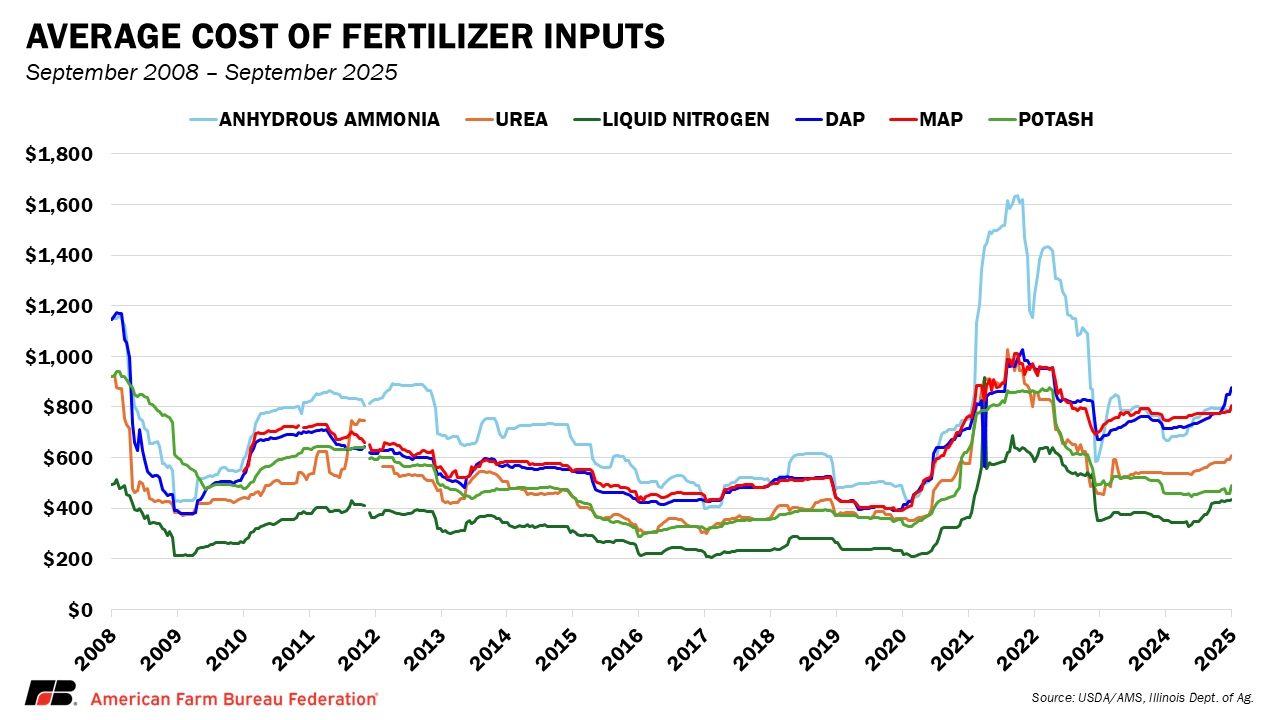

Rising Fertilizer and Fuel Prices Risk Global Food Shock

Escalating conflict in Iran has triggered a global agricultural crisis, driving fertilizer and fuel prices to critical thresholds. This supply-side shock threatens global food security, squeezing farm-gate margins and forcing a massive reallocation of capital as producers struggle to hedge against volatile input costs throughout the 2026 fiscal year.

The immediate fiscal problem is a crushing compression of EBITDA margins for mid-to-large scale agribusinesses. When the cost of nitrogen-based fertilizers—heavily dependent on natural gas feedstock—spikes alongside diesel volatility, the operational leverage of a farm flips from an asset to a liability. This isn’t just a “poor season”; it is a systemic liquidity event.

Farmers are now facing a solvency crisis. To survive the upcoming quarters, they are pivoting away from traditional credit lines and seeking sophisticated commodity risk management consultants to navigate the chaos of the futures markets.

The Macro-Economic Fracture: Input Inflation vs. Yield

The geopolitical instability in the Middle East has effectively severed the reliable flow of petrochemical precursors. According to the latest World Bank Commodity Markets Outlook, the correlation between regional conflict and the “Agflation” index has reached a historical peak. We are seeing a classic supply-chain bottleneck where the cost of production is outpacing the market price of the crop.

Liquidity is drying up in the rural heartlands. As working capital is devoured by fuel surcharges, the ability to finance the next planting cycle vanishes.

“We are witnessing a fundamental decoupling of production costs from consumer price ceilings. Farmers cannot pass 100% of these input hikes to the grocery store without triggering a demand collapse, meaning the producer absorbs the loss.” — Marcus Thorne, Chief Investment Officer at Agris Capital Management.

This imbalance creates a vacuum that only high-level corporate restructuring can fill. Many family-owned operations are currently consulting with specialized agricultural law firms to navigate bankruptcy protections or structured buyouts before the Q4 harvest window closes.

Three Vectors of the Global Food Shock

- The Nitrogen Trap: Fertilizer production relies on natural gas. With Iranian energy exports unstable and transit routes compromised, the price of urea and ammonia has surged. This forces farmers to either reduce application rates—risking lower yields—or overleverage their balance sheets to maintain productivity.

- Energy Logistics Paralysis: Fuel isn’t just for tractors; it’s for the entire cold chain. The surge in Brent Crude prices increases the “last-mile” cost of delivering produce to urban centers, creating a paradox where food is expensive for the consumer but unprofitable for the grower.

- Credit Tightening: As risk premiums rise, lenders are tightening covenants. The yield curve for agricultural loans is steepening, making it prohibitively expensive for farmers to secure the short-term liquidity needed for seed and chemical inputs.

The volatility is breathtaking.

One week, the market bets on a diplomatic ceasefire; the next, a drone strike on a refinery sends the price of diesel up 15% in a single trading session. This creates a “whiplash” effect that makes long-term fiscal planning impossible for anyone without a sophisticated hedging strategy.

Analyzing the Margin Collapse

To understand the gravity, one must look at the operational expenses. In a standard fiscal year, fuel and fertilizer typically account for 20-30% of total operating costs. Under the current Iran-driven volatility, those figures have ballooned to nearly 45% for many producers.

Per the FAO World Food Situation reports, the disruption in the Persian Gulf corridor has created a “butterfly effect” that is now hitting the Midwest US and the Brazilian highlands. The result is a dangerous contraction in net farm income.

When margins shrink this rapidly, the only move for the savvy operator is consolidation. We are seeing a surge in M&A activity as institutional investors swoop in to acquire distressed acreage. These transactions are rarely simple; they require the oversight of enterprise corporate accountants capable of valuing biological assets amidst extreme market turbulence.

“The current volatility is a catalyst for industry consolidation. We expect a 20% increase in land acquisitions by private equity firms as smaller operators hit their debt ceilings.” — Sarah Jenkins, Managing Director at Global Ag-Ventures.

The market is no longer rewarding efficiency; it is rewarding scale and liquidity.

The Path Toward Fiscal Recovery

The upcoming quarters will be defined by a shift toward “Precision Ag” and alternative inputs. The reliance on volatile global petrochemicals is now viewed as a systemic risk. We expect a massive capital rotation into bio-fertilizers and autonomous energy solutions—not because they are cheaper today, but because they remove the geopolitical risk premium from the balance sheet.

Though, the transition period is brutal. The “Information Gap” between the current crisis and the future solution is where most farmers are losing their shirts. They are operating on 20th-century intuition in a 21st-century geopolitical war zone.

The trajectory is clear: the era of cheap inputs is dead. The winners of the 2026-2027 cycle will be those who treat their farm not as a plot of land, but as a complex financial portfolio. Those who fail to hedge, fail to restructure and fail to seek professional B2B guidance will simply be absorbed by the larger players.

As the landscape shifts, the need for vetted, high-tier professional services becomes the only viable hedge. Whether it is navigating the complexities of international trade law or securing emergency liquidity, the World Today News Directory remains the definitive resource for connecting distressed enterprises with the B2B partners capable of stabilizing their fiscal future.