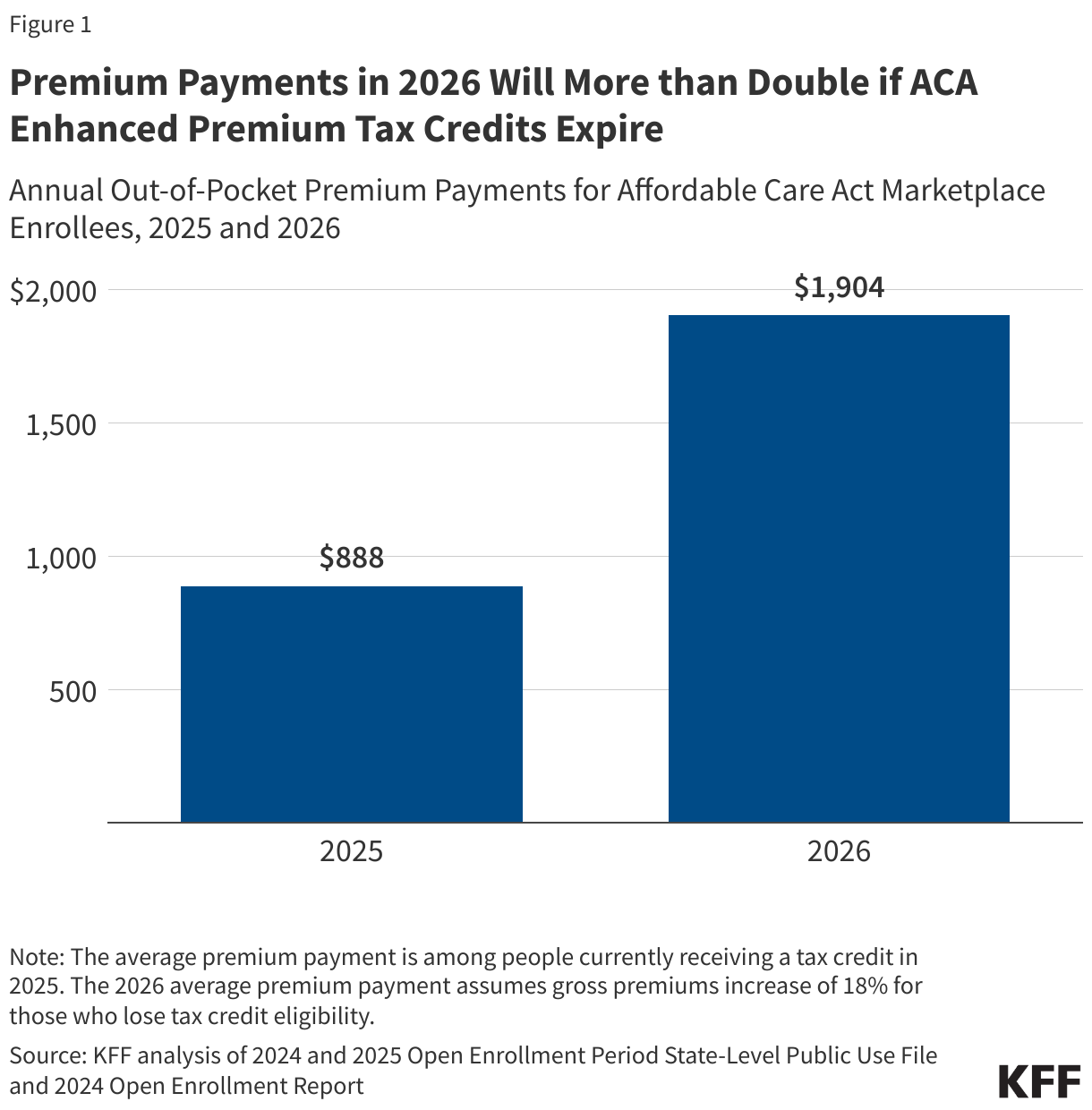

ACA Marketplace premiums Set to Surge in 2026 as Tax credit Expansion Nears Expiration

WASHINGTON, D.C. – Average premiums for individuals purchasing health insurance through the Affordable Care Act (ACA) Marketplace are projected to more than double next year if enhanced premium tax credits expire as scheduled,according to a new analysis. The analysis reveals significant financial impacts across income levels, possibly reversing gains in coverage affordability achieved through recent legislation.

Currently, a couple earning $75,000 annually – 150% of the federal poverty Level (FPL) – receives an average of $6,300 in premium tax credits, effectively covering 82% of their annual premium cost. Without the extension of these credits, that couple would see their premium payments rise to $12,800, representing a jump to 17% of their annual income, up from 8.5%.

The impact will be particularly acute for those with modest incomes. A 45-year-old earning $20,000 (128% FPL) in a state that has not expanded Medicaid could face annual premium payments of $420, a significant increase from the current $0, due to the loss of enhanced tax credits.

These projections are based on an analysis of 2024 enrollment data and forecasts for 2026, factoring in anticipated premium increases. The study notes that roughly 45% of ACA Marketplace enrollees have incomes between 100-150% of poverty, 28% between 150-250% of poverty, and approximately 10% earn above 400% of poverty.

The analysis estimates premium increases by extrapolating 2024 savings data,adjusting for income inflation based on federal poverty guideline changes,and accounting for a provision in the recent reconciliation bill impacting subsidized eligibility for lawfully present immigrants.It assumes a uniform income distribution within each income category and projects an 18% increase in average unsubsidized premiums for 2026, based on preliminary rate filings.

Researchers acknowledge that state-funded subsidies could potentially offset some of these increases, but these are not factored into the current estimations. The calculations also assume no changes in plan selection, family composition, income relative to FPL, or geographic location between 2024 and 2026. A Monte Carlo method was used to address rounding in data from the Open Enrollment report, ensuring accuracy in the overall findings.