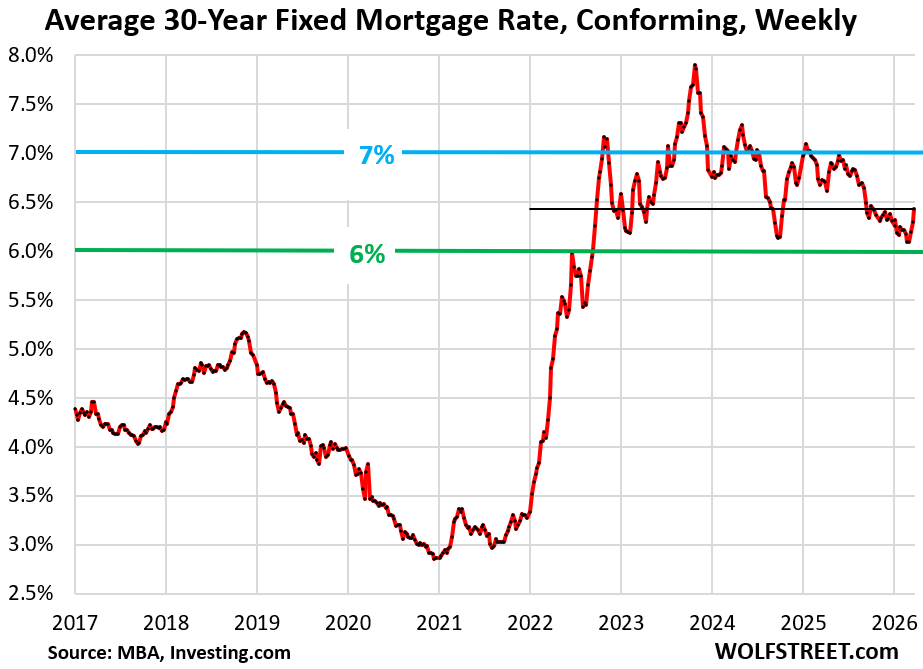

Mortgage Purchase Applications Down 35 Percent in Frozen 2026 Housing Market

Mortgage purchase applications have plummeted 35% since 2019 as average 30-year fixed rates hit 6.43%, the highest since October 2025, effectively freezing the spring selling season. This contraction stems from the Federal Reserve’s unwinding of quantitative easing and persistent inflationary pressures, impacting homebuilders and related financial services. Businesses navigating this downturn require robust risk management and strategic financial planning.

The Anatomy of a Frozen Market

The current situation isn’t simply about higher rates; it’s a confluence of factors. The artificially suppressed rates of the QE era created a housing bubble, inflating prices to unsustainable levels. Now, as the Fed attempts to rein in inflation through quantitative tightening – reducing its balance sheet and raising benchmark interest rates – the housing market is experiencing a painful correction. This isn’t a typical cyclical downturn; it’s a recalibration. The surge in housing supply, with resale inventories at a nine-year high and completed new homes at levels not seen since 2009, exacerbates the problem. Sellers are hesitant to lower prices significantly, creating a standoff. Buyers, meanwhile, are sidelined by affordability concerns.

The Refinance Mirage and its Implications

The brief spikes in refinance applications observed earlier this year were a fleeting phenomenon, triggered by even minor dips in mortgage rates. Homeowners, acutely aware of the potential for higher rates, rushed to lock in lower payments or extract equity. However, these surges were short-lived, quickly extinguished as rates rebounded. The cost of refinancing – typically 1% of the mortgage balance in upfront fees – further diminishes the appeal for many. This volatility underscores the importance of sophisticated financial modeling and advisory services for homeowners and lenders alike.

A Decade of Inverse Correlation

Looking back a decade reveals a clear inverse relationship between mortgage rates and refinance activity. As rates fall, refinance applications surge, and vice versa. This pattern highlights the sensitivity of the housing market to interest rate fluctuations. The current environment, characterized by persistently elevated rates, presents a significant challenge for the industry.

The Builder’s Dilemma: Price Cuts and Inventory Glut

Homebuilders are feeling the pinch acutely. Lennar, a major player in the industry, recently cut its average selling price by 24% to levels last seen in 2017, as reported by Wolf Street. This drastic measure underscores the desperation to move inventory in a market where demand has evaporated. Other builders are likely to follow suit, leading to a broader price correction. This situation demands agile supply chain management and proactive risk mitigation strategies.

“We’re seeing a significant slowdown in demand, particularly among first-time homebuyers. Affordability is the biggest hurdle, and it’s not going to improve anytime soon.” – Robert Dietz, Chief Economist, National Association of Home Builders (Source: NAHB Housing Economics Outlook, March 2026)

The B2B Problem: Navigating a Downturn

This market freeze isn’t just a problem for homeowners and builders; it’s a systemic risk that ripples through the entire financial ecosystem. Mortgage lenders face declining volumes and increased defaults. Title insurance companies are experiencing a slowdown in transactions. Real estate brokers are struggling to close deals. The entire housing finance supply chain is under pressure. Businesses operating in this space need to optimize their operations, manage risk effectively, and explore new revenue streams. Here’s where specialized B2B services become invaluable.

The Impact on Financial Institutions

The decline in mortgage applications directly impacts the profitability of mortgage lenders. Reduced origination fees and increased servicing costs squeeze margins. The risk of defaults rises as borrowers struggle to meet their obligations. Banks and credit unions are tightening lending standards, further restricting access to credit. According to the latest SEC 10-Q filings from Wells Fargo, mortgage banking revenue declined by 18% in Q4 2025, a trend expected to continue throughout 2026.

The Role of Regulatory Compliance

In times of market stress, regulatory scrutiny intensifies. Mortgage lenders must ensure they are fully compliant with all applicable regulations, including Dodd-Frank and the Consumer Financial Protection Bureau’s (CFPB) rules. Navigating this complex regulatory landscape requires specialized expertise. Companies are increasingly turning to specialized financial regulatory law firms to ensure compliance and mitigate legal risks.

The Rise of Fintech Solutions

While the traditional mortgage market struggles, fintech companies are emerging as potential disruptors. These companies are leveraging technology to streamline the mortgage process, reduce costs, and improve the customer experience. However, they also face regulatory challenges and competition from established players.

The Forward-Looking View: A Prolonged Correction

The outlook for the housing market remains bleak. Unless the Federal Reserve reverses course and begins to lower interest rates – a scenario that appears unlikely in the near term – the market is likely to remain frozen for the foreseeable future. The spring selling season, traditionally a period of robust activity, is shaping up to be a disappointment. The key to surviving this downturn lies in adaptability, innovation, and a willingness to embrace new technologies.

Strategic Imperatives for B2B Providers

The current environment presents both challenges and opportunities for B2B providers serving the housing market. Companies that can offer solutions to aid lenders manage risk, streamline operations, and improve compliance will be in high demand. Businesses that can provide data analytics and market intelligence will be invaluable to clients navigating this complex landscape. Consider partnering with leading financial risk management consultants to develop robust strategies for navigating this volatile market.

“We anticipate continued volatility in the mortgage market throughout 2026. Lenders need to focus on efficiency, risk management, and customer retention.” – Michael Barr, Vice Chair for Supervision, Federal Reserve Board (Source: Federal Reserve Board Press Conference, February 2026)

The housing market’s current predicament demands a proactive and informed approach. Don’t navigate this challenging landscape alone. Explore the World Today News Directory to connect with vetted B2B partners specializing in financial services, legal compliance, and technology solutions. Finding the right partners is crucial for weathering this storm and positioning your business for long-term success.