Mortgage Delinquencies Rise Nationally in Q3 2025, Driven by FHA and VA Loan Performance

WASHINGTON, D.C. – November 14, 2025 – National mortgage delinquency rates ticked upward in the third quarter of 2025, according to the Mortgage Bankers AssociationS (MBA) latest National Delinquency survey. While overall increases were modest, critically important jumps were observed in FHA and VA loan delinquencies, signaling potential challenges for specific segments of the housing market.

The seasonally adjusted mortgage delinquency rate for all loans outstanding increased compared to the second quarter of 2025. Specifically, 30-day delinquencies rose 2 basis points to 2.12 percent, while 60-day delinquencies increased 4 basis points to 0.76 percent. The 90-day delinquency rate held steady at 1.11 percent.

A deeper dive into loan types reveals a more nuanced picture. Conventional loan delinquencies increased by 2 basis points to 2.62 percent. However, FHA loans experienced a more ample rise, with the delinquency rate climbing 21 basis points to 10.78 percent. VA loan delinquencies also increased,rising 18 basis points to 4.50 percent.

Looking at year-over-year trends, total mortgage delinquencies increased across the board.Conventional loans saw a slight decrease of 1 basis point,while FHA loans increased 32 basis points and VA loans decreased 8 basis points compared to the third quarter of 2024.

The survey also indicated a slight increase in foreclosure activity.The percentage of loans in the process of foreclosure at the end of the third quarter was 0.50 percent, up 2 basis points from the second quarter of 2025 and 5 basis points higher than one year ago.

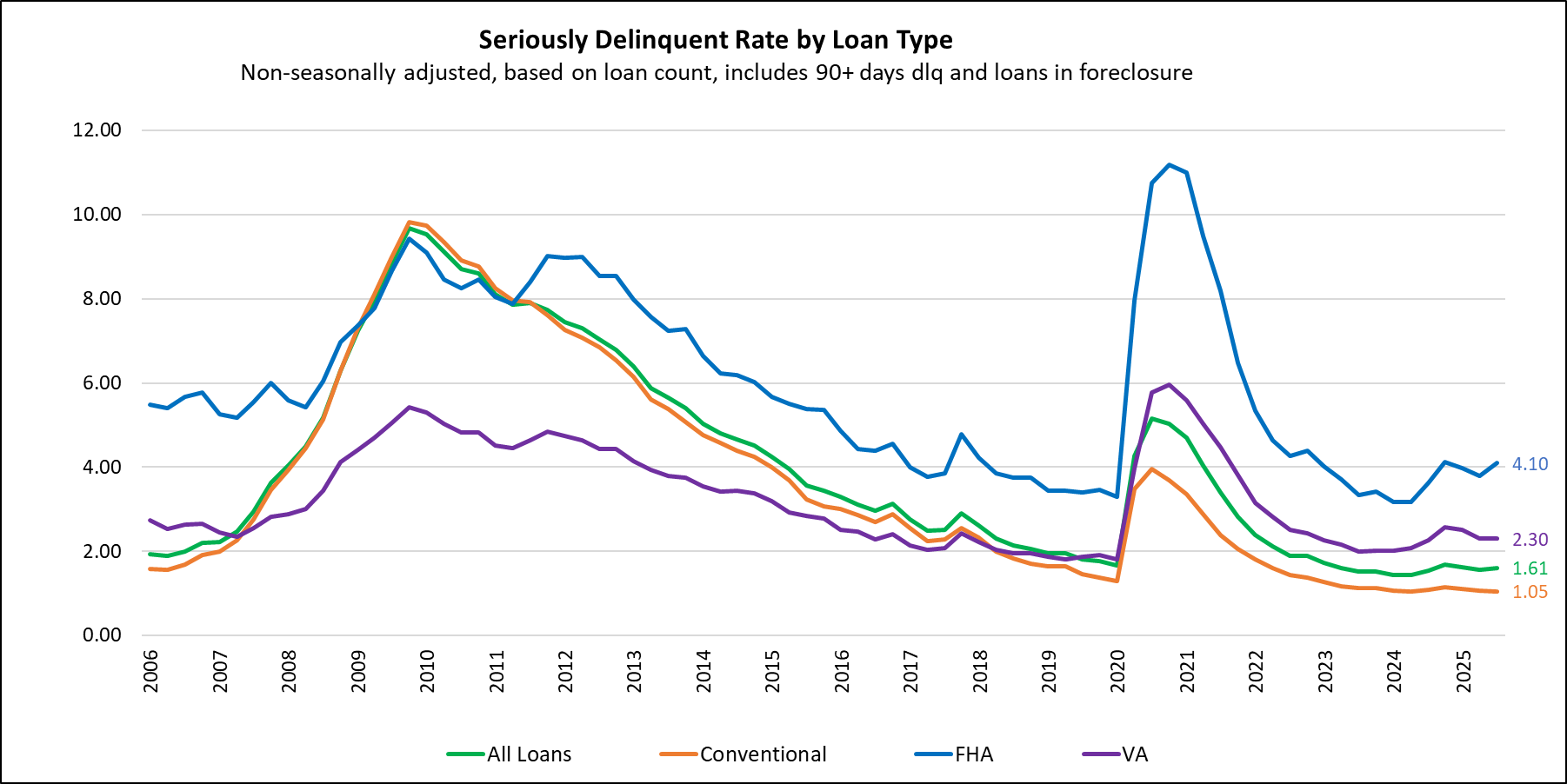

The non-seasonally adjusted seriously delinquent rate – encompassing loans 90 days or more past due or in foreclosure - was 1.61 percent, a 4 basis point increase from the previous quarter and a 6 basis point increase year-over-year. This rate decreased 2 basis points for conventional loans, increased 30 basis points for FHA loans, and decreased 1 basis point for VA loans from the previous quarter. Year-over-year comparisons showed a 4 basis point decrease for conventional loans, a 47 basis point increase for FHA loans, and a 4 basis point increase for VA loans.

Geographically, five states experienced the largest quarterly increases in overall delinquency rates: Arizona (29 basis points), Louisiana (28 basis points), Indiana (28 basis points), Iowa (26 basis points), and Texas (24 basis points).

It’s significant to note that the MBA survey instructs servicers to report loans in forbearance as delinquent if payments are not made according to the original mortgage terms.

These findings come as the housing market continues to navigate economic uncertainties, including inflation and fluctuating interest rates. While the overall delinquency rate remains relatively low compared to historical peaks seen during the 2008 financial crisis, the increases in FHA and VA loan delinquencies warrant close monitoring as indicators of potential financial strain among specific borrower groups.

Further details, including supplemental information on servicing portfolio performance by investor type, forbearance data, and servicer call volume, are available in MBA’s Monthly Loan Monitoring Survey at www.mba.org/lms.