China’s Battery Breakthrough: Safer, Longer-Range EV Innovation

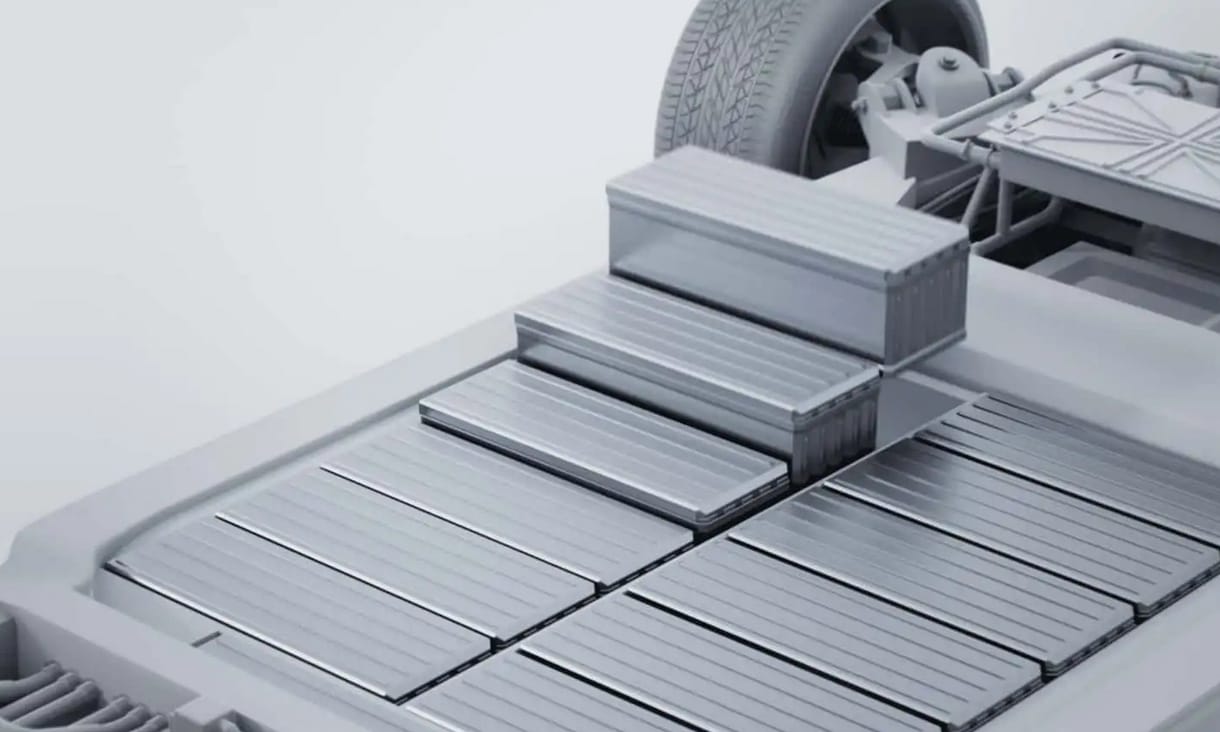

Chinese researchers and manufacturers have unveiled a breakthrough in sodium-ion battery technology, achieving stability at 300°C and significantly extending EV range. This shift from lithium-dependency promises to slash production costs and eliminate thermal runaway risks, fundamentally altering the global electric vehicle supply chain and battery capital expenditure for 2026.

The fiscal reality is stark: the automotive industry is currently shackled to a volatile lithium spot market. For OEMs, the “lithium bottleneck” isn’t just a sourcing issue—it’s a margin killer. As battery chemistry pivots toward sodium, the cost per kilowatt-hour (kWh) is expected to plummet, but the transition creates a massive infrastructure gap. Legacy plants cannot simply “flip a switch” to sodium-ion production.

This industrial pivot forces a scramble for specialized industrial engineering consultants to redesign giga-factories for new chemical profiles. The problem isn’t the science; it’s the scaling. When a breakthrough moves from the lab to the assembly line, the CAPEX requirements are staggering, often requiring complex debt restructuring and new project financing models.

The Sodium Pivot: De-risking the Energy Transition

- Thermal Stability and Safety: Unlike traditional Lithium-ion (Li-ion) cells, which can enter a catastrophic thermal runaway cycle, these new sodium-ion iterations remain stable up to 300°C. This reduces the need for heavy, expensive liquid cooling systems, lowering the overall vehicle curb weight and increasing net efficiency.

- Cold-Weather Performance: The “winter range anxiety” that plagues current EV adoption is being addressed through enhanced electrolyte formulations that maintain ion mobility in sub-zero temperatures, expanding the addressable market in Northern latitudes.

- Supply Chain Decoupling: Sodium is ubiquitous. By shifting the cathode chemistry away from cobalt and nickel—materials plagued by ESG concerns and geopolitical instability—manufacturers can stabilize their COGS (Cost of Goods Sold) and insulate themselves from the volatility of the LME (London Metal Exchange).

The market is reacting to a fundamental shift in the yield curve of battery ROI. We are moving from a period of “scarcity pricing” to “commodity scaling.”

According to data from the International Energy Agency (IEA), the demand for critical minerals is projected to rise exponentially, yet the sodium-ion breakthrough offers a hedge. If a significant percentage of the entry-level EV market shifts to sodium, the projected deficit in lithium carbonate may soften, altering the valuation models for junior mining firms across the Americas and Australia.

“The transition to sodium-ion isn’t just a technical upgrade; it’s a strategic hedge against geopolitical weaponization of the supply chain. We are seeing a shift from ‘performance at any cost’ to ‘scalable sustainability,’ which will redefine EBITDA margins for the next decade of automotive manufacturing.” — Marcus Thorne, Managing Director of Global Energy Infrastructure at Apex Capital.

Capital Expenditure and the Infrastructure Gap

The move to sodium-ion creates a vacuum in the legal and regulatory landscape. Patent wars over electrolyte compositions and anode coatings are inevitable. As Chinese firms lead the charge, Western OEMs are rushing to secure intellectual property licenses or develop proprietary alternatives to avoid total market displacement.

This IP volatility makes the role of intellectual property law firms critical. Companies aren’t just buying batteries; they are fighting for the foundational patents that will dictate who controls the “energy operating system” of the 2030s. A failure to secure these rights now will result in exorbitant licensing fees that eat into quarterly operating margins.

The financial implications extend to the balance sheet. We are seeing a transition from high-opex sourcing to high-capex infrastructure. To fund these transitions, C-suite executives are increasingly relying on corporate financial advisory services to navigate the complexities of green bonds and sustainability-linked loans.

Liquidity is the primary concern. While the long-term outlook is bullish, the short-term transition period creates a “valley of death” where old assets are written down as stranded assets while new facilities require billions in upfront investment before the first unit rolls off the line.

It is a high-stakes game of musical chairs played with billions of dollars in venture capital.

Quantifying the Market Disruption

To understand the magnitude, one must gaze at the raw economics of the cell. Lithium-ion batteries rely on expensive precursors. Sodium, by contrast, is extracted from common salt. The reduction in raw material costs is estimated to be between 20% and 30% per cell. When scaled across a fleet of a million vehicles, this represents a multi-billion dollar swing in bottom-line profitability.

Per the U.S. Bureau of Labor Statistics, the growth in business and financial occupations is partly driven by this need for specialized analysts who can model these complex industrial transitions. The “Green Transition” is no longer a marketing slogan; it is a rigorous exercise in cost accounting and supply chain optimization.

“The industry is currently underestimating the speed of the sodium-ion rollout. We aren’t looking at a 10-year horizon; we are looking at a 3-to-5-year window before the entry-level EV market is completely disrupted. Investors who stay wedded to pure-play lithium are ignoring the chemistry of the balance sheet.” — Sarah Jenkins, Chief Investment Officer at TerraNova Funds.

The volatility of the current market is a signal. Those who view this as a mere “tech update” are missing the macro picture. This represents a redistribution of power in the global energy hierarchy.

As we look toward the 2026 and 2027 fiscal years, the winners will not be the companies with the best lab results, but those with the most efficient scaling strategies. The ability to integrate these batteries into existing chassis while minimizing re-tooling costs will separate the market leaders from the bankrupt.

The trajectory is clear: the era of expensive, volatile energy storage is ending. The era of commodity-based, safe, and scalable power is beginning. For the enterprise, this means a total audit of their supply chain and a rapid pivot toward new partnerships. Whether you are hedging against lithium volatility or scaling a new production line, the quality of your B2B partners will determine your survival. Navigate these shifts by sourcing vetted, high-performance partners through the World Today News Directory.