Employer-Sponsored Health Insurance: 2025 Coverage and Eligibility Analysis

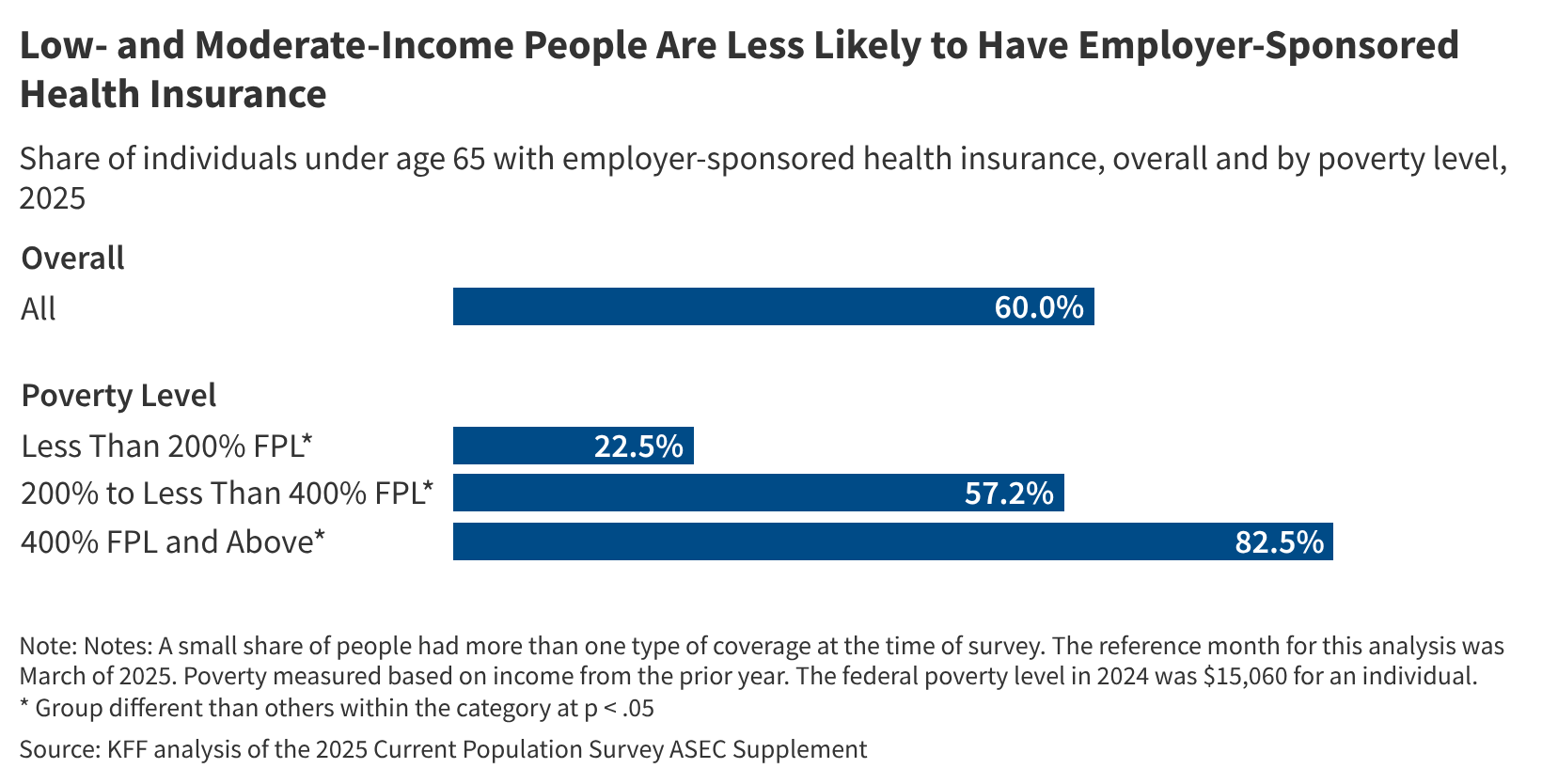

Employer-sponsored health insurance remains the cornerstone of coverage for working-age Americans, with 165.6 million individuals under 65 enrolled as of March 2025, according to the Annual Economic and Social Supplement of the Current Population Survey. Yet beneath this aggregate stability lie shifting patterns in access, affordability, and equity that demand clinical and public health scrutiny. As healthcare costs continue to outpace wage growth and chronic disease prevalence rises, understanding who gains coverage—and who falls through the cracks—has become essential for employers, policymakers, and providers seeking to mitigate long-term morbidity and systemic inefficiencies.

Key Clinical Takeaways:

- Employer-based coverage declined slightly among low-wage and part-time workers between 2023 and 2025, widening disparities in preventive care access.

- Mental health and chronic disease management benefits are increasingly standardized in large-group plans, driven by federal parity rules and employer ROI calculations.

- Geographic variation in offer rates persists, with Southern and Western states lagging behind Northeast and Midwest regions in eligibility expansion.

The data reveal a nuanced landscape: while large firms (200+ employees) maintain near-universal offer rates at 98.4%, small businesses (<50 employees) saw offer rates dip from 54.1% in 2022 to 51.7% in 2025, per the Kaiser Family Foundation’s Employer Health Benefits Survey. This trend disproportionately affects service-sector workers, where fluctuating hours and multiple jobholding reduce eligibility thresholds. As Dr. Elena Rodriguez, epidemiologist at the Johns Hopkins Bloomberg School of Public Health, notes, “When employment-based coverage erodes in low-wage sectors, we see delayed diagnosis of hypertension and diabetes—conditions where early intervention reduces long-term morbidity by up to 40%.”

Funded by the Agency for Healthcare Research and Quality (AHRQ) under grant HS026381, the analysis links declining offer rates in small firms to administrative burden and premium volatility rather than lack of interest. Employers cite rising costs—averaging $8,435 annually for single coverage in 2025—as the primary barrier, yet 68% of firms offering coverage now include telehealth and wellness programs, reflecting a shift toward value-based design. “Employers aren’t abandoning coverage; they’re recalibrating it,” explains Dr. Marcus Chen, health economist at the University of Michigan’s School of Public Health. “The real innovation is in integrating preventive services directly into workplace wellness platforms to reduce downstream claims.”

These trends have tangible implications for clinical care. Gaps in employer-based coverage correlate with lower rates of cancer screening and statin adherence, particularly among Hispanic and Black workers in retail and hospitality industries. For patients navigating fragmented access, continuity of care becomes critical. Individuals experiencing lapses in coverage due to job transitions or hourly instability benefit from coordinated re-engagement strategies—services increasingly provided by vetted primary care physicians who specialize in managing chronic conditions amid socioeconomic flux. Similarly, employers seeking to stabilize their benefits architecture while complying with ERISA and ACA mandates often consult healthcare compliance attorneys to audit plan design and avoid costly noncompliance penalties.

Looking ahead, the integration of biosimilars and value-based insurance design (VBID) into employer plans may redefine cost-effectiveness benchmarks. Early adopters report 11–15% reductions in specialty drug spending without compromising access, per a 2024 study in Health Affairs. As these models scale, the role of occupational health clinics and board-certified occupational medicine specialists will grow—not merely as gatekeepers of clearance exams, but as strategists in workforce health optimization. The future of employer-based coverage lies not in reversing decline, but in refining its precision: aligning benefit structures with epidemiological risk to improve both population health outcomes and organizational resilience.

*Disclaimer: The information provided in this article is for educational and scientific communication purposes only and does not constitute medical advice. Always consult with a qualified healthcare provider regarding any medical condition, diagnosis, or treatment plan.*