Heat Wave Hits Philippines: Temperatures Soar to Dangerous 47°C Across Multiple Regions

On April 26, 2026, a severe heatwave struck multiple provinces across the Philippines, pushing the heat index to dangerous levels above 42°C and triggering public health emergencies, power grid strain, and agricultural disruption in a nation already vulnerable to climate extremes. This event underscores how climate-driven shocks are no longer isolated environmental concerns but systemic threats to global supply chains, labor productivity, and foreign investment stability in Southeast Asia — a region responsible for over 30% of global electronics manufacturing and a critical node in maritime trade routes.

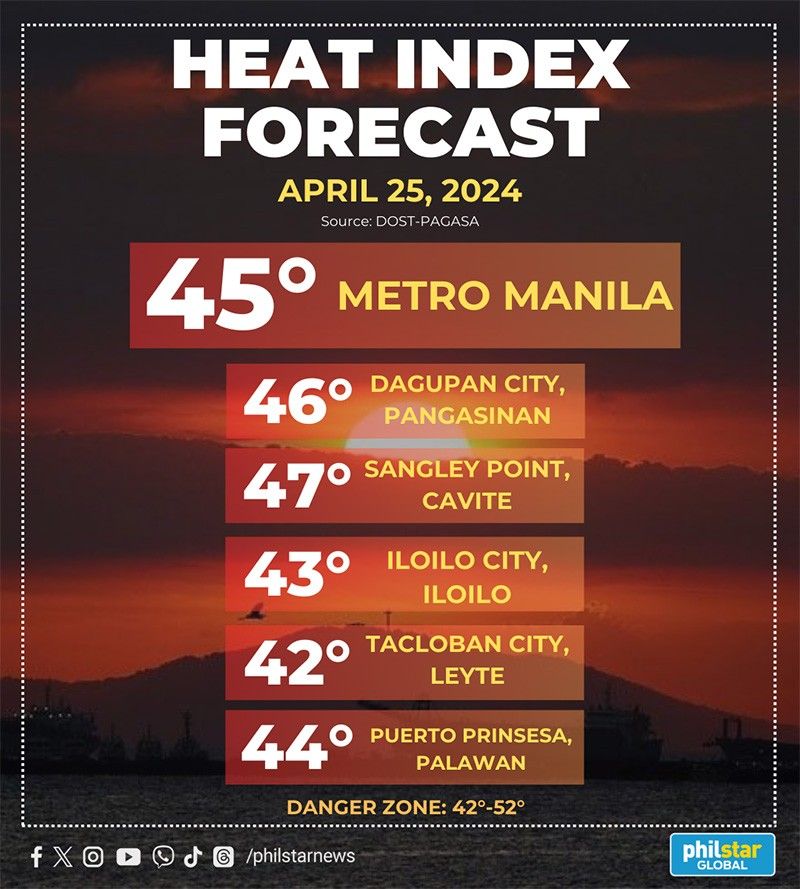

The Philippines, an archipelago of over 7,000 islands, faces acute exposure to rising temperatures due to its geographic location in the Western Pacific typhoon belt and limited adaptive infrastructure. Historical data from the Philippine Atmospheric, Geophysical and Astronomical Services Administration (PAGASA) shows that the frequency of days exceeding 35°C has increased by 40% since 2000, with urban heat islands in Metro Manila and Cebu amplifying risks. The current heatwave, driven by a persistent high-pressure system over the South China Sea, has pushed temperatures in Luzon and Visayas to 47°C, exceeding human survivability thresholds without artificial cooling.

How Climate Stress Tests Global Manufacturing Resilience

Extreme heat directly disrupts labor-intensive industries that form the backbone of Philippine exports. Electronics manufacturers in special economic zones like Cavite and Batangas report reduced worker output during peak heat hours, with some firms shifting to night operations to maintain output. According to the World Bank, heat stress could reduce global GDP by up to 10% by 2050, with Southeast Asia bearing a disproportionate share due to high humidity and reliance on outdoor labor. For multinational firms reliant on Philippine-based assembly lines — particularly in semiconductors, automotive parts, and medical devices — prolonged heat exposure increases the risk of production delays, quality control failures, and supply chain fragmentation.

This is not merely a local issue. The Philippines accounts for 8% of global semiconductor packaging and testing capacity, a sector where even minor disruptions ripple through global tech supply chains. When combined with concurrent heat stress in Vietnam and Thailand, regional manufacturing capacity faces compounded strain. Logistics providers must now factor in climate volatility when designing resilient routes, prompting increased demand for adaptive warehousing, real-time environmental monitoring, and heat-resilient transportation protocols.

“Climate adaptation is no longer a corporate social responsibility footnote — it’s a core supply chain imperative. Firms that ignore heat stress in their operational planning are betting against physics.”

The Investment Risk Premium in a Warming Archipelago

Foreign direct investment (FDI) inflows to the Philippines have shown volatility in recent years, averaging $10 billion annually but highly sensitive to perceived operational risk. The 2023–2024 period saw a 15% decline in new greenfield investments in manufacturing, partly attributed to infrastructure concerns and natural disaster exposure. Heatwaves exacerbate these concerns by increasing energy demand — during the April 2026 event, peak electricity load surged to 14,200 MW, nearing the grid’s 15,000 MW capacity — leading to rolling brownouts in industrial zones.

Energy-intensive industries face dual pressure: rising cooling costs and unreliable power. This creates a growing market for decentralized energy solutions, including solar-plus-storage microgrids and demand-response systems. Simultaneously, insurers are reassessing risk models, with property and business interruption premiums rising 8–12% in high-exposure zones. Investors now require climate resilience audits as part of due diligence, driving demand for specialized advisory services.

Multinational corporations navigating this landscape increasingly turn to firms that specialize in climate-risk-adjusted site selection, infrastructure hardening, and ESG-compliant operational planning. These advisors help clients evaluate not just current conditions but long-term climate projections under RCP 4.5 and 8.5 scenarios, ensuring capital allocation aligns with physical reality.

“The new frontier of due diligence isn’t just financial or legal — it’s climatic. Investors who don’t model heat stress, flood risk, and sea-level rise are pricing assets blind.”

Geopolitical Ripples: From Manila to the Malacca Strait

The Philippines’ strategic position along the eastern edge of the South China Sea makes it a linchpin in Indo-Pacific security and trade. Approximately 60% of global maritime trade by value passes through waters adjacent to the archipelago, including critical chokepoints like the San Bernardino Strait and the Mindoro Strait. Climate-induced instability — whether through mass migration from rural areas, increased disaster relief burdens on the state, or social unrest linked to resource scarcity — could indirectly affect regional security dynamics.

While no direct link exists between heatwaves and territorial disputes, prolonged environmental stress can strain government capacity to maintain maritime patrols or invest in defense modernization. The Philippines’ 2026 defense budget remains constrained at $4.2 billion, with over 60% allocated to personnel costs, limiting modernization of its naval and air capabilities. This creates openings for external actors to exploit perceived vacuums, though the country’s Enhanced Defense Cooperation Agreement (EDCA) with the United States and trilateral patrols with Japan and Australia continue to provide a stabilizing presence.

Nonetheless, climate resilience is becoming a silent pillar of national security. Forward-thinking defense planners now advocate for hardening bases against extreme weather, ensuring water and power continuity during disasters, and integrating climate data into mission readiness assessments. This opens avenues for specialized contractors in military logistics, disaster-resilient infrastructure, and environmental intelligence services.

| Indicator | Pre-Heatwave (April 2025) | During Heatwave (April 2026) | Change |

|---|---|---|---|

| Average Daily Temperature (Metro Manila) | 31.2°C | 38.7°C | +24% |

| Peak Electricity Demand (National Grid) | 12,100 MW | 14,200 MW | +17% |

| Reported Heat-Related Illnesses (DOH) | 1,200 cases/week | 8,900 cases/week | +642% |

| Manufacturing Output Utilization (PEZA Zones) | 84% | 71% | -15% |

The human toll is immediate and severe. The Department of Health reported over 35,000 heat-related cases nationwide during the week of April 20–26, 2026, with elderly outdoor workers and urban poor disproportionately affected. Schools suspended in-person classes in 12 provinces, and the Department of Labor issued advisories for modified work hours in construction, agriculture, and outdoor services. These measures, while necessary, reduce economic output and increase informal sector vulnerability.

Long-term adaptation requires systemic investment: urban greening, reflective building materials, expanded access to cooling centers, and grid modernization. The Philippine government’s 2025–2030 Climate Change Action Plan allocates ₱1.2 trillion ($21 billion) for adaptation, but implementation lags due to bureaucratic fragmentation and limited local government capacity. International climate finance — including the Green Climate Fund and World Bank’s Climate-Smart Agriculture initiative — remains critical to scaling solutions.

For global businesses, the message is clear: climate risk is operational risk. The firms that will thrive in the coming decade are not those with the lowest labor costs, but those that build resilience into their supply chains from the ground up. In other words partnering with experts who can model future conditions, design adaptive infrastructure, and navigate the complex web of local regulations, international standards, and climate finance mechanisms.

As the planet warms, the competitive advantage will shift from cost efficiency to adaptive capacity. The winners will be those who treat climate not as a peripheral ESG checkbox, but as a central variable in location strategy, supplier selection, and capital planning.

To navigate this new reality, multinational operators need trusted advisors who speak the language of both meteorology and balance sheets. They require climate risk consultants who can translate IPCC scenarios into site-specific action plans, infrastructure resilience engineers who design facilities to withstand 47°C heatwaves and grid instability, and international trade lawyers who ensure compliance with evolving ESG disclosure regimes across jurisdictions. These are not optional extras — they are the architects of continuity in an era of planetary disruption.