The Impact of Long-Term Interest Rates

The decision to rent or buy in April 2026 hinges on a 6.50% average 30-year fixed mortgage rate. While homeownership builds long-term equity, current interest rates—driven by 10-year government bond yields—increase borrowing costs, forcing a cold calculation of liquidity versus asset appreciation across the U.S. Housing market.

This isn’t a simple lifestyle choice; We see a capital allocation problem. When the cost of debt climbs, the traditional “American Dream” narrative hits a wall of mathematical reality. The current fiscal environment creates a significant drag on disposable income, shifting the advantage toward renters who can maintain liquidity while waiting for a pivot in monetary policy.

For the corporate sector, this volatility isn’t just a consumer issue. It disrupts talent acquisition and executive relocation. Companies are now forced to reconsider housing stipends and relocation packages, often consulting real estate legal firms to navigate the complexities of corporate housing and lease-to-buy structures that mitigate the risk of high entry costs.

The Interest Rate Wall: Analyzing the 6.50% Benchmark

As of Saturday, April 4, 2026, Bankrate reports the current average 30-year fixed mortgage interest rate at 6.50 percent. For a prospective buyer, those basis points represent a massive increase in the total cost of credit over the life of the loan.

The math is brutal. At 6.50%, a significant portion of the early-year payments is swallowed by interest rather than principal amortization. This slows the build-up of home equity, making the “buy” side of the equation far less attractive than it was during the era of quantitative easing.

Liquidity is king in this market.

When a buyer locks a substantial down payment into a property during a high-rate environment, they sacrifice the ability to pivot their capital into higher-yielding liquid assets. This opportunity cost is the hidden tax of homeownership in 2026. To manage these risks, high-net-worth individuals are increasingly utilizing mortgage advisory services to structure loans that allow for future refinancing without predatory penalties.

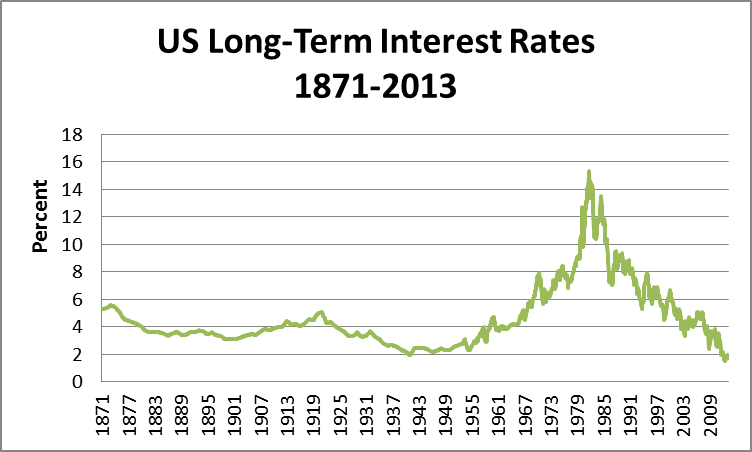

The Bond Connection: Why the 10-Year Yield Dictates Your Mortgage

Mortgage rates do not exist in a vacuum. They are tethered to the broader bond market. According to the OECD, long-term interest rates are primarily determined by the price of government bonds maturing in ten years. These bonds serve as the benchmark for risk-free returns, and when their yields rise, mortgage lenders must raise their rates to remain competitive and cover their own cost of capital.

This relationship creates a feedback loop. If the market anticipates persistent inflation, bond prices fall, yields rise, and the 30-year fixed rate climbs. The Federal Reserve Bank of St. Louis (FRED) tracks this weekly, providing a transparent look at how the 30-year fixed rate moves in lockstep with these macro trends.

The yield curve is the roadmap for the next fiscal quarter.

When the curve flattens or inverts, it signals a market that is bracing for a slowdown. In such a climate, the “rent” option becomes a strategic hedge. Renting allows a household to avoid the risk of negative equity—where the home’s market value drops below the outstanding loan balance—while maintaining a flexible debt-to-income ratio.

The Macro Breakdown: Three Pillars of the Rent vs. Buy Dilemma

To determine the optimal path in the current fiscal quarter, one must analyze the intersection of borrowing costs, asset liquidity, and monetary policy.

- The Cost of Capital Arbitrage: At a 6.50% mortgage rate, the “buy” decision only makes sense if the projected annual appreciation of the property plus the saved rent exceeds the interest expense. If rental markets soften or home price growth stagnates, the arbitrage fails, and renting becomes the mathematically superior choice for cash-flow preservation.

- Liquidity vs. Equity Traps: Homeownership is essentially a forced savings account, but it is an illiquid one. In a volatile economy, the ability to deploy capital quickly is a competitive advantage. Renters maintain a higher level of liquidity, allowing them to invest in equities or business ventures that may offer returns far exceeding the 3-5% typical of residential real estate appreciation.

- The Federal Reserve’s Shadow: The Federal Reserve Board’s H.15 report on selected interest rates provides the raw data on where the economy stands. Whether through quantitative tightening or adjustments to the federal funds rate, the Fed’s actions dictate the liquidity available to lenders. When liquidity dries up, mortgage spreads widen, pushing rates even higher regardless of the 10-year bond yield.

The Corporate Ripple Effect

This housing tension creates a secondary problem for the B2B sector. As employees struggle with the rent-vs-buy calculation, productivity and retention are impacted. The “housing crisis” for the mid-level manager is a “talent crisis” for the CEO.

Forward-thinking enterprises are addressing this by offering more than just a salary. They are integrating financial wellness programs and partnering with corporate tax consultants to optimize housing allowances and provide tax-efficient relocation benefits that help employees navigate the current interest rate environment.

The era of cheap debt is over.

We are now in a regime of “price discovery,” where the true cost of capital is being felt across every layer of the economy. The winners in this environment are those who treat their housing decision as a financial instrument rather than an emotional milestone.

The trajectory for the remainder of 2026 suggests a continued plateau in rates. Until the Federal Reserve signals a definitive shift in its monetary policy, the tension between renting and buying will remain a primary driver of consumer behavior and corporate strategy. For firms looking to navigate these headwinds, finding vetted B2B partners through the World Today News Directory is the only way to ensure your corporate infrastructure can withstand the volatility of the global markets.