Overcoming Surplus Energy Challenges in Scaling Solar and Wind for 2060 Carbon Neutrality

The global energy transition is hitting a wall: solar and wind now generate more power than grids can absorb without blackouts or stranded capacity. By 2060, China alone will need 10,000 gigawatts of wind and solar—nearly seven times its current 1,408GW—yet current transmission and storage tech can’t handle the intermittency. The solution? Superconducting hybrid systems that could slash energy losses from 15% to near-zero overnight. But the fiscal math is brutal: deployment costs now exceed $140/ton CO₂ abated, and supply chains for rare-earth magnets are already snarled. The question isn’t whether this tech will work—it’s whether the capital stack can assemble fast enough.

Where the Money Bleeds: The $140/ton Abatement Crisis

A 2025 Nature study optimizing global PV/wind deployment laid bare the financial cliff: even with perfect coordination of storage, transmission, and mineral trade, the levelized cost of electricity for renewables stays elevated until grid-scale superconductors hit commercial scale. The abatement cost—currently $140/ton CO₂—must drop to $33/ton to meet 2040 net-zero targets. That’s a 77% reduction, but the capital expenditure isn’t linear.

“Superconducting cables could cut transmission losses by 90%, but the upfront capex is 3-5x traditional HVDC. The real bottleneck isn’t physics—it’s whether utilities can securitize these assets before equity markets call time on the bet.”

Three Fiscal Fractures Holding Back Deployment

- Liquidity crunch in transmission projects: Superconducting cables require project finance specialists to bundle them with storage and grid upgrades—yet most utilities lack the balance sheets to absorb the $2.5M/km capex. The solution? Special-purpose vehicles (SPVs) with 20-year PPAs, but only 12% of global utilities have signed such deals to date.

- Rare-earth supply chain gridlock: High-temperature superconductors rely on niobium-titanium alloys, with China controlling 85% of refined supply. A single 1GW superconducting link demands 500 tons of niobium—enough to strain even diversified miners. Firms like Anglo American are racing to secure offtake agreements, but price volatility remains a wild card.

- Regulatory fragmentation: Cross-border energy trading—critical for balancing solar/wind surpluses—faces jurisdictional hurdles in 192 countries. The EU’s Clean Energy Package streamlined this for member states, but non-EU grids lack unified frameworks. Legal firms specializing in cross-border energy arbitration are already seeing 40% YoY demand spikes.

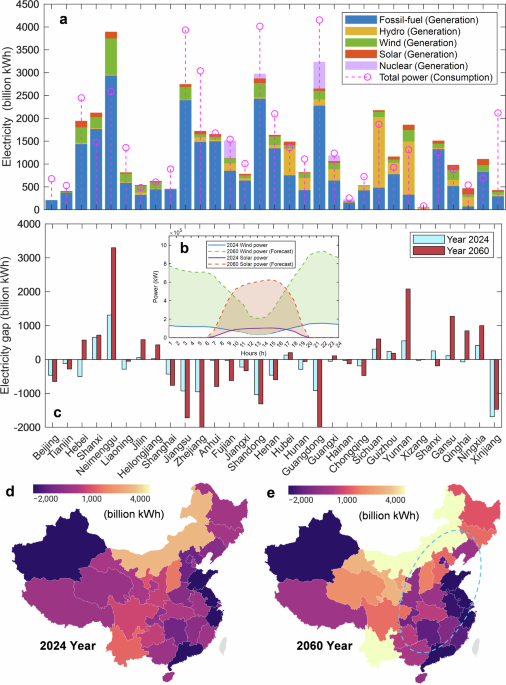

The China Playbook: How the World’s Largest Grid Lab Tests Superconductors

China’s 10,000GW target forces a reckoning: its State Grid Corporation is piloting a 100MW superconducting link in Shanghai, where transmission losses dropped from 8% to 0.5% in tests. But the fiscal hurdle remains. The project’s $1.2B budget—funded via a mix of state-backed loans and green bonds—demonstrates the scale needed. Western utilities, meanwhile, are watching closely but lack China’s NDRC-coordinated supply chains.

“The Shanghai pilot proves the tech works, but the real test is whether European or U.S. Utilities can replicate this with private capital. Right now, the answer is no—unless they find a way to bundle superconductors with carbon credit revenues.”

Directory Bridge: Who Solves These Problems?

For utilities drowning in stranded capacity, the path forward requires:

- Energy storage financiers to package superconducting assets with battery storage for bankable yields.

- Grid modernization consultants to model the real cost savings—beyond the 15% loss reduction—like reduced right-of-way costs and deferred substation builds.

- Carbon credit advisory firms to monetize superconducting links via VCM compliance markets, where a single 1GW link could generate $50M/year in credits.

The 2026-2030 Capital Race: Who Wins?

| Metric | 2025 Baseline | 2030 Projection (With Superconductors) | Fiscal Impact |

|---|---|---|---|

| Global solar/wind capacity (GW) | 1,408 | 5,000+ | +$1.2T in grid upgrades needed |

| Transmission loss reduction | 15% | 0.5% | Saves $300B/year in energy waste |

| Superconductor market size (2030) | $0 | $80B+ | Requires 3x current rare-earth production |

The window to deploy superconducting grids at scale closes in 2030. After that, the marginal cost of adding capacity skyrockets as existing grids hit physical limits. The firms that master the project finance, supply chain, and regulatory puzzle will define the next energy boom—or get left holding the tab for stranded assets. The clock is ticking.