UAE corporate tax compliance is now at the center of a structural shift involving tighter enforcement and integrated tax reporting. The immediate implication is heightened operational risk for firms that lag in registration, filing, or data reconciliation.

The Strategic Context

The United Arab Emirates introduced a federal corporate tax regime to broaden itS non‑oil revenue base and align with international tax standards. While the framework is relatively new, the Federal Tax Authority (FTA) has signaled a move toward systematic enforcement, mirroring global trends toward greater tax clarity and data integration across regimes such as VAT.

Core Analysis: Incentives & Constraints

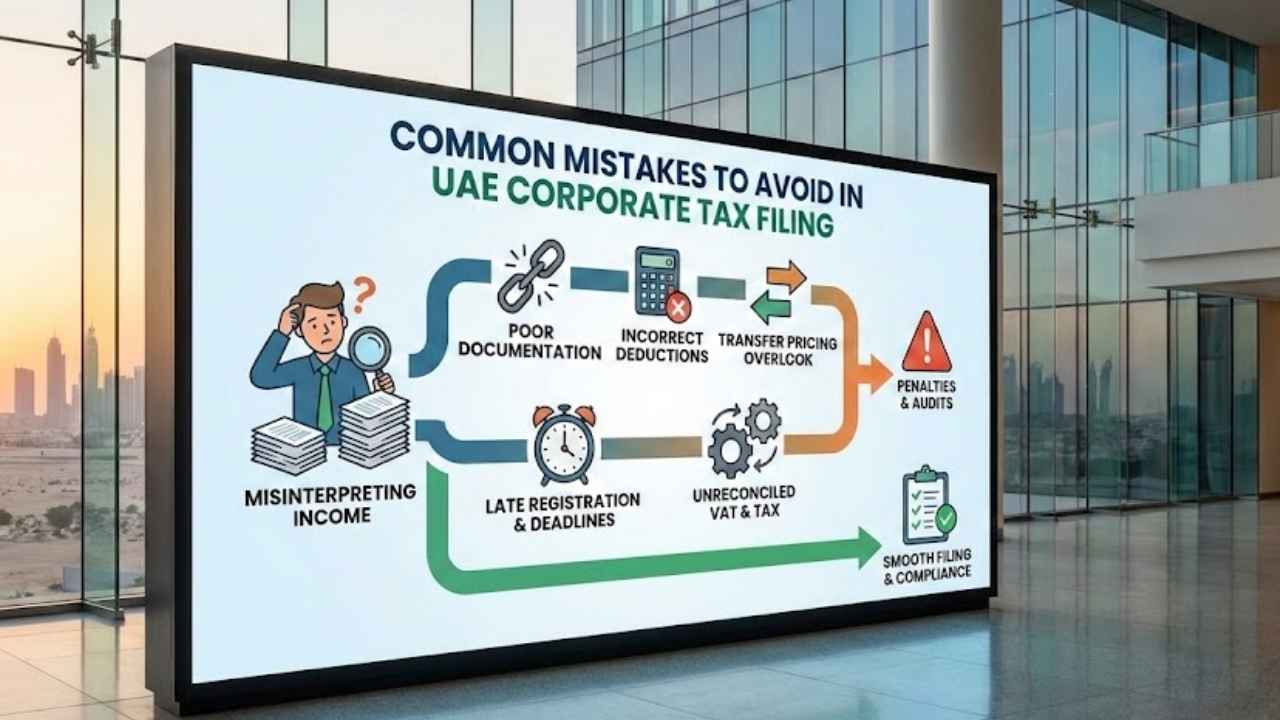

Source Signals: The source text identifies three recurring compliance gaps: (1) delayed corporate tax registration,(2) missed filing deadlines,and (3) failure to reconcile corporate tax data with VAT records. It notes that late registration incurs fines,missed deadlines trigger penalties,and data mismatches raise audit risk.

WTN Interpretation:

- Incentives: Early registration secures access to tax credits, avoids penalty accrual, and signals credibility to investors and the FTA. Timely filing preserves cash‑flow predictability and reduces the cost of interest on late payments. reconciling tax and VAT data leverages shared financial systems, lowering internal audit workload and enhancing the firm’s risk profile.

- Constraints: Many firms operate with limited in‑house tax expertise, especially smes and free‑zone entities, creating reliance on external advisors. Seasonal business cycles and rapid growth can strain accounting resources, leading to procedural oversights. Additionally, the coexistence of multiple tax regimes (corporate tax, VAT, customs) introduces complexity that exceeds the capacity of legacy ERP systems.

- Structural forces: The UAE’s diversification agenda and its commitment to OECD‑aligned tax standards increase regulatory scrutiny. The FTA’s data‑analytics capabilities enable cross‑checking of corporate tax and VAT submissions, amplifying the cost of inconsistencies. Global moves toward country‑by‑country reporting further pressure firms to maintain unified financial narratives.

WTN Strategic Insight

“In jurisdictions where tax regimes are being layered, the single most effective compliance lever is the integration of reporting calendars and data pipelines-or else, procedural gaps become the default source of fiscal risk.”

Future outlook: Scenario Paths & Key Indicators

Baseline Path: If firms adopt unified compliance calendars, invest in ERP modules that link corporate tax and VAT ledgers, and maintain proactive engagement with the FTA, the incidence of penalties will decline. The FTA’s enforcement focus will shift toward substantive audit of high‑value transactions rather than procedural infractions.

Risk Path: Should firms continue to rely on fragmented processes and external advisors without internal capacity building, the volume of late registrations and mismatched filings is highly likely to rise. This would trigger a scaling‑up of FTA audit activity, perhaps leading to broader industry‑wide penalties and reputational spillovers.

- Indicator 1: Publication of the FTA’s quarterly penalty statistics (expected within the next 3 months).

- Indicator 2: Release of the corporate tax filing calendar for the upcoming fiscal year (typically announced 2 months before the filing deadline).

- Indicator 3: Uptake metrics of ERP integration solutions advertised by major UAE accounting software vendors (quarterly sales reports).