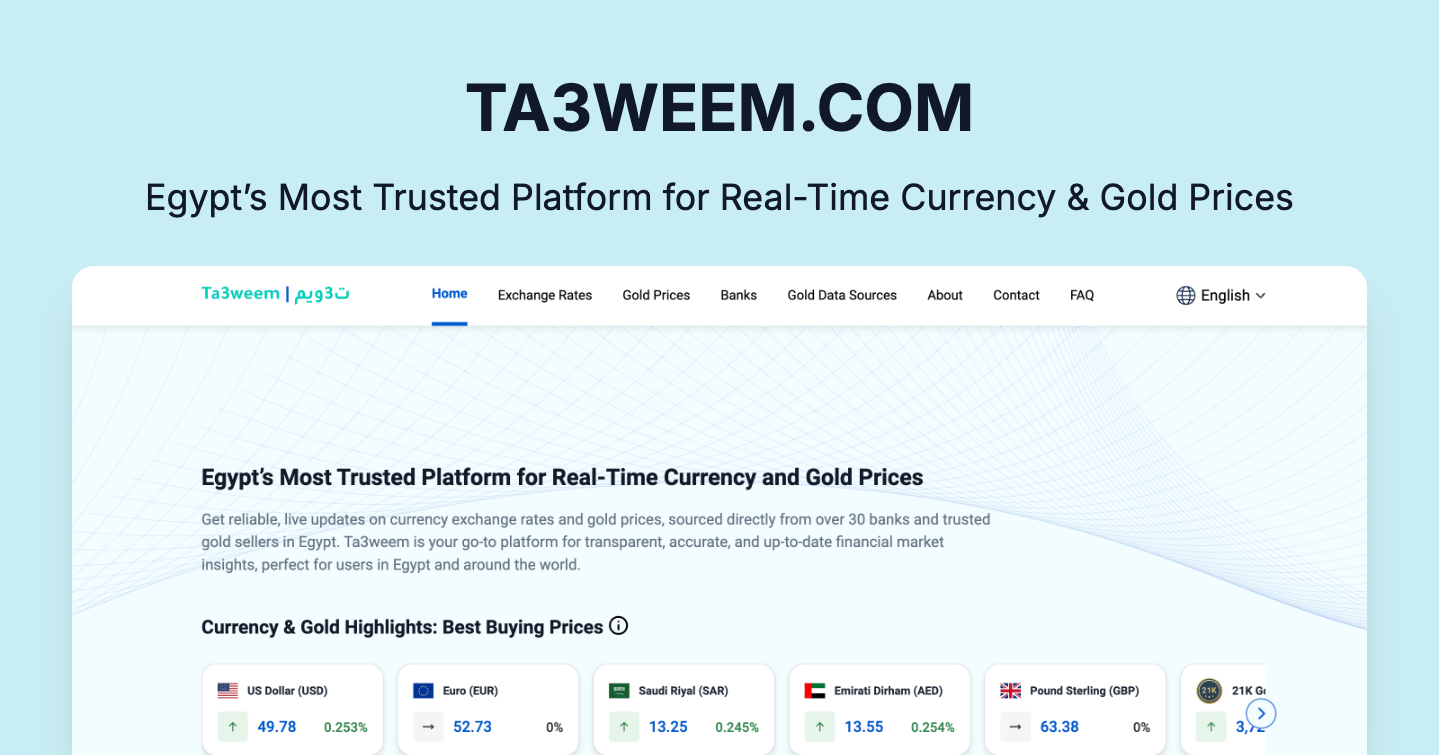

Dollar Exchange Rate in Egypt Today: Updates & Latest Prices

The Central Bank of Egypt (CBE) has anchored the USD/EGP buying price at 52.75 as of March 28, 2026, signaling a stabilization attempt amidst rising global liquidity pressures. This fixed rate, released ahead of the weekend trading halt, reflects a strategic divergence from the parallel market, creating immediate friction for import-dependent sectors. For multinational corporations operating in Cairo, this spread represents a critical variance in cost-of-goods-sold (COGS) projections for the upcoming fiscal quarter.

The official peg at 52.75 EGP per dollar is not merely a number. it is a fiscal firewall. While the headline suggests stability, the underlying mechanics reveal a tightening liquidity trap. Importers facing the Q2 earnings season are now forced to navigate a dual-track reality: the sanitized official rate for government transactions and the volatile street rate for private procurement. This bifurcation forces treasury departments to reassess their exposure to foreign exchange risk, often necessitating immediate engagement with specialized forex hedging and risk management firms to lock in forward contracts before the spread widens further.

The Mechanics of the March 2026 Correction

We are witnessing a classic emerging market response to a strengthening dollar index (DXY). The CBE’s intervention is designed to preserve foreign reserves, but it comes at the cost of local liquidity. When a central bank absorbs dollars to maintain a specific price point, it effectively drains local currency from the banking system. This contraction pushes interbank lending rates higher, increasing the cost of capital for Egyptian SMEs and large conglomerates alike. The result is a slowdown in domestic consumption, as credit becomes prohibitively expensive for the extremely businesses driving GDP growth.

To understand the trajectory of the Egyptian pound through Q2 2026, we must isolate three specific macro-drivers currently distorting the valuation:

- Debt Service Obligations: Egypt faces a significant wall of sovereign debt maturities in the second half of 2026. The CBE is prioritizing reserve accumulation to meet these obligations without triggering a default event. This defensive posture limits the amount of hard currency available for commercial imports, creating artificial scarcity that drives up the effective cost of goods for private sector players.

- The Federal Reserve’s 2026 Stance: With US inflation proving stickier than anticipated in early 2026, the Federal Reserve has maintained a “higher-for-longer” interest rate environment. This strengthens the dollar globally, pulling capital away from emerging markets like Egypt. The yield differential between US Treasuries and Egyptian sovereign bonds has narrowed, reducing the incentive for foreign portfolio investment in local debt instruments.

- Supply Chain Repricing: Global shipping costs have surged due to geopolitical tensions in the Red Sea corridor. Egyptian importers are paying a premium in USD for logistics, which compounds the pressure on the exchange rate. Companies unable to hedge this exposure are seeing their margins erode by 15-20% quarter-over-quarter, forcing many to seek supply chain logistics and consulting partners to reroute shipments and negotiate better freight terms.

Corporate Strategy in a Volatile FX Environment

The divergence between the 52.75 official rate and the market reality creates a compliance nightmare for foreign investors. Multinationals booking revenue in EGP but repatriating profits in USD face a valuation gap that can wipe out quarterly earnings. This is no longer a theoretical risk; it is a balance sheet liability. CFOs across the region are shifting focus from growth to preservation, prioritizing cash flow stability over expansion.

“The 52.75 handle is a psychological anchor, not a market equilibrium. Until we see a normalization of foreign direct investment (FDI) inflows, the liquidity premium on the Egyptian pound will remain elevated. Corporations must treat FX exposure as a primary operational risk, not a back-office accounting issue.”

This sentiment echoes the warnings issued by senior analysts at major emerging market funds. The consensus is clear: volatility is the new baseline. Businesses that fail to adapt their procurement strategies to this reality will find themselves insolvent by year-end. The solution lies in diversification—sourcing locally where possible and utilizing complex financial instruments to mitigate currency risk.

the regulatory landscape is shifting. The CBE has signaled stricter enforcement on import documentation to curb capital flight. This bureaucratic tightening means that even companies with access to dollars at the official rate face delays. To navigate this, firms are increasingly turning to corporate law and regulatory compliance experts who specialize in Egyptian trade law. These firms provide the necessary due diligence to ensure that import licenses are processed without triggering regulatory red flags that could freeze assets.

Outlook: The Q2 Liquidity Crunch

Looking ahead to April and May, the pressure on the pound is unlikely to dissipate. The seasonal demand for dollars typically peaks in Q2 as agricultural imports and energy payments come due. If the CBE continues to defend the 52.75 level aggressively, we expect to see a further contraction in credit availability. Banks will become more risk-averse, tightening lending standards for any business with significant FX exposure.

For the astute investor, this environment presents opportunities in sectors that are naturally hedged against currency devaluation, such as export-oriented manufacturing and tourism. However, for the broader market, the message is one of caution. The era of easy liquidity in Cairo is over. Survival depends on agility, robust risk management frameworks, and partnerships with B2B service providers who understand the nuances of this specific fiscal crisis.

The market does not forgive hesitation. As we move deeper into 2026, the gap between the official rate and the economic reality will define the winners and losers in the Egyptian corporate landscape. Those who secure their supply chains and hedge their currency exposure now will weather the storm; those who wait for stability will be left holding devalued assets.