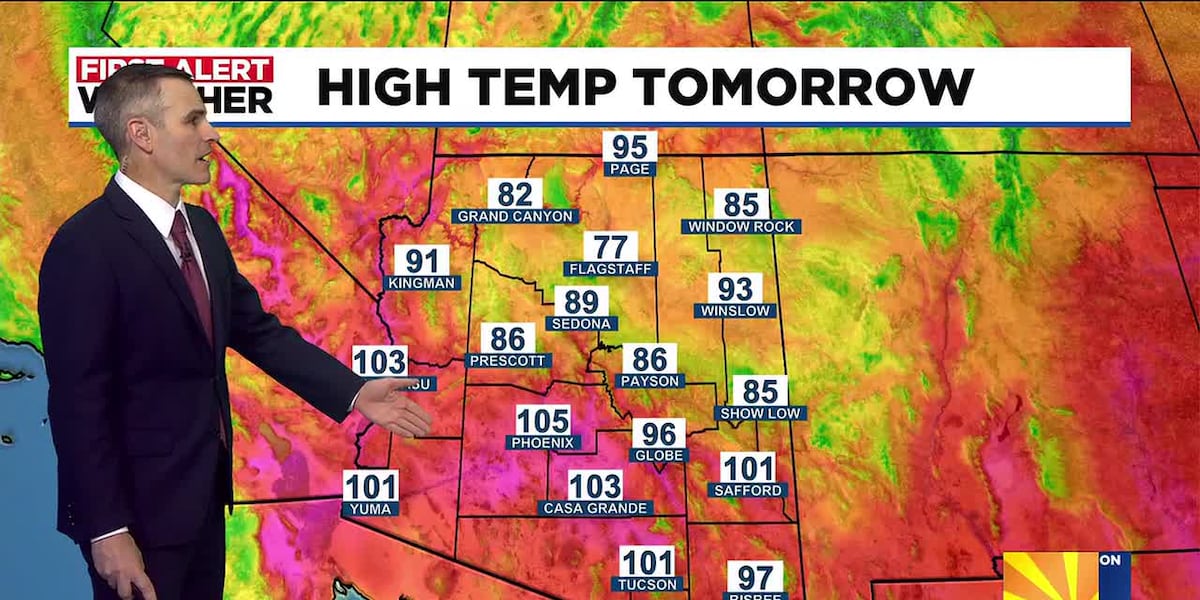

Return of Extreme Heat: 110-Degree Temperatures Expected This Week

Phoenix’s 110°F+ heatwave is back—and this time, the fiscal burn will hit utilities, logistics, and commercial real estate harder than ever. With the National Weather Service forecasting sustained triple-digit temperatures by mid-June, Arizona’s energy grid operators are scrambling to avoid a repeat of last summer’s record $2.1 billion in grid-related costs, while logistics hubs face supply chain slowdowns that could push freight rates up 15-20% by Q3. The question isn’t whether the heat will disrupt business—it’s how deep the pockets of mid-market firms will be when the cooling bills arrive.

Why Phoenix’s Heatwave Isn’t Just a Weather Story—It’s a Fiscal Stress Test

The city’s utility demand surges during 110°F+ stretches now account for roughly 25% of Arizona Public Service’s (APS) total summer load, according to the 2025 Integrated Resource Plan. Last year, APS’s peak demand hit 8,500 megawatts—up 12% year-over-year—while wholesale electricity prices spiked to $120/MWh during grid strain events. For commercial tenants in Phoenix’s Class 8 office parks, where average square footage per tenant exceeds 50,000 sq. ft., cooling costs now consume 10-15% of total operating expenses. “We’re seeing landlords pass through energy surcharges as a line item in leases,” says Raj Patel, Head of Real Estate Capital Markets at CBRE Phoenix. “The firms that don’t have hedging strategies in place are about to get blindsided.”

“By Q3, we expect to see a 10-15% uptick in tenant turnover in non-hedged Class B office spaces. The firms that don’t lock in power contracts now will face a 20-30% effective rate hike when the heat peaks.”

How the Heatwave Forces a Reckoning on Energy Hedging and Grid Resilience

Phoenix’s vulnerability isn’t just about air conditioning—it’s about the cascading effects on energy procurement, supply chain logistics, and commercial lease structures. Here’s the breakdown:

- Energy Cost Volatility: APS’s 2025 IRP projects that without additional baseload capacity, wholesale electricity prices could hit $150/MWh during peak demand days. Firms without fixed-price contracts are already seeing spot rates exceed $100/MWh—double the 2024 average. Energy risk management firms are reporting a 40% increase in inquiries from mid-market clients seeking hedging strategies.

- Logistics Gridlock: The Port of Phoenix handles 3.2 million container moves annually, but temperatures above 110°F force truckers to reduce payloads by 10-15% to prevent cargo spoilage. FreightWaves data shows spot rates on the I-10 corridor already up 12% YoY, with a further 5-8% spike expected by July. Cold chain logistics providers are the only ones laughing—their revenue per container is up 25%.

- Commercial Lease Renegotiations: Landlords with older buildings (pre-2010) face HVAC systems designed for 105°F max loads. Upgrades to ASHRAE 90.1-2019 standards can cost $5-$10 per sq. ft., pushing some tenants to walk. Green building financiers are seeing a surge in inquiries for retrofits—though the ROI timelines are brutal.

Who’s Getting Burned—and Who’s Buying the Fire Insurance?

The firms that thrive in this heatwave will be those with pre-positioned hedges, alternative energy sourcing, and supply chain agility. The rest? They’re about to learn why Phoenix’s real estate market has seen a 30% drop in Class B office space valuations since 2024.

| Sector | Key Risk | Solution Provider | Q2 2026 Cost Impact |

|---|---|---|---|

| Utilities & Energy | Wholesale price spikes, grid congestion | Energy procurement advisors | +15-25% for unhedged firms |

| Logistics & Freight | Payload reductions, spoilage costs | Cold chain logistics | +10-15% freight rates |

| Commercial Real Estate | HVAC upgrades, lease defaults | Green building financiers | -$5-$10/sq. ft. retrofit costs |

“The firms that don’t act now will be the ones negotiating from a position of weakness in Q4. The market isn’t just heating up—it’s becoming a liability for those who didn’t prepare.”

What Happens Next: The Q3 Fiscal Reckoning

By mid-July, Phoenix’s heatwave will have forced a reckoning on three fronts:

- Energy Contracts: Firms that locked in rates before May will see savings of $0.08-$0.12/kWh vs. those who waited. Corporate law firms specializing in energy procurement are already fielding calls about contract disputes.

- Supply Chain Shifts: The Census Bureau’s Q2 logistics report will likely show a 5-7% slowdown in Arizona’s freight volumes. Companies that diversified their logistics networks away from I-10 will outperform.

- Real Estate Valuations: Cap rates for Class B office spaces in Phoenix are expected to widen by 50-75 basis points by Q3, per CoStar data. Landlords with energy-efficient building management systems will command premiums.

The Bottom Line: Phoenix’s Heatwave Isn’t a One-Time Hit—It’s a Structural Cost

This isn’t a story about a single heatwave. It’s about the new baseline for Arizona’s economy. The firms that survive—and thrive—will be those that treat energy resilience, supply chain flexibility, and lease structuring as core fiscal strategies, not afterthoughts. For everyone else? The cooling bills are just the beginning.

Need a hedging strategy? A logistics overhaul? Or a green building retrofit plan? The World Today News Directory has the vetted partners to keep your business from wilting in the heat.