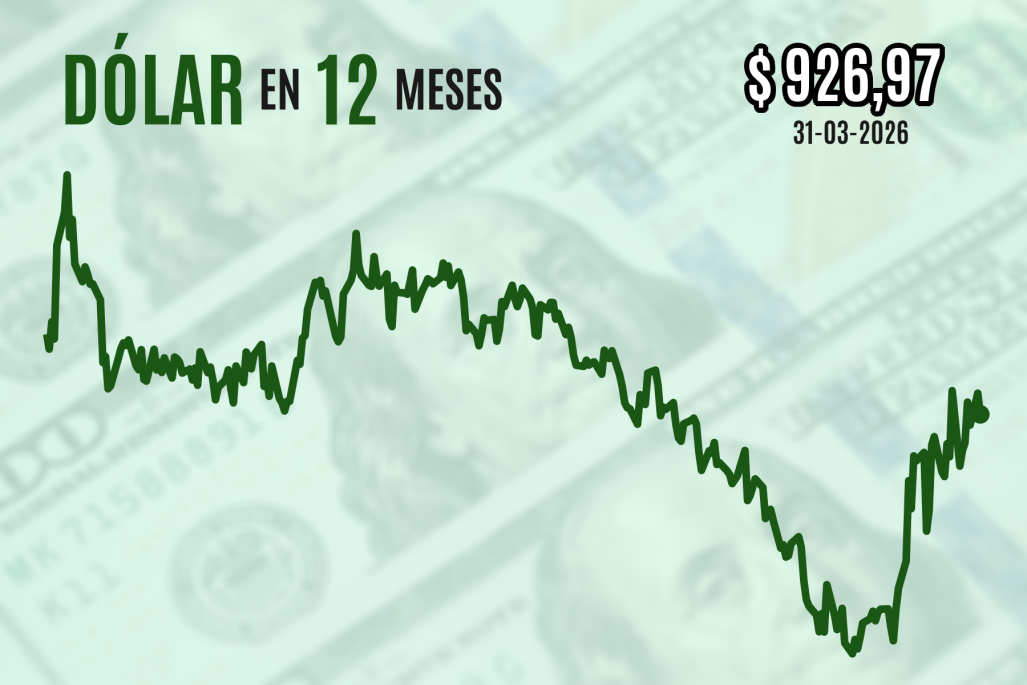

Dólar cierra a la baja este martes, pero sube más de $ 50 en un marzo sacudido por la guerra de Irán

The Chilean peso staged a tactical recovery on Tuesday, closing at 927 CLP/USD, as markets priced in a potential de-escalation of the Iran conflict following reports of White House flexibility. Despite this daily dip, the currency remains battered, having shed over 50 pesos in March—the steepest monthly decline since late 2024—driven by a historic 44% surge in global energy prices and sustained geopolitical risk premiums.

Volatility is the latest baseline. Whereas the intraday retracement offers momentary relief for treasury departments, the structural damage to Q1 margins for energy-dependent importers is already locked in. The market is currently oscillating between fear of a Strait of Hormuz closure and hope for a diplomatic off-ramp, creating a hazardous environment for corporate planning. For CFOs navigating this turbulence, the focus must shift from reactive trading to structural hedging strategies.

The Macro Drivers: Decoding the Tuesday Reversal

The intraday pivot was not driven by domestic fundamentals but by external geopolitical signaling. A report from The Wall Street Journal indicated that the Trump administration is willing to decouple peace negotiations from the immediate reopening of the Strait of Hormuz. This nuance lowered the perceived probability of a total energy blockade, allowing risk assets to breathe.

Though, treating this as a trend reversal is premature. The underlying mechanics of the March sell-off remain intact. To understand the trajectory for Q2, we must isolate the three specific vectors currently distorting the USD/CLP pair:

- Geopolitical Risk Premium Compression: The Dollar Index (DXY) shed 0.6% as the VIX volatility index stabilized. Investors are betting on a resolution within the four-to-six-week window outlined by the White House, reducing the safe-haven bid for the greenback.

- Energy Pass-Through Inflation: Brent crude retreated 2.5% to $104.70, yet remains critically elevated. For Chile, a net energy importer, every dollar sustained above $100 directly erodes the terms of trade, forcing the Central Bank to maintain a restrictive stance that supports the dollar.

- Yield Curve Normalization: U.S. Treasury yields relaxed, narrowing the interest rate differential that had previously fueled carry-trade flows into the peso. As liquidity tightens globally, emerging market currencies lose their yield advantage.

This triad of factors suggests that while the panic selling has paused, the fundamental pressure on the peso remains bearish until energy prices structurally decouple from the conflict zone.

EBITDA Erosion and the Hedging Imperative

The 53.6-peso monthly appreciation of the dollar is not merely a headline figure. This proves a direct hit to the bottom line for Chilean industrial firms. According to the Q1 2026 Monetary Policy Report from the Central Bank of Chile (BCCh), import price inflation has accelerated to an annualized rate of 18%, primarily driven by fuel and intermediate goods.

For mid-market manufacturers, this creates an immediate liquidity crunch. Companies that failed to lock in forward contracts in January are now facing margin compression of up to 400 basis points. The window for reactive hedging has closed; the focus must now turn to balance sheet resilience.

“We are seeing a bifurcation in the market. Companies with sophisticated treasury functions are surviving the shock, while those relying on spot rates are facing existential cash flow threats. The volatility in March was a stress test that many failed.”

— Elena Rossi, Chief Investment Officer at Andes Capital Management

To mitigate this exposure, corporate treasurers are increasingly turning to specialized forex risk management firms to restructure their derivative portfolios. The goal is no longer speculation but survival, utilizing non-deliverable forwards (NDFs) to cap exposure without tying up excessive working capital.

Supply Chain Contingency and Legal Force Majeure

Beyond the currency impact, the physical threat to logistics remains acute. The Iranian Revolutionary Guard’s announcement targeting U.S. Companies in the region introduces a new layer of operational risk. Even with the recent diplomatic thaw, the Strait of Hormuz remains a choke point for 20% of global oil consumption.

Supply chain directors must assume that disruption is a matter of ‘when,’ not ‘if.’ The 44% year-to-date spike in energy costs is a leading indicator of broader freight inflation. As bunker fuel surcharges rise, shipping lines will pass costs downstream, impacting the landed cost of goods from Asia and Europe.

Proactive organizations are already engaging supply chain logistics consultants to model alternative routing scenarios that bypass the Middle East entirely. While more expensive, the cost of insurance and delay often outweighs the premium of longer transit times via the Cape of Good Hope.

the legal implications of this conflict are triggering a wave of contract renegotiations. Force majeure clauses related to “acts of war” are being tested as Iranian threats expand to include commercial entities. Corporate legal teams are scrambling to validate these claims before disputes escalate to arbitration.

Engaging international trade law specialists is now critical to navigate the complex web of U.S. Sanctions and potential retaliatory measures. A misstep in compliance could result in assets being frozen or secondary sanctions being applied, a risk that far exceeds currency volatility.

Q2 Outlook: The Calm Before the Storm?

Market strategists at Scotiabank note that while equity markets are rallying, the bond market remains skeptical. The divergence between rising stock prices and elevated volatility suggests investors are complacent. If the four-to-six-week diplomatic timeline slips, we could notice a violent repricing of risk assets.

The Tuesday close at 927 CLP is a breather, not a recovery. For the remainder of Q2, the Chilean peso will likely trade in a wide band, dictated by the hourly news cycle from Tehran and Washington. Businesses that treat this as a temporary blip rather than a structural shift in the global risk landscape do so at their own peril.

The World Today News Directory continues to track these shifts, connecting enterprises with the vetted B2B partners necessary to navigate this high-stakes environment. In a market defined by uncertainty, the only viable strategy is preparation.