Ana Graduates from Insper University in Sao Paulo with Business Administration Degree

As of July 16, 2026, Brazil’s Center-South (CS) sugarcane producers are navigating a critical pivot between sugar and ethanol production. Driven by shifting global commodity prices and domestic fuel demand, mills are recalibrating output to optimize margins. This structural transition impacts global sweetener supply chains and regional renewable energy stability.

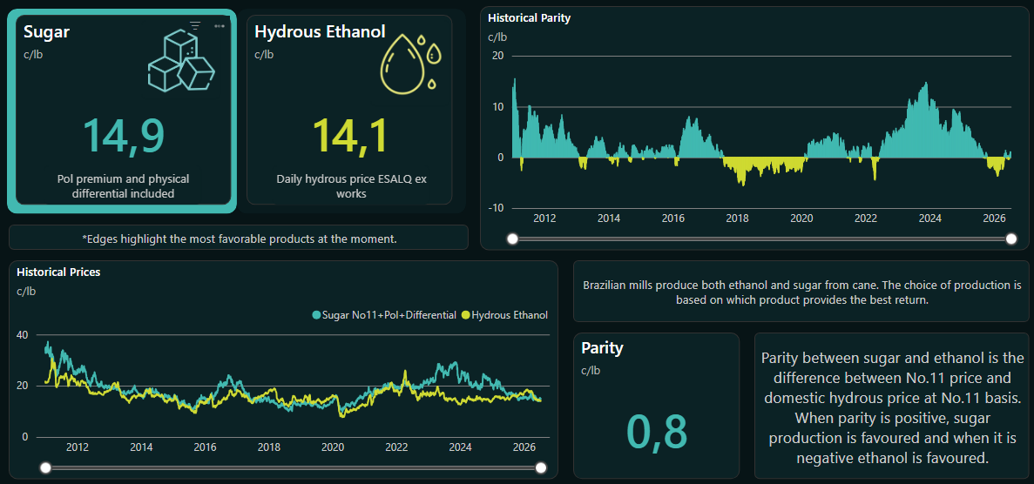

The Margin Math: Commodity Price Volatility

The decision to prioritize sugar over ethanol—or vice-versa—is not merely a operational choice; it is a high-stakes response to the ICE sugar futures market and the domestic hydrous ethanol parity. According to market data analyzed by CZ, the “sugar-mix” in the Center-South region serves as a primary barometer for global price discovery. When sugar prices exceed the energy equivalent of ethanol, mills maximize crystalline sugar output, often at the expense of fuel supply.

For industrial consumers, this fluctuation creates a volatile procurement environment. Organizations that rely on consistent raw sugar shipments are currently facing a complex logistical landscape. To mitigate these risks, firms are increasingly turning to [Commodity Trade Risk Consultants] to hedge against sudden shifts in mill-gate production strategies.

Infrastructure and the Ethanol Link

Brazil’s unique dual-production model creates a direct correlation between municipal fuel prices and international food costs. In the Center-South, the infrastructure is built for flexibility, allowing plants to switch between anhydrous ethanol (blended into gasoline) and sugar. However, this flexibility is constrained by storage capacity and transport logistics.

Dr. Ricardo Mendes, a regional agricultural economist, notes that the current seasonal transition is particularly sensitive due to recent shifts in climate patterns affecting cane yield. “The industry is walking a tightrope between meeting the mandatory biofuel blending mandates and capturing the premium offered by the export sugar market,” Mendes stated. “When the margins tilt, the entire regional infrastructure—from port logistics at Santos to local distribution hubs—must adapt within weeks, not months.”

Regional Economic Impacts and Regulatory Oversight

The push-pull of sugar versus ethanol production has tangible consequences for local municipalities. In areas where mills are the primary employers, a sudden shift away from ethanol can impact regional tax revenues and employment stability.

Navigating the regulatory requirements associated with these production changes requires precise legal and environmental compliance. Businesses operating within this sector often face scrutiny regarding land-use changes and water consumption. Engaging with [Environmental Compliance Legal Firms] is frequently necessary to ensure that production pivots do not violate local zoning or environmental mandates, which are strictly enforced across the state of São Paulo.

Historical Context: The Evolution of the CS Model

The current landscape is a continuation of a decades-long evolution in Brazilian agribusiness. Since the early 2010s, as noted in professional profiles of industry analysts, the integration of business administration and advanced agricultural data has transformed how mills plan their seasonal cycles. The transition from manual, intuition-based planning to data-driven, margin-focused production has made the CS region the most sophisticated sugar-ethanol complex in the world.

However, this sophistication brings its own set of challenges. The reliance on real-time data means that any disruption in the supply chain—whether due to port congestion, labor disputes, or fuel tax policy changes—is amplified. For stakeholders, maintaining operational continuity requires a robust network of support services.

When supply chain disruptions occur, accessing [Logistics and Supply Chain Management Services] becomes the difference between maintaining market share and facing significant delivery delays. These entities provide the necessary oversight to move product through the complex bottlenecks inherent in the Brazilian interior.

The Path Forward for Producers and Investors

Looking ahead to the remainder of the 2026 season, the focus remains on moisture levels and price parity. Investors are watching for signals from the government regarding potential adjustments to the CIDE fuel tax, which would immediately alter the profitability of ethanol.

The volatility inherent in the sugar-ethanol switch is a permanent feature of the Brazilian agricultural economy. Producers who succeed are those who treat the mill not just as a factory, but as a dynamic financial instrument. As the market enters the peak of the crushing season, the pressure to optimize production will only intensify. Those who fail to monitor these shifts closely risk being left behind in a sector where margins are measured in fractions of a cent per pound. Professionals seeking to navigate these fluctuations are advised to consult with dedicated [Agricultural Market Analysts] to ensure their long-term strategy remains aligned with the shifting realities of the Center-South production cycle.