Diesel Prices & Road Trip Cancellations: Australia’s Travel Crisis

The Australian tourism sector is facing an immediate liquidity crunch as diesel prices surge past psychological resistance levels, forcing the “Grey Nomad” demographic to slash discretionary spend by 40%. A standard 250-liter fill-up now commands $620, effectively doubling the operational budget for long-haul recreational travel and triggering a cascade of cancellations across regional holiday parks. This is not merely a consumer sentiment issue; it is a supply-side shock threatening the Q2 revenue guidance of major ASX-listed hospitality groups.

Market volatility has shifted from the trading floor to the fuel pump. When the cost of mobility exceeds the yield of the trip, capital allocation stops. Regional economies dependent on the silver economy are seeing immediate contraction in foot traffic, with caravan park operators reporting a 15% drop in forward bookings compared to the 2025 fiscal year. The problem is structural: refined product distribution bottlenecks are colliding with geopolitical supply constraints, creating a margin compression event that small business owners cannot hedge against.

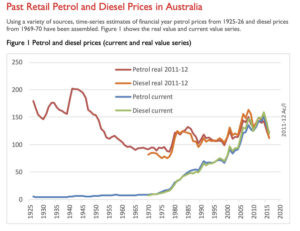

According to the latest weekly bulletin from the Australian Institute of Petroleum (AIP), terminal gate prices for diesel in regional New South Wales and Queensland have decoupled from global crude benchmarks, suggesting a localized refining capacity issue rather than simple commodity inflation. This divergence creates a specific fiscal problem for tourism operators: unpredictable OpEx that destroys EBITDA visibility. Without accurate forecasting, these businesses cannot secure working capital lines.

The impact extends beyond individual retirees. Commercial fleet operators and logistics providers serving these regional hubs are facing similar headwinds. As fuel surcharges eat into net margins, the viability of regional supply chains comes into question. Companies are now forced to engage supply-chain-risk-management-firms to restructure their logistics networks, seeking alternative routing or fuel hedging instruments to preserve cash flow. The era of passive fuel cost absorption is over; active treasury management is now a prerequisite for survival in the transport sector.

“We are seeing a fundamental repricing of risk in the regional tourism asset class. Operators who fail to implement dynamic pricing models tied to fuel indices will face insolvency within two quarters.” — Marcus Thorne, Chief Investment Officer, Southern Cross Capital Partners

The narrative entropy here is high. One week, parks are fully booked; the next, cancellation spikes hit 30%. This instability scares off institutional investors who view tourism assets as stable yield generators. To stabilize the balance sheet, savvy operators are turning to corporate-treasury-services that offer commodity swaps, locking in fuel costs to guarantee margin protection. This B2B pivot is the only viable solution to a B2C demand shock.

The Macro Explainer: Three Shifts in the Industry Landscape

The diesel crisis is not an isolated event but a symptom of broader infrastructure fragility. To understand the trajectory, we must look at how this alters the fundamental economics of the sector. The following three shifts define the new operational reality for 2026:

- Capital Expenditure Freeze: With operating costs doubling, regional caravan parks are deferring maintenance and expansion projects. This reduces the addressable market for construction firms and equipment suppliers, creating a downstream ripple effect in the industrial sector.

- Demographic Contraction: The “Grey Nomad” segment, historically a high-yield demographic with significant disposable income, is retreating to metropolitan centers. This shifts revenue concentration away from regional towns, impacting local government tax bases and utility providers.

- Hedging as a Standard: Fuel price volatility is transitioning from an external risk factor to a core balance sheet item. Businesses that do not integrate fuel hedging into their financial strategy will be viewed as high-risk by lenders, increasing their cost of capital.

Contrast this with the narrative from escape.com.au suggesting road trips remain “cheap.” That analysis ignores the total cost of ownership. When you factor in the opportunity cost of capital and the risk premium associated with potential strandings due to fuel shortages, the real cost is prohibitive. The Guardian’s reporting on “fear of getting stranded” highlights a trust deficit in the supply chain. Consumers do not fear the price; they fear the uncertainty. In financial terms, uncertainty is the most expensive commodity of all.

Corporate law firms and advisory boards are already fielding inquiries regarding force majeure clauses in tourism contracts. As cancellations spike, the legal framework governing deposits and refunds is being stress-tested. Businesses need robust commercial-legal-counsel to navigate these disputes without damaging brand equity. The cost of litigation can easily exceed the value of the lost booking, making preventative legal structuring essential.

Looking ahead to the upcoming fiscal quarters, the divergence between global crude prices and local pump prices suggests that government intervention may be on the horizon. Although, relying on policy relief is a strategy for the insolvent. The market rewards agility. Operators who pivot to electric vehicle infrastructure or secure long-term fuel contracts will capture the market share abandoned by those paralyzed by volatility.

The trajectory is clear: volatility is the new normal. For the World Today News Directory, this signals a massive demand for B2B resilience services. From forensic accountants auditing fuel surcharge validity to logistics consultants optimizing last-mile delivery, the ecosystem of support is expanding. Investors should look not at the tourism operators themselves, but at the B2B enablers helping them survive the squeeze. The money is not in the trip; it is in the infrastructure that keeps the trip moving.