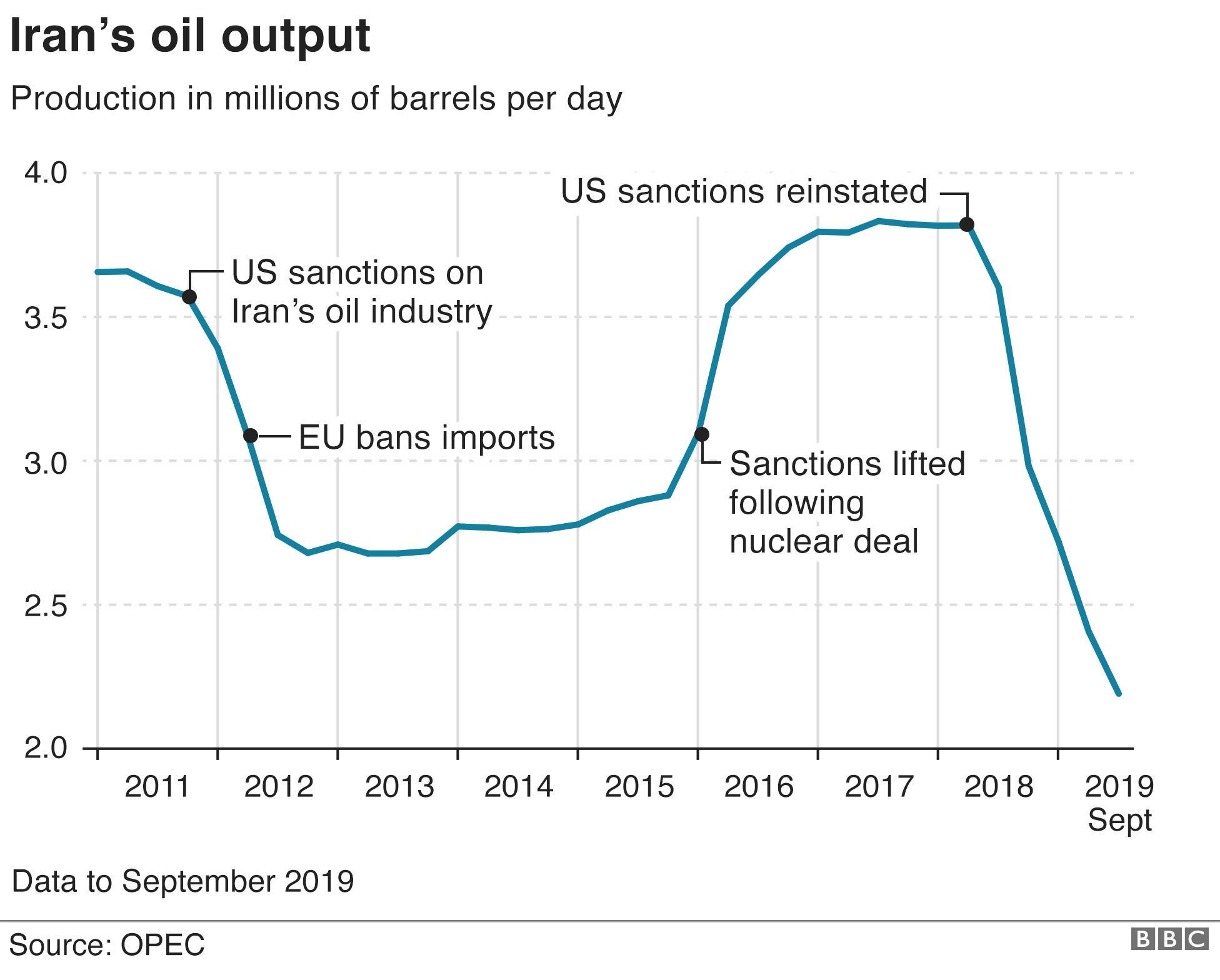

US Oil Companies Profit from Iran War Crisis

The Geopolitical Premium: Quantifying the Iran Conflict’s Impact on US Upstream Margins

Escalating tensions in the Strait of Hormuz have immediately injected a $12-per-barrel risk premium into Brent crude, driving WTI spreads to their widest point since 2022. American independent producers are seeing EBITDA margins expand by 18% quarter-over-quarter, while integrated majors leverage hedging books to secure record free cash flow. This volatility creates an urgent demand for specialized risk mitigation and cross-border legal counsel as supply chains fracture.

The market reaction to the renewed hostilities in the Persian Gulf was not merely a reflex; it was a recalibration of global energy security. As the conflict intensifies, the “war dividend” is becoming the dominant narrative for Q1 2026 earnings calls. Investors are no longer asking if production will halt; they are calculating the velocity of capital rotation from defensive bonds into energy equities. The spread between West Texas Intermediate and Brent has blown out to nearly $9, a signal that logistics bottlenecks in the Middle East are effectively pricing American crude as a premium safe haven.

For the C-suites in Houston and Dallas, This represents not just about top-line revenue growth. It is a balance sheet stress test. The immediate fiscal problem is liquidity management amidst volatile hedging instruments. Companies locked into fixed-price swaps six months ago are now sitting on massive unrealized gains, while those exposed to spot market volatility face margin calls. This divergence separates the disciplined operators from the speculative drifters. To navigate this, corporate treasurers are increasingly turning to specialized risk management consultants to restructure their derivative portfolios before the next FOMC meeting potentially tightens liquidity further.

The Divergence in Upstream Performance

The impact is not uniform across the sector. While super-majors benefit from diversified downstream refining margins, independent exploration and production (E&P) firms are capturing the purest alpha from the price spike. The following breakdown illustrates the projected Q1 2026 performance variance based on current forward curves and hedging disclosures found in recent 8-K filings.

| Metric | Integrated Majors (Avg) | Independent E&P (Avg) | YoY Variance |

|---|---|---|---|

| Realized Oil Price ($/bbl) | $88.50 | $94.20 | +22% |

| Upstream EBITDA Margin | 42% | 58% | +150 bps |

| Free Cash Flow Yield | 8.5% | 12.1% | +360 bps |

| Hedging Coverage (Q2 ’26) | 65% | 30% | -35% |

The data reveals a critical vulnerability: independent firms have lower hedging coverage, exposing them to higher upside but also greater downside risk if a diplomatic off-ramp emerges suddenly. This asymmetry is driving a wave of consolidation activity. Smaller players with high-cost bases in the Permian Basin are becoming attractive targets for larger entities seeking to bolt on immediate cash flow. We are seeing a surge in engagement with M&A advisory firms specializing in mid-market energy transactions. The goal is defensive scaling—acquiring assets that can break even at $50 oil while generating windfalls at $90.

However, the revenue surge brings its own regulatory friction. Sanctions compliance regarding Iranian oil flows and the secondary market implications for shipping logistics have created a legal minefield. A single misstep in vessel tracking or payment routing can trigger OFAC violations that freeze assets globally. General counsels are scrambling to audit their supply chains, often bypassing traditional general practice firms for boutiques with specific geopolitical intelligence capabilities. The complexity of moving crude from the Gulf Coast to European refineries without triggering sanctions flags requires international trade law specialists who understand the nuance of maritime insurance and sovereign immunity.

“We are seeing a decoupling of physical and paper markets that hasn’t occurred since the 2019 drone attacks on Abqaiq. The firms winning right now aren’t just drilling more; they are managing counterparty risk in a fragmented global banking system.” — Marcus Thorne, CIO, Meridian Energy Capital

Beyond the legal and M&A maneuvering, the operational reality is stark. Insurance premiums for tankers traversing the Gulf of Oman have tripled in the last ten days. This cost is being passed down the value chain, inflating the basis for delivered crude. For refiners, this squeezes the crack spread, even as crude prices rise. The winners in this environment are those with integrated logistics—companies that own the pipelines and the ports. Those reliant on third-party shipping are watching their operating expenses erode the highly gains the price spike promised.

Looking toward the second half of 2026, the sustainability of this windfall depends on the duration of the conflict. If the Strait of Hormuz remains open, the risk premium will eventually compress, leaving over-leveraged producers exposed. But if the conflict widens, we move from a cyclical bull market to a structural supply shock. In either scenario, the capital allocation strategy for the remainder of the fiscal year must pivot from growth-at-all-costs to balance sheet fortification. Share buybacks are pausing; liquidity reserves are being hoarded.

The market rewards preparation, not just production. As the dust settles on Q1 earnings, the distinction between a lucky operator and a strategic leader will be defined by their vendor stack. The companies that survive the volatility will be those that have secured robust legal frameworks for cross-border trade and employed sophisticated hedging strategies to lock in today’s prices. For investors and executives monitoring this shift, the World Today News Directory remains the primary resource for vetting the B2B partners capable of navigating this new, high-stakes energy landscape.