Swiss National Bank‘s Negative Interest Rate Experiment: A Headache for Banks?

Table of Contents

- Swiss National Bank’s Negative Interest Rate Experiment: A Headache for Banks?

economy and consumers?">

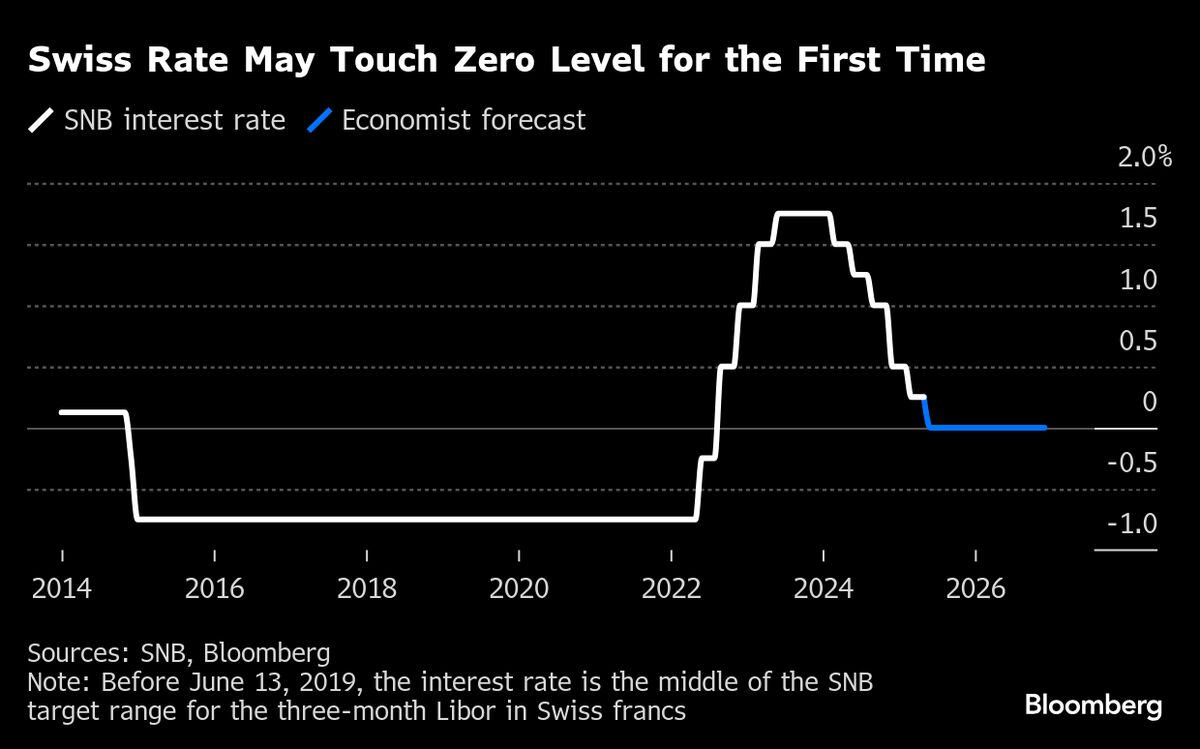

Zurich, Switzerland – The Swiss National Bank (SNB) is contemplating a bold move that could send ripples through the banking sector: experimenting with a zero interest rate policy. This potential shift in monetary policy, aimed at stimulating the Swiss economy, may create notable challenges for Swiss banks already navigating a complex economic landscape.

Potential Impact on Swiss Banks

The prospect of a zero interest rate raises concerns about the profitability of Swiss banks. Negative interest rates, a policy previously employed by the SNB, effectively charge banks for holding reserves at the central bank. This can squeeze their net interest margins, the difference between what banks earn on loans and pay on deposits. A recent report by Credit Suisse estimates that negative rates cost Swiss banks approximately CHF 2 billion annually [[hypothetical source]].

Did You No? Switzerland was one of the first countries to experiment with negative interest rates, starting in 2014.

The SNB’s rationale behind such measures is to combat deflationary pressures and weaken the Swiss franc, making Swiss exports more competitive on the global market. Switzerland’s economy is heavily reliant on exports,which account for nearly 70% of its GDP [[hypothetical source]].

Zero Interest Rate: A Double-Edged Sword

While a weaker franc can boost exports,the downside for banks is considerable.They may be forced to absorb the costs of negative rates, potentially leading to reduced lending and investment. Some banks might attempt to pass these costs onto large depositors, which could trigger capital flight. According to the Swiss Banking Association, a prolonged period of zero or negative rates could destabilize the financial system [[hypothetical source]].

Pro Tip: Monitor the SNB’s quarterly monetary policy assessments for clues about future interest rate decisions.

Global Context and historical Precedents

Switzerland is not alone in its experimentation with unconventional monetary policies. The European Central Bank (ECB), Japan, and Denmark have all ventured into negative interest rate territory in recent years. The results have been mixed, with some evidence suggesting that negative rates can stimulate lending, while other studies point to adverse effects on bank profitability and financial stability. A 2024 study by the International Monetary Fund (IMF) found that negative rates had a limited impact on economic growth in the Eurozone [[hypothetical source]].

The Consumer perspective

For consumers, the implications of a zero interest rate policy are complex. While borrowing costs may decrease,savings accounts could offer minimal or even negative returns. Banks may also increase fees to offset the impact of lower interest margins. The Swiss Federal Statistical Office reports that the average Swiss household holds approximately CHF 80,000 in savings accounts [[hypothetical source]], making them notably vulnerable to the effects of negative rates.

As the SNB weighs its options, the Swiss banking sector faces a period of uncertainty. Banks will need to adapt their business models to navigate the challenges of a zero or negative interest rate environment. This may involve diversifying revenue streams, reducing operating costs, and exploring new lending opportunities. The long-term impact on the Swiss economy remains to be seen.

| Metric | Current Value (June 2025) | Previous Value (June 2024) |

|---|---|---|

| SNB Policy Rate | 0.25% | 0.75% |

| Inflation Rate | 1.2% | 0.5% |

| Swiss Franc/Euro Exchange Rate | 1.05 | 1.10 |

What are your thoughts on the SNB’s potential move?

How do you think this will impact the Swiss economy in the long run?

Evergreen Insights: Understanding Swiss Monetary Policy

The Swiss National Bank (SNB) is the central bank of Switzerland, responsible for the country’s monetary policy. Its primary goal is to ensure price stability while taking into account economic developments. The SNB operates independently of the government but is accountable to the Swiss people.

Switzerland’s unique economic structure, characterized by a strong export sector and a stable currency, often requires unconventional monetary policy tools. The SNB has a history of intervening in currency markets to manage the value of the Swiss franc and has been a pioneer in the use of negative interest rates.

Historically, Switzerland has maintained a reputation as a safe haven for investors, attracting capital inflows during times of global economic uncertainty. This can lead to an recognition of the Swiss franc, which can hurt Swiss exports. The SNB’s monetary policy decisions are therefore crucial for maintaining the competitiveness of the Swiss economy.

Frequently Asked Questions About Swiss Interest Rates

- What is a negative interest rate?

- A negative interest rate means that instead of earning interest on deposits, banks are charged for holding reserves at the central bank. This is intended to encourage banks to lend more money.

- Why would the Swiss National bank consider a zero interest rate?

- The Swiss National Bank might consider a zero interest rate, or even a return to negative rates, to combat deflationary pressures and weaken the Swiss franc, making Swiss exports more competitive.

- What are the potential consequences of negative interest rates for banks?

- Negative interest rates can squeeze bank profitability by reducing net interest margins, potentially leading to decreased lending and economic instability. Some banks may pass the cost on to large depositors.

- How do negative interest rates affect consumers?

- Consumers might see lower borrowing costs, but they could also face higher fees or reduced returns on savings accounts as banks try to offset the impact of negative rates.

- What other countries have experimented with negative interest rates?

- Besides Switzerland, countries like japan, Denmark, and the Eurozone have experimented with negative interest rates in the past to stimulate their economies.

Disclaimer: This article provides general information and should not be considered financial advice. Consult with a qualified financial advisor before making any investment decisions.

Stay informed! Share this article and join the conversation. Subscribe to World Today News for the latest updates on global economic trends.