Global Economic Slowdown & the Growing Finance–Trade Nexus

The latest Trade and Advancement Report 2025 paints a concerning picture of the global economy, forecasting a deceleration of growth to 2.6% in both 2025 and 2026,down from 2.9% in 2024.This represents a significant dip below the 3% average experienced before the pandemic and a stark contrast to the 4.4% growth rate preceding the 2008-2009 financial crisis.

This slowdown isn’t limited to the global average. The US economy is predicted to experience a deceleration to 1.8% growth in 2025 and 1.5% in 2026, while China’s expansion is projected to fall from 5% in 2025 to 4.6% in 2026 – a considerable decrease from its pre-pandemic average of 6.7%. The initial resilience observed earlier in the year is now appearing increasingly fragile.

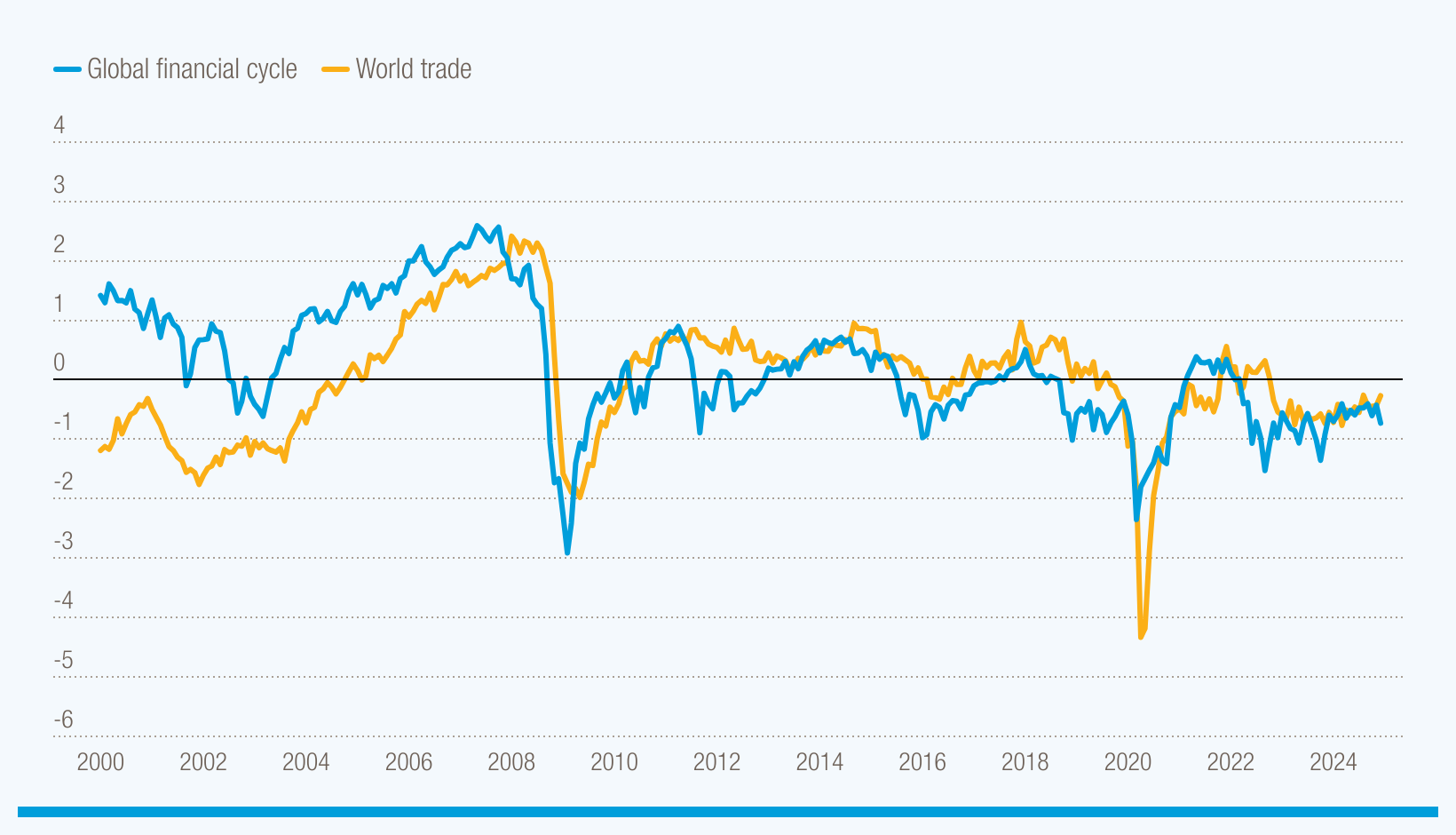

A key trend highlighted in the report is the increasingly intertwined relationship between trade and finance. While trade is frequently enough visualized thru physical logistics, it’s fundamentally underpinned by financial mechanisms – credit lines, exchange rates, and a complex network of banking institutions. Over 90% of global trade now relies on trade finance,meaning access to banking,payment systems,and financial instruments dictates who can participate in trade,under what conditions,and at what cost.

This integration makes trade considerably more susceptible to financial fluctuations, such as interest rate changes and shifts in investor confidence.This is especially evident in food markets, where financial operations, like agricultural derivatives, now generate over 75% of major trading companies’ income, eclipsing revenue from the actual movement of commodities.

This growing dominance of finance in trade creates vulnerabilities, especially for developing nations. Currency volatility increases import costs and debt burdens, while fluctuations in global risk appetite can abruptly cut off access to crucial credit. These countries are disproportionately impacted by financial instability. Furthermore, when market prices are driven by financial signals rather than underlying economic realities, businesses in developing countries face an uneven competitive landscape.

The report underscores a widening disparity: developing countries now contribute over 40% of global output and merchandise trade, attracting nearly 60% of global Foreign Direct Investment (FDI).However, they collectively hold only 25% of global financial market value. This limited presence in financial markets restricts firms’ ability to secure funding, frequently enough forcing reliance on foreign banks and significantly higher, more volatile interest rates. While advanced economies can borrow at rates between 1% and 4%, many emerging markets face rates of 6% to 12% for comparable government bonds, hindering investment in vital areas like infrastructure, innovation, and climate resilience.

To address these challenges and build greater economic resilience,the report proposes a series of targeted reforms:

* Revitalizing the multilateral trade dispute system to ensure consistent rule enforcement and reduce uncertainty.

* Improving data collection on trade and investment to facilitate better-informed policy decisions.

* Reforming the international monetary system to mitigate damaging currency and capital flow swings.

* Strengthening regional and domestic capital markets to provide developing countries with access to affordable, long-term financing.

* Enhancing openness in commodity trading and expanding access to affordable trade finance, particularly for small and medium-sized enterprises.

Ultimately, achieving genuine economic resilience requires a holistic approach that integrates trade, finance, and sustainability, empowering developing countries to actively shape global economic shifts rather than simply reacting to them.