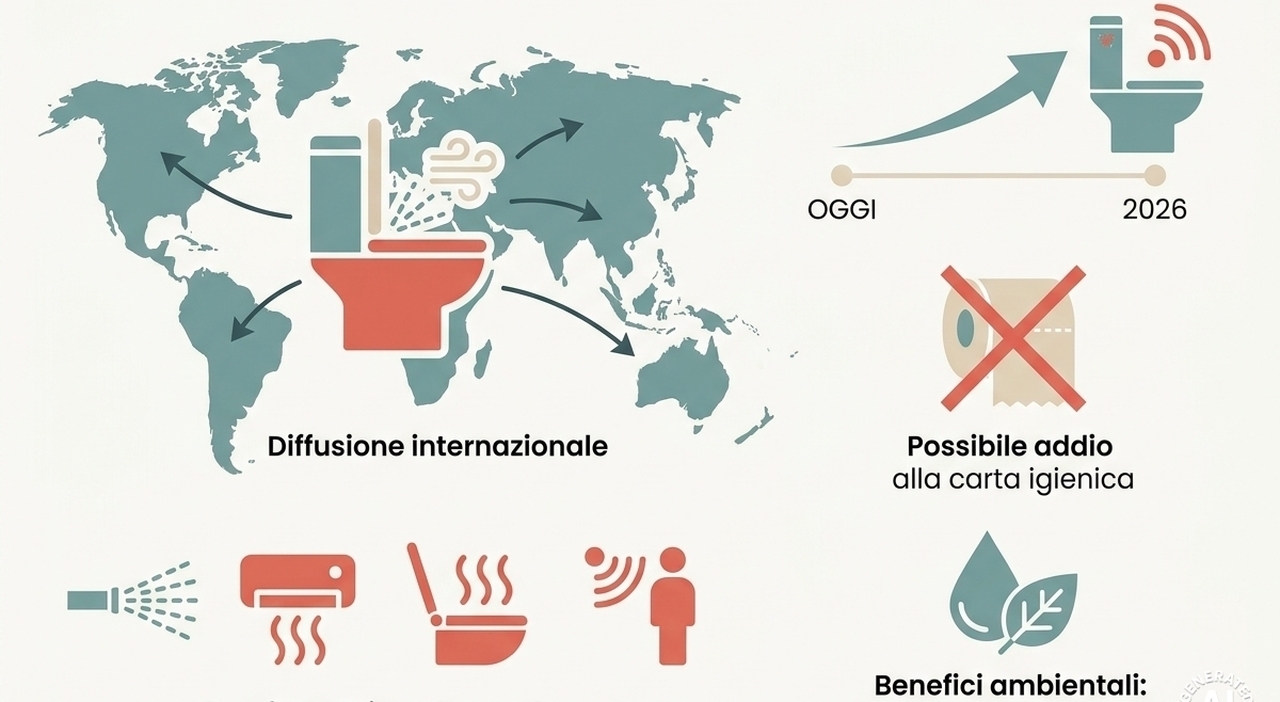

Goodbye to Toilet Paper in 2026? The Trending Global Bathroom Alternative

The global sanitary paper market, valued at approximately $28.5 billion in 2025, faces a structural disruption as consumer preferences shift toward bidet technology and integrated water-based hygiene systems. Driven by sustainability mandates and rising raw material costs, the transition away from traditional toilet paper is accelerating across European and North American retail channels, forcing legacy manufacturers to re-evaluate their long-term capital expenditure strategies.

The Fiscal Mechanics of the Hygiene Shift

For consumer packaged goods (CPG) firms, the shift represents more than a change in consumer behavior; it is a fundamental challenge to the high-margin, high-volume model that has defined the paper industry for decades. According to the Food and Agriculture Organization (FAO), pulp and paper production remains highly sensitive to energy price volatility and sustainable sourcing requirements. As demand for traditional cellulose-based products softens, companies are seeing a contraction in EBITDA margins as they struggle to amortize the costs of massive, single-use production facilities.

This transition necessitates a rigorous audit of supply chain resilience. Manufacturers are increasingly turning to supply chain management firms to mitigate the risks associated with declining volume and the necessary pivot toward electronic bathroom hardware integration.

“The commoditization of paper products has reached a ceiling. When you look at the Q1 2026 balance sheets of major tissue producers, the inventory turnover ratios are signaling a clear need for product diversification. Investors are no longer rewarding simple scale; they are demanding a transition toward long-term asset utility,” says Marcus Thorne, a senior sector analyst at Global Market Insights.

Capital Allocation and the Hardware Pivot

The move toward bidet integration changes the nature of the “bathroom economy.” Unlike paper, which requires constant replenishment and creates a recurring revenue cycle, bidet-integrated fixtures are durable goods. This structural change forces firms to shift their business model from recurring CPG revenue to a mix of hardware sales and maintenance services. This requires a sophisticated approach to corporate finance and treasury management, as companies must manage the transition from low-cost, high-frequency manufacturing to high-cost, low-frequency hardware assembly.

The following table outlines the comparative financial impact of the transition for a mid-market hygiene firm:

| Metric | Traditional Paper Model | Integrated Bidet Model |

|---|---|---|

| Revenue Frequency | High (Weekly/Monthly) | Low (One-time/Service) |

| Capital Intensity | Moderate (Pulp/Machinery) | High (R&D/Electronics) |

| Inventory Turnover | Rapid | Slow |

| EBITDA Margin | 12–15% | 18–22% |

Regulatory Pressure and ESG Compliance

Regulatory bodies, particularly within the European Union, are tightening the definition of “sustainable consumer goods.” Recent amendments to the EU’s Circular Economy Action Plan prioritize the reduction of single-use materials. This regulatory tailwind is a primary driver for the 2026 shift. Firms failing to adapt their product mix face increasing scrutiny from institutional investors who utilize ESG (Environmental, Social, and Governance) scores to determine capital allocation.

Legal teams are now central to this transformation. Companies are engaging corporate law firms to navigate the complex web of environmental compliance, liability regarding electronic components in plumbing systems, and the restructuring of distribution contracts that were historically optimized for bulk paper transport.

The Infrastructure of the Future Bathroom

As the market moves toward 2027, the focus shifts to the infrastructure required to support these new systems. The integration of high-pressure water systems and electric components requires significant retrofitting of existing residential and commercial properties. This creates a secondary market for specialized installation and plumbing engineering services.

The volatility in the pulp market, evidenced by the World Bank’s recent commodity price index, suggests that the cost of paper production will likely remain high through the next fiscal year. This price floor acts as a catalyst for consumers to adopt alternatives. The transition is not merely a trend; it is a fiscal necessity for households looking to hedge against inflation in essential goods.

For corporate leaders, the lesson is clear: the era of paper-based dominance is entering its terminal phase. Firms that fail to leverage the current liquidity to pivot toward sustainable, durable hygiene solutions risk becoming stranded assets in a market that no longer values their core output. Organizations looking to survive this structural shift must prioritize strategic partnerships with specialized business consultants to ensure their operational models align with the realities of the next decade.