Ireland vs Europe: Comparing Energy Costs

Ireland currently maintains some of the highest energy costs in the European Union, with net electricity prices ranking as the most expensive in the bloc. Driven by data center expansion and grid constraints, these costs place significant fiscal pressure on Irish enterprises compared to EU peers in Spain and Germany.

The pricing disparity is not merely a statistical anomaly; it is a structural burden. While the headline figures often obscure the details, the raw data reveals a stark reality for the Irish balance sheet. When taxes are stripped away, Ireland possesses the most expensive electricity in the EU. This creates a hidden overhead that erodes the competitive edge of domestic firms, forcing them to seek out energy management consultants to mitigate volatility.

The discrepancy between “net” and “gross” pricing is largely a function of fiscal policy. Ireland’s VAT rate on electricity stands at 9 per cent, significantly lower than the approximately 20 per cent seen in many other EU member states. On paper, this makes the final bill seem less severe, but the underlying cost of the energy itself is the highest in the union. This is a critical distinction for any CFO analyzing operational expenditure.

Operational costs are spiraling.

The Historical Divergence of Irish Energy Costs

Data from the Sustainable Energy Authority of Ireland (SEAI), based on EU Electricity and Gas Price Regulation statistics, highlights a persistent gap between Ireland and the Euro Area. Looking back at the average electricity price to business, the trend is clear. In 2007 (S2), Ireland’s price stood at 12.50 Euro cent/kWh compared to 9.06 for the EU-27. By 2015 (S1), Ireland had climbed to 14 Euro cent/kWh while the EU-27 sat at 12.42.

This gap has not closed; it has widened. According to a presentation from the Economic and Social Research Institute (ESRI), Ireland is consistently positioned among the countries with the highest electricity prices in Europe. The divergence became acute between 2018 and 2023. In the period ending H2 2023, average EU electricity prices rose by 73 per cent compared to H1 2018. In Ireland, that same metric surged by 148 per cent.

Most EU countries that saw price spikes in 2022 and early 2023 experienced a convergence back toward the EU-27 average by the second half of 2023. Ireland did not. It remained an outlier, decoupled from the broader European recovery.

The grid is struggling to keep pace with demand.

The Macro Drivers of the Price Surge

The fiscal drag on Irish businesses is not an accident of the market but a result of specific systemic pressures. The current energy landscape is defined by three primary catalysts:

- The Data Center Dilemma: The rapid proliferation of data centers has placed unprecedented pressure on the national grid. This surge in demand, coupled with a relatively small and dispersed population, has created a supply-demand imbalance that drives prices upward.

- Emergency Generation Costs: To plug the gap between electricity demand and supply, Ireland has been forced to procure high-cost, high-emission emergency gas generation. This “stop-gap” measure adds a premium to the cost of energy that other EU nations avoid through more integrated or robust grids.

- Net Price Inflation: With net electricity prices being the highest in the EU, the fundamental cost of generation and transmission is inflated. Businesses facing these costs often require corporate tax advisors to navigate the complex interplay between low VAT rates and high base costs.

“Irish households have been paying electricity prices that are well above the EU average for years. So these latest figures from Eurostat aren’t surprising unfortunately,” says Daragh Cassidy of bonkers.ie.

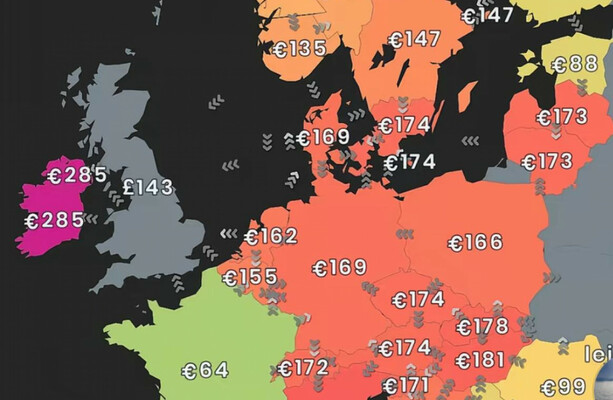

The problem extends beyond electricity. Gas prices in Ireland are the fifth-highest in the EU, sitting more than 15 per cent above the EU average. For the average household, this translates to paying €183 more per year for gas and roughly €350 more for domestic electricity alone than their EU counterparts. For a business, these figures scale exponentially, impacting everything from EBITDA margins to long-term capital expenditure plans.

Infrastructure Bottlenecks and the Path Forward

The government’s “White Paper on Ireland’s Transition to a Low Carbon Energy Future 2015-2030” outlined a commitment to developing metrics for energy cost competitiveness. However, the reality on the ground suggests that the transition is hitting a wall of infrastructure limitations. When electricity in Ireland is potentially five times more expensive than in Spain, the “competitiveness” of the region is called into question.

The necessity for emergency gas generation is a red flag for institutional investors. It indicates a lack of baseload stability. To resolve this, the market is seeing an increased reliance on infrastructure engineering firms to modernize the grid and integrate renewable sources more efficiently.

Price maps tell a story of geography and inefficiency. Ireland’s position as an island, combined with its role as a global tech hub, has created a perfect storm of high demand and limited supply.

Looking ahead to the next fiscal quarters, the trend suggests that unless there is a radical shift in generation capacity, Irish firms will continue to operate under a “cost penalty” relative to their European competitors. This is no longer just an energy issue; it is a macroeconomic risk. Companies that fail to optimize their energy footprint now will find their margins squeezed as the gap between Irish and EU-27 averages persists. For those seeking to hedge against this volatility, the only viable move is to partner with vetted B2B specialists through the World Today News Directory to secure operational efficiency before the next price shock hits.

- Central and Eastern European Governments Conserve Electricity Amid Danube River Power Threats

- Fed Faces AI Bubble and Oil Price Shock Risks

- RAP vs. IBR: What Your New Student Loan Bill Actually Costs (daybreakwire.com)

- Banks Maintain Stable Credit Rates Despite Rising Borrowing Costs and Iran Conflict (archyde.com)