IFR Predicts Significant Growth in All Robotics Market Segments

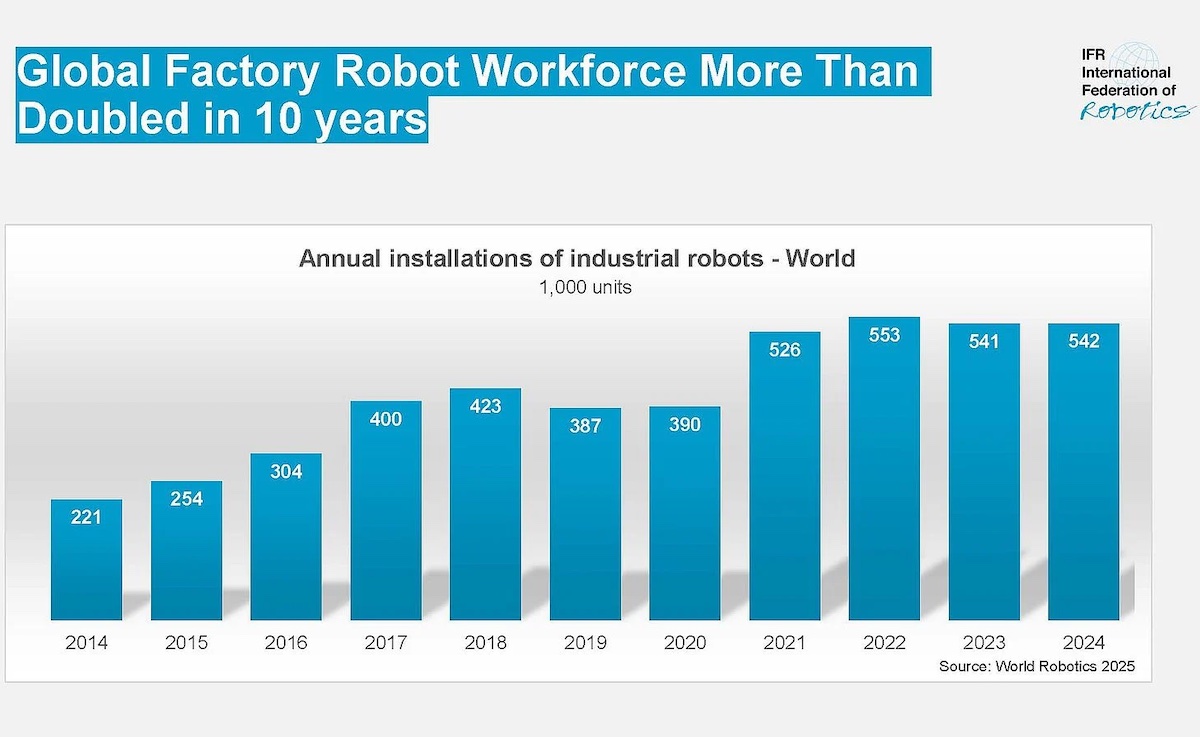

Global industrial robotics adoption is accelerating, yet remains a non-linear economic transition as manufacturers struggle with high capital expenditures and integration friction. According to the International Federation of Robotics (IFR), global robot density hit a record 162 units per 10,000 employees in 2025, though fragmented regional adoption rates and labor market volatility continue to obscure the path toward universal automation.

The industrial sector faces a capital allocation dilemma. While robotics promise to compress unit labor costs and improve EBITDA margins in the long term, the immediate fiscal reality involves heavy upfront depreciation and specialized talent shortages. For many mid-market firms, the transition is not an inevitability but a calculated risk often requiring external oversight from specialized financial consulting firms to ensure ROI targets are met before the next fiscal cliff.

The Capital Expenditure Hurdle

Robotic integration requires a significant shift in balance sheet management. Companies are moving from variable labor costs to fixed asset-heavy models, a transition that increases sensitivity to interest rate fluctuations. As of June 2026, the cost of debt remains elevated, forcing firms to prioritize projects with the shortest payback periods.

Per the SEC filings of major industrial conglomerates, capital expenditure on automated systems has risen by 14% year-over-year, yet cash flow from operations has not seen a commensurate bump. This divergence suggests that the “automation dividend” is lagging behind the initial investment cycle. Executives are now turning to corporate law firms to structure complex leasing agreements that shift robotic hardware from the balance sheet to operational expenses where possible, effectively mitigating the immediate impact on debt-to-equity ratios.

“The bottleneck isn’t the technology; it’s the institutional appetite for long-term horizon planning in a high-volatility environment. We aren’t just buying machines; we are buying a decade of maintenance, software updates, and the necessity for a completely different workforce skillset.” — Marcus Thorne, Chief Operating Officer at a Tier-1 Automotive Supplier.

Regional Variance in Market Penetration

Market data reveals a stark divide in how regions approach the robotics transition. The IFR data indicates that Asia remains the dominant force, accounting for over 70% of new installations, while North American and European manufacturers are more selective, focusing on high-precision segments where the margin spread justifies the initial outlay.

| Region | Robot Density (Units/10k Employees) | Growth Outlook (2026-2028) |

|---|---|---|

| South Korea | 1,012 | Stable/High |

| European Union | 145 | Moderate |

| North America | 138 | Accelerating |

This geographic disparity creates a complex supply chain environment. Firms attempting to standardize global production lines encounter massive interoperability issues. When local infrastructure or labor laws impede the deployment of standardized robotics, enterprises must engage supply chain optimization experts to recalibrate their regional distribution and production nodes.

Integration Friction and Operational Risk

Technology is only as effective as the systems supporting it. A common oversight in the current industrial cycle is the failure to account for cybersecurity and software maintenance costs. According to the European Central Bank’s latest Financial Stability Review, digital operational resilience is now a primary systemic risk for the manufacturing sector. An automated factory floor is a high-stakes target; downtime resulting from a software glitch or a security breach can erase a quarter’s worth of efficiency gains in hours.

The transition is not inevitable because the cost of failure is rising. A pivot toward robotics is a commitment to a permanent, high-maintenance digital infrastructure. Companies that fail to integrate robust risk management frameworks often find themselves trapped in a cycle of “automation debt,” where the cost of maintaining legacy robotic systems exceeds the productivity gains they were intended to provide.

The Path to Sustained Automation

The market is currently in a state of consolidation. Larger players are aggressively acquiring niche robotics software firms, while smaller manufacturers are opting for “Robot-as-a-Service” (RaaS) models to avoid the pitfalls of heavy upfront capital expenditure. This trend suggests that the future of the global economy will be defined by those who can best manage the transition to intelligent, automated systems without sacrificing liquidity.

Successful implementation requires more than just hardware. It demands a holistic strategy that balances technological ambition with fiscal reality. As market conditions evolve through the remainder of 2026, firms must ensure their operational and financial structures are sufficiently flexible to handle the ongoing volatility of the industrial sector. For businesses looking to secure their position in this evolving landscape, connecting with vetted, high-level partners through the World Today News Directory remains the most effective way to identify the expertise needed to manage these complex, capital-intensive transitions.