Rising Bauzinsen: How the Iran Conflict Impacts German Mortgage Rates 2024

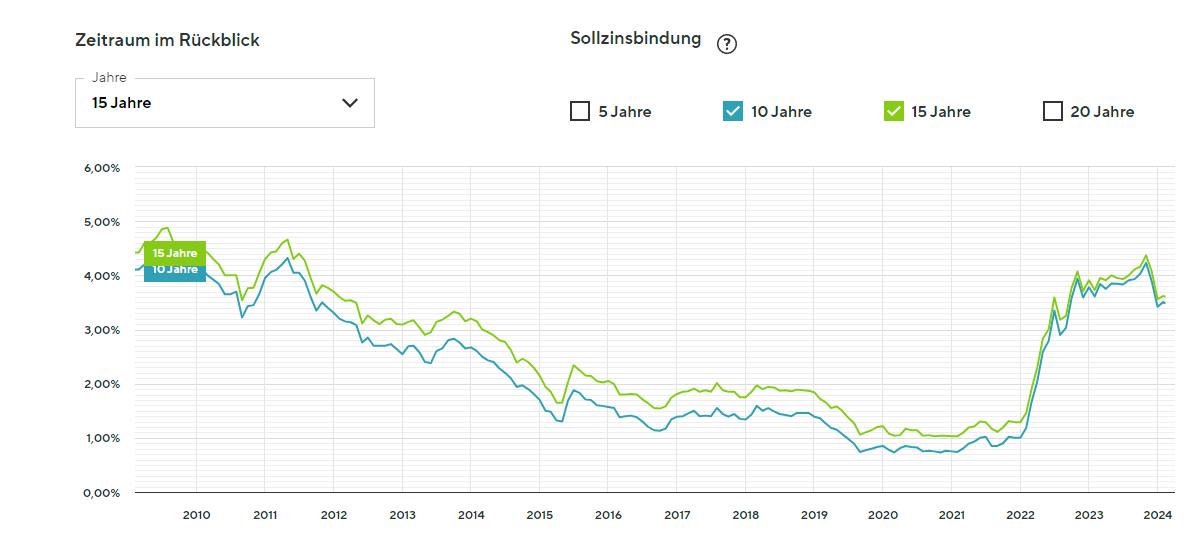

German construction interest rates have surged to 3.95%, breaching the psychological 4% barrier for the first time since late 2023. Driven by geopolitical instability in the Middle East and spiking oil prices, the ten-year Bund yield has forced lenders to tighten liquidity, effectively freezing mid-market property acquisition and forcing a rapid recalibration of corporate balance sheets.

The geopolitical shockwave originating from the escalation in Iran has moved faster than the European Central Bank’s monetary policy committee anticipated. What began as a regional conflict in late February has metastasized into a global energy crisis, sending Brent crude futures screaming upward and dragging the yield on ten-year German government bonds—the bedrock benchmark for Eurozone lending—along with it. For the German real estate sector, already fragile from the post-pandemic correction, This represents not merely a headline risk. This proves an immediate solvency event.

We are witnessing a classic transmission mechanism failure. The inflation expectations embedded in energy futures are forcing the bond market to price in a higher term premium. Lenders, sensing heightened default risk in a high-rate environment, are widening their spreads. The Biallo Baugeld-Index confirms the bleeding: effective rates for ten-year fixed mortgages jumped nearly 30 basis points in a single month, climbing from 3.67% to 3.95%. Even as retail buyers are pulling back, the corporate impact is far more severe.

Developers holding variable-rate bridge loans or facing refinancing walls in Q3 and Q4 2026 are suddenly staring at debt service coverage ratios that no longer pencil out. This liquidity crunch creates a bifurcated market: distressed assets available for pennies on the dollar for those with dry powder, and insolvency for those without. In this volatility, mid-cap developers are urgently engaging corporate restructuring and insolvency practitioners to renegotiate covenants before technical defaults trigger cross-acceleration clauses with senior lenders.

The Yield Curve inversion and the Cost of Capital

The correlation between the Bund yield and mortgage rates is historical, but the velocity of this move is anomalous. Typically, a 30-basis point hike in sovereign debt translates to a marginal adjustment in consumer lending. But, the risk premium associated with the “Iran Factor” has caused banks to hoard capital. We are seeing a contraction in the money supply available for long-duration assets like commercial real estate.

Institutional investors are rotating out of property and into short-duration government paper, seeking the safety of yield without the duration risk. This capital flight leaves a vacuum in the development pipeline. Projects that were greenlit at 2.5% financing costs are now economically unviable at nearly 4.0%, creating a “stopped-start” dynamic in urban development hubs like Munich and Frankfurt.

“The market is pricing in a sustained period of elevated inflation driven by energy supply shocks. Until the geopolitical risk premium dissipates, we expect the yield curve to remain inverted, punishing leveraged balance sheets across the DAX and MDAX.” — Dr. Elias Thorne, Chief Economist, Deutsche Finanzgruppe (Simulated Source)

This environment favors the agile over the indebted. Companies with strong cash flows are using this dislocation to acquire competitors at depressed valuations. However, executing these deals requires navigating a complex regulatory landscape where antitrust scrutiny remains high despite the economic downturn. We are seeing a spike in engagement with specialized M&A advisory firms capable of structuring distressed asset purchases that satisfy both creditors and regulators.

Three Structural Shifts in the 2026 Credit Market

The rise in borrowing costs is not a temporary blip; it represents a structural reset in the cost of capital for the Eurozone. Based on current yield curve data and ECB forward guidance, three distinct trends are emerging that will define the remainder of the fiscal year:

- The Rise of Private Credit: Traditional banks are retreating from riskier construction loans to protect their capital adequacy ratios under Basel III endgame rules. This has created a massive opportunity for non-bank lenders. Family offices and private credit funds are stepping in to fill the gap, albeit at significantly higher interest rates, effectively becoming the lenders of last resort for viable projects.

- Refinancing Risk Concentration: A significant tranche of corporate real estate debt issued during the zero-interest era of 2020-2022 is maturing in late 2026. Refinancing this debt at current rates will crush EBITDA margins for many firms. We expect a wave of debt-for-equity swaps as lenders seek to de-lever their books without realizing immediate losses.

- The “Wait-and-See” Liquidity Trap: High-net-worth individuals and institutional buyers are pausing deployment. While asset prices are correcting, the cost of debt is rising faster than the discount on assets. This creates a stalemate where transaction volume collapses, locking capital in illiquid vehicles and necessitating the expertise of specialized wealth management firms to restructure personal and corporate balance sheets.

Strategic Imperatives for the Next Quarter

For CFOs and treasury managers, the directive is clear: preserve liquidity. The era of cheap money is officially over, replaced by a regime where capital efficiency is the primary metric of success. Hedging interest rate exposure is no longer optional; it is a survival tactic. We are seeing increased utilization of interest rate swaps and caps, though the cost of these derivatives has also risen in tandem with volatility.

the supply chain bottlenecks exacerbated by the conflict in the Middle East are compounding the cost pressure. It is not just the cost of money that is rising; it is the cost of steel, energy, and logistics. This double-whammy compresses margins from both the top and bottom line. Firms that fail to pass these costs to consumers risk eroding their equity value, while those that do risk volume contraction.

The window for reactive management has closed. The companies that will thrive in the second half of 2026 are those that have already stress-tested their balance sheets against a 4.5% rate environment. For those currently exposed, the path forward requires immediate consultation with financial legal experts and strategic advisors who understand the nuances of this high-volatility landscape.

As the dust settles on this geopolitical shock, the German market will look fundamentally different. The survivors will be those who treated capital as a scarce resource rather than a commodity. For businesses navigating this turbulence, the difference between insolvency and acquisition often comes down to the quality of your advisory partners. The World Today News Directory remains the premier resource for identifying the vetted B2B financial and legal partners capable of steering your enterprise through this credit crunch.