Second Wave of Inflation Hits: Bond Markets Turn Red as Yields Surge Globally

The U.S. Treasury yield curve, a barometer of financial stability, has flattened to levels not seen since the 2008 global financial crisis, according to data from major bond market platforms. On Tuesday, yields on 10-year Treasury notes surged to 4.25%, the highest since 2007, while two-year notes climbed to 4.02%, widening the spread between short- and long-term debt instruments to just 23 basis points—a threshold economists warn signals heightened recession risks.

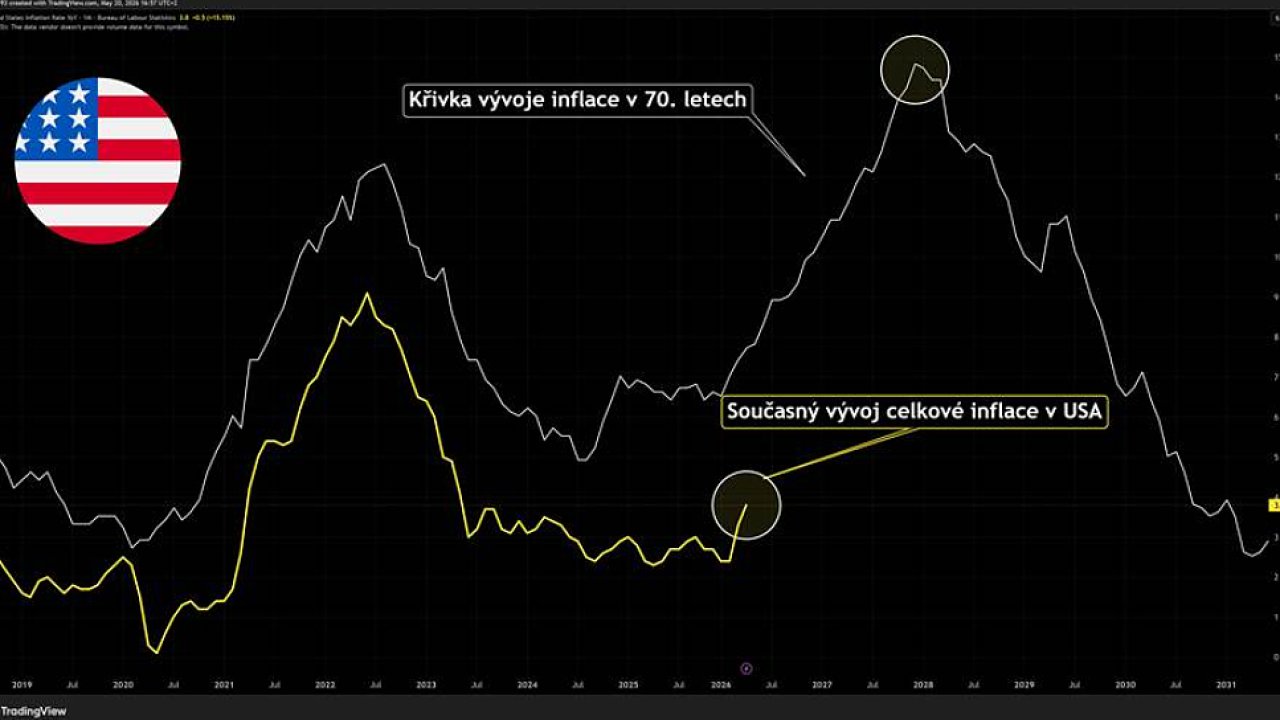

Traders and analysts described the shift as a “second wave of inflationary pressure” unfolding despite Federal Reserve efforts to cool price growth through aggressive interest rate hikes. “The bond market is sending a clear message: the Fed’s tightening cycle has not yet broken inflation’s momentum,” said a senior strategist at a European investment bank, who requested anonymity due to client sensitivity. The strategist pointed to a 20-year high in Treasury yields as evidence that investors are pricing in prolonged economic uncertainty, with corporate bond spreads also widening to levels last observed during the 2022 banking sector turmoil.

Central to the market’s unease is the inversion of the yield curve between 3-month and 10-year Treasury notes, a phenomenon that has preceded every U.S. Recession since the 1950s. While Fed Chair Jerome Powell has repeatedly dismissed parallels to past crises, market participants are increasingly focused on the sharp rise in yields on U.S. Government debt, which now exceed those of Germany and Japan—traditionally seen as safer havens. The inversion deepened after data released Tuesday showed U.S. Consumer prices rising at an annualized rate of 3.8%, above the Fed’s 2% target.

The sell-off in bond markets has triggered a broader reassessment of risk across global financial markets. In Europe, German bund yields hit 2.8%, their highest since 2011, while Japanese government bonds (JGBs) saw their steepest sell-off in a decade as domestic investors rotated out of fixed-income assets. The spread between U.S. And European yields has widened to 1.45 percentage points, the largest gap since the eurozone debt crisis of 2012, according to trading desks at major banks.

Analysts at FXstreet.cz noted that the yield on 10-year U.S. Treasuries has climbed to its highest level since 2007, a development that has sent shockwaves through global capital flows. “This is not just a U.S. Story anymore,” said a fixed-income trader at a Swiss bank. “The domino effect is already visible in emerging markets, where currencies are under pressure as capital flees to perceived safety in U.S. Assets.” The trader cited the Mexican peso and Indonesian rupiah, both of which have depreciated by over 3% against the dollar this week.

Meanwhile, the increased volatility in bond markets has sparked concerns about the stability of pension funds and insurance companies, which hold large portfolios of long-duration debt. A report from Patria.cz highlighted how yields on corporate bonds have also surged to multi-year highs, forcing borrowers to pay premiums not seen since the pandemic-era liquidity crunch. The cost of refinancing debt for mid-sized firms has risen by nearly 40% in the past month, according to internal bank data.

In response to the market turbulence, the Federal Reserve has convened an emergency session of its Open Market Committee to assess whether additional policy measures are warranted. However, officials have so far refrained from signaling a shift in their stance, with Powell reiterating that “the data continues to support the current policy path.” The lack of immediate action has fueled speculation that the Fed may be caught between combating inflation and preventing a deeper economic slowdown, a dilemma that has left market participants bracing for further volatility.

As of Tuesday evening, trading desks in London, Frankfurt, and New York remained open late, with liquidity in long-duration bonds at historic lows. The European Central Bank (ECB) has also signaled caution, with President Christine Lagarde warning that “financial conditions are tightening rapidly,” though she stopped short of hinting at an imminent policy pivot. The interbank lending rates in euros have risen to 3.9%, their highest since 2001, further tightening credit conditions across the continent.

The unfolding bond market crisis has also drawn attention to the growing divide between U.S. And global monetary policy. While the Fed has paused rate hikes, central banks in emerging economies—including Brazil, South Korea, and Turkey—have continued raising rates to defend their currencies, exacerbating the mismatch in borrowing costs. This divergence has led to a sharp decline in cross-border capital flows, with private equity and hedge funds pulling back from developing markets.

For now, the focus remains on whether the current yield spike will persist or if it marks a temporary correction. Historically, such inversions have preceded recessions by 12 to 18 months, but the Fed’s ability to navigate this terrain without triggering a deeper downturn remains untested. With no immediate resolution in sight, traders are bracing for what one London-based strategist described as “a prolonged period of uncertainty.”