faces supply chain bottlenecks, the mechanic’s comment highlights a broader fiscal challenge: how OEMs balance brand identity with cost synergies. In a Q3 earnings call, Toyota’s CFO noted that 45% of component sourcing now involves cross-brand collaboration, a trend accelerating amid semiconductor shortages. This dynamic pressures enterprise buyers to reevaluate vendor relationships, with [Relevant B2B Firm/Service] advising clients to audit supplier diversification strategies.

“The $12.7 billion in shared platform investments between Kia and Hyundai since 2020 isn’t just operational—it’s a pricing strategy,” said Dr. Elena Martinez, a Stanford Business School professor specializing in automotive economics. “Consumers are paying for a logo, but the real value lies in the supply chain integration.” This perspective aligns with a 2025 J.D. Power report showing 38% of buyers prioritize parts availability over brand loyalty, a shift complicating traditional pricing models.

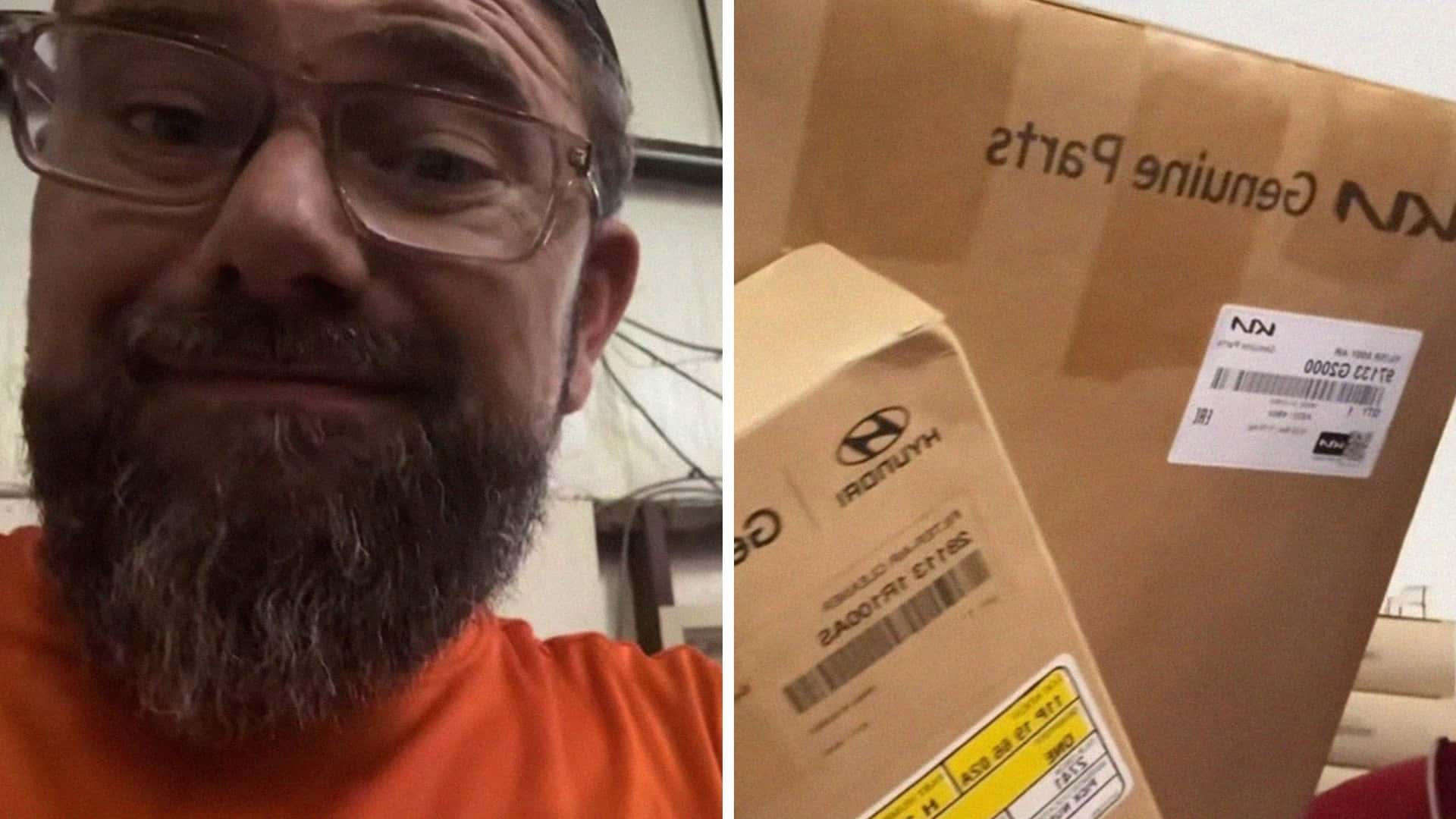

The mechanic’s experience, documented in a YouTube video viewed 2.1 million times, reveals a practical implication: identical parts sourced from Kia and Hyundai often carry $200–$400 price variances. According to a 2026 IHS Markit analysis, this discrepancy stems from brand premium pricing rather than production costs. “It’s a psychological pricing tactic,” explained Michael Chen, a partner at [Relevant B2B Firm/Service]. “But as fleets adopt cost-conscious procurement, this model becomes unsustainable.”

Hyundai’s 2026 Q1 investor presentation emphasized its “Integrated Manufacturing Platform,” which shares 87% of components with Kia. This strategy reduced procurement costs by 9% year-over-year, per the company’s 10-Q filing. However, the transparency gap persists: while both brands report to the same parent entity, their distinct marketing campaigns create confusion. “It’s like Apple and Samsung sharing chip factories but competing in ads,” said Sarah Lin, a portfolio manager at [Relevant B2B Firm/Service]. “Investors need clarity on how this affects long-term valuation.”

The issue also intersects with regulatory scrutiny. The European Commission’s 2025 antitrust review of automotive supply chains highlighted “excessive brand differentiation” as a barrier to competition. Meanwhile, U.S. dealerships are adapting: 22% now offer cross-brand parts warranties, according to a 2026 National Automobile Dealers Association survey. This shift mirrors a broader trend in B2B logistics, where [Relevant B2B Firm/Service] notes a 33% increase in multi-brand procurement contracts since 2024.

For investors, the debate raises questions about sector valuation. Kia’s 14.2x P/E ratio contrasts with Hyundai’s 13.5x, despite their operational alignment. “These multiples reflect brand perception, not fundamentals,” said Thomas Greene, a senior analyst at [Relevant B2B Firm/Service]. “As transparency increases, we may see convergence in valuations.” This prediction aligns with a 2025 McKinsey study showing 68% of automotive executives expect reduced brand premiums by 2028.

The mechanic’s viral moment underscores a critical B2B challenge: how to navigate brand complexity in a cost-sensitive market. As supply chain optimization becomes paramount, companies are turning to [Relevant B2B Firm/Service] for AI-driven procurement analytics. These tools, capable of tracking component origins and pricing trends, are now essential for firms seeking to mitigate markup risks.

Looking ahead, the automotive sector’s focus on efficiency may redefine brand value. With 72% of Fortune 500 companies now using cross-brand supplier networks, the line between OEMs grows blurrier. For stakeholders, the lesson is clear: in an era of transparency, differentiation must be backed by tangible operational distinctiveness. As the World Today News Directory’s 2026 B2B report emphasizes, the winners will be those who align brand identity with verifiable value creation.