Li Auto delivers 41,053 cars in Mar, stabilizing after tough year

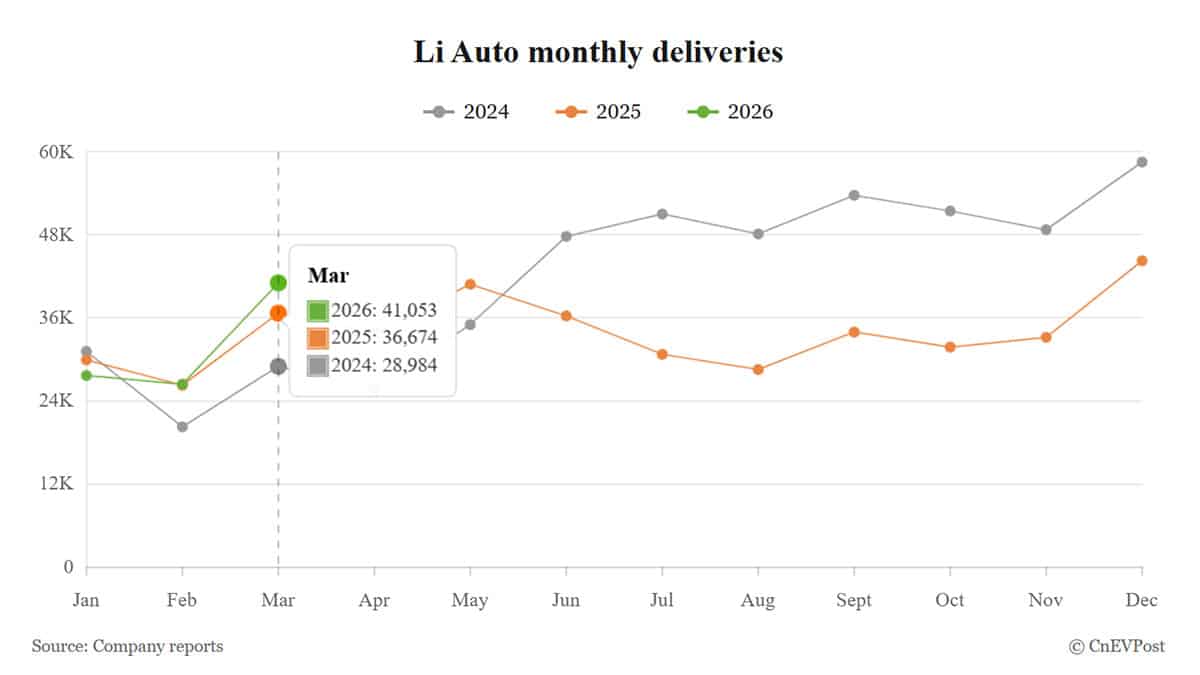

Li Auto delivered 41,053 vehicles in March 2026, a 55% month-over-month surge that signals a operational turnaround following a severe Q4 2025 profitability crunch. While Q1 totals hit 95,142 units, beating guidance, the company faces a critical liquidity test as it deploys a $1 billion buyback to stabilize investor confidence amidst thinning margins.

The Volume Trap: Why Delivery Beats Mask Margin Compression

Wall Street loves a headline number. 41,053 units in a single month looks like a victory lap. Dig deeper into the unit economics, and the picture fractures. Li Auto is moving metal, but the cost of moving that metal has skyrocketed. The resolution of production bottlenecks for the Li i6 electric SUV, which finally surpassed 24,000 units in March, came at a premium. Supply chain friction rarely disappears without a financial penalty, usually absorbed in the form of expedited freight costs or premium component pricing that eats directly into gross margin.

This is the classic volume trap. You sell more to preserve the lights on, but you sell cheaper to acquire the volume. The fourth quarter of 2025 was a bloodbath for the bottom line, with net profit collapsing to a mere 20.2 million yuan against revenue of 28.8 billion yuan. That is a net margin of roughly 0.07%. For a capital-intensive hardware manufacturer, that is effectively breathing through a straw.

The market reaction to the Q1 guidance beat suggests investors are skeptical of the sustainability of this recovery. They want to see EBITDA expansion, not just top-line growth. Until Li Auto can demonstrate that the Li L9 series launch in Q2 can command premium pricing without eroding the brand’s value proposition, the stock remains a speculative hold rather than a growth anchor.

Operational Volatility: A Three-Year Financial Autopsy

To understand the severity of the 2025 slump and the significance of the 2026 rebound, one must appear at the delivery volatility over the last thirty-six months. The data reveals a company that overextended during the 2024 peak and spent the entirety of 2025 contracting to survive.

| Metric | 2024 Peak (Sept) | 2025 Trough (Aug) | 2026 Recovery (Mar) | Delta (Trough to Recovery) |

|---|---|---|---|---|

| Monthly Deliveries | 53,709 | 28,529 | 41,053 | +43.9% |

| Q1 Total Volume | N/A (Historical) | ~86,000 (Est.) | 95,142 | +10.6% |

| Guidance vs. Actual | Met | Missed | Exceeded (Upper End) | Positive Variance |

The table above illustrates a violent contraction followed by a sharp V-shaped recovery. However, notice the gap between the 2024 peak and current 2026 numbers. Li Auto has not yet returned to its maximum throughput capacity. This suggests that while the bleeding has stopped, the patient is still in rehabilitation. The 12% year-on-year increase for March 2026 is healthy, but it pales in comparison to the hyper-growth rates seen in the sector during the 2023-2024 electrification boom.

Production bottlenecks were the primary culprit for the 2025 underperformance. Resolving these issues requires more than just hiring more line workers; it demands a complete overhaul of vendor management and logistics synchronization. Companies facing similar supply chain fragility often turn to specialized supply chain optimization firms to re-engineer their procurement workflows. For Li Auto, the 55% jump from February to March indicates that these operational fixes are finally bearing fruit, but the lag time cost them a full year of market share.

Capital Allocation and the $1 Billion Lifeline

Cash is the only metric that matters in a downturn. Li Auto ended 2025 with 101.2 billion yuan in cash reserves. That is a formidable war chest, but it is not infinite. The decision to authorize a $1 billion share buyback program is a defensive maneuver designed to put a floor under the stock price. It signals to the market that management believes the equity is undervalued, but it also drains liquidity that could be used for R&D or expansion.

“The buyback is a necessary signal, but it doesn’t fix the underlying margin compression. Investors need to see a path to 15% gross margins before they re-rate the stock. Until then, this is a value trap disguised as a turnaround.” — Marcus Thorne, Senior Analyst, Global Auto Equity Research

The buyback strategy highlights a broader issue in the EV sector: the transition from growth-at-all-costs to profitability discipline. As valuations compress, companies are forced to engage with investor relations specialists to communicate a more mature narrative to institutional holders. Li Auto’s first buyback since its 2020 US listing marks a shift in corporate maturity, acknowledging that share price stability is now as critical as delivery volume.

However, capital allocation decisions of this magnitude require rigorous stress testing. With an operating loss of 442.6 million yuan in Q4 2025, the company is walking a tightrope. The upcoming launch of the Li L9 series in Q2 2026 is the catalyst that will determine if this buyback was a smart investment or a waste of precious cash. If the L9 fails to capture the flagship SUV market, the company may discover itself needing to raise capital in a hostile environment, likely consulting with capital markets advisory firms to structure debt or equity offerings that won’t further dilute existing shareholders.

The Road Ahead: Infrastructure as the Moat

Beyond the balance sheet, Li Auto’s physical footprint remains its strongest defensive moat. As of March 31, 2026, the company operates 517 retail stores and 4,057 super charging stations. In the EV game, hardware is a commodity; the network is the product. Competitors can copy a battery pack in six months. They cannot copy a charging network in six years.

This infrastructure density supports the 20% annual growth target for 2026. But maintaining 4,057 charging stations requires significant operational expenditure. The efficiency of these assets—uptime, energy cost management, and location optimization—will directly impact the company’s long-term free cash flow. The stabilization seen in March is a good start, but the fiscal year is only one quarter old. The real test begins when the Li L9 hits the showroom floor and the market decides if Li Auto is a recovery play or a relic of the previous cycle.

For B2B partners watching this space, the lesson is clear: volatility creates opportunity. Whether it is legal counsel for restructuring, logistics firms for bottleneck resolution, or IR firms for narrative control, the companies that solve Li Auto’s efficiency problems will be the ones riding the next wave of profitability.