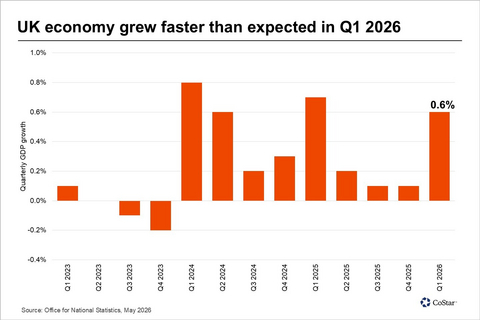

U.K. Economy Grows 0.6% in Q1 2026 Driven by Services Sector

The United Kingdom’s economy outperformed expectations in Q1 2026, recording a 0.6% growth rate as the services sector provided a robust tailwind. Driven by resilient domestic demand and a recovery in construction, the expansion marks a significant acceleration from the 0.1% growth observed in the final quarter of 2025.

Growth is rarely a uniform tide. While the headline figures from CoStar’s latest market intelligence suggest a strengthening macroeconomic backdrop, the underlying data reveals a bifurcated reality. Manufacturing output is hitting a four-year high, yet the volatility in travel and hospitality sectors highlights the fragility of consumer discretionary spending. For firms navigating this uneven recovery, the immediate challenge is not just capturing growth, but managing the operational friction that comes with rapid, sector-specific expansion.

The Real Estate Catalyst: Beyond the Headline

CoStar Group’s (NASDAQ: CSGP) data underscores a critical shift: commercial real estate is no longer just a passive asset class; it is the primary engine of operational agility. The return to growth in construction, albeit concentrated in repair and maintenance rather than ground-up development, signals that enterprises are optimizing existing footprints rather than expanding into new builds. This shift toward capital-efficient asset management is a direct response to sustained high interest rates and the lingering effects of quantitative tightening.

Market participants are watching the yield curve closely. As borrowing costs stabilize, the window for refinancing debt is narrowing. “We are seeing a pivot in corporate strategy,” notes a senior strategist at a global investment bank. “Companies are no longer waiting for the ‘perfect’ rate environment. They are leveraging data-driven insights to consolidate their real estate portfolios, prioritizing occupancy efficiency over sheer square footage.”

Operational Friction and the B2B Response

Growth creates its own set of administrative bottlenecks. As firms scale operations to match this unexpected Q1 uptick, the internal pressure on human resources and compliance departments spikes. When an organization pivots from defensive cost-cutting to aggressive expansion, the gaps in legacy infrastructure become glaring. Here’s where the [Relevant B2B Firm/Service: Enterprise Resource Planning (ERP) Integration Specialists] become essential. Without streamlined digital workflows, the margin gains achieved through increased output are often eroded by administrative overhead.

Similarly, the 0.4% rise in construction repair activity indicates that businesses are prioritizing the longevity of their physical assets. Facility management teams are under pressure to maintain high-spec environments while keeping Opex under control. Firms that fail to leverage [Relevant B2B Firm/Service: Predictive Facility Maintenance Consultants] risk unexpected capital expenditures that could derail the momentum built in the first quarter.

Macroeconomic Headwinds and the Services Sector

The services sector remains the U.K.’s primary growth engine, yet it is not immune to labor market tightness. According to the latest Bank of England Monetary Policy Report, wage growth continues to exert pressure on core inflation, complicating the path for future rate cuts. This environment forces a difficult trade-off for C-suite executives: increase prices and risk demand destruction, or absorb the costs and watch EBITDA margins compress.

The 6.4% decline in travel and tour operator activity serves as a canary in the coal mine. When consumers pull back on discretionary services, it is often the first indicator that the cost-of-living squeeze is beginning to outweigh the benefits of a broader economic recovery. For businesses operating in this space, the need for sophisticated hedging strategies and revenue management software is paramount. Engaging [Relevant B2B Firm/Service: Corporate Financial Advisory and Risk Management Firms] is the standard move for leadership teams looking to insulate their balance sheets against these sudden sector-specific demand shocks.

Strategizing for Q3 and Beyond

The disparity between manufacturing resilience—evidenced by a 53.6 PMI reading—and the contraction in leisure services demands a nuanced approach to capital allocation. Investors should look for companies with low debt-to-equity ratios and high operational leverage, as these firms are best positioned to capitalize on the ongoing services expansion without overextending their liquidity.

Predicting the trajectory of the U.K. Economy requires more than just reading the monthly GDP prints; it requires an understanding of how supply chain bottlenecks and energy costs are being priced into the broader market. As we move into the second half of the year, the winners will be those who transition from reactive management to proactive, data-informed strategy.

Navigating these complexities is not a solo endeavor. Whether you are a mid-market firm seeking to optimize your real estate footprint or an enterprise looking to overhaul your financial reporting to meet new regulatory mandates, the right expertise is the difference between stagnation, and scale. Explore the World Today News Directory to connect with vetted B2B partners, legal experts, and financial consultants who specialize in turning macroeconomic data into actionable corporate strategy.

The data is clear: the economy is moving. The question for leadership is whether your firm is built to keep pace.