DAX Update: Middle East Peace Plan & 23,000 Point Mark – Access Denied

German DAX futures briefly surged past 23,000 points on Wednesday, fueled by tentative optimism surrounding a potential ceasefire in the Middle East, but gains proved unsustainable as geopolitical anxieties and persistent inflation concerns reasserted themselves. The initial rally highlighted market sensitivity to global stability, whereas the subsequent pullback underscores the fragility of current valuations and the need for robust risk management strategies. This volatility creates immediate challenges for multinational corporations reliant on stable supply chains and predictable energy costs.

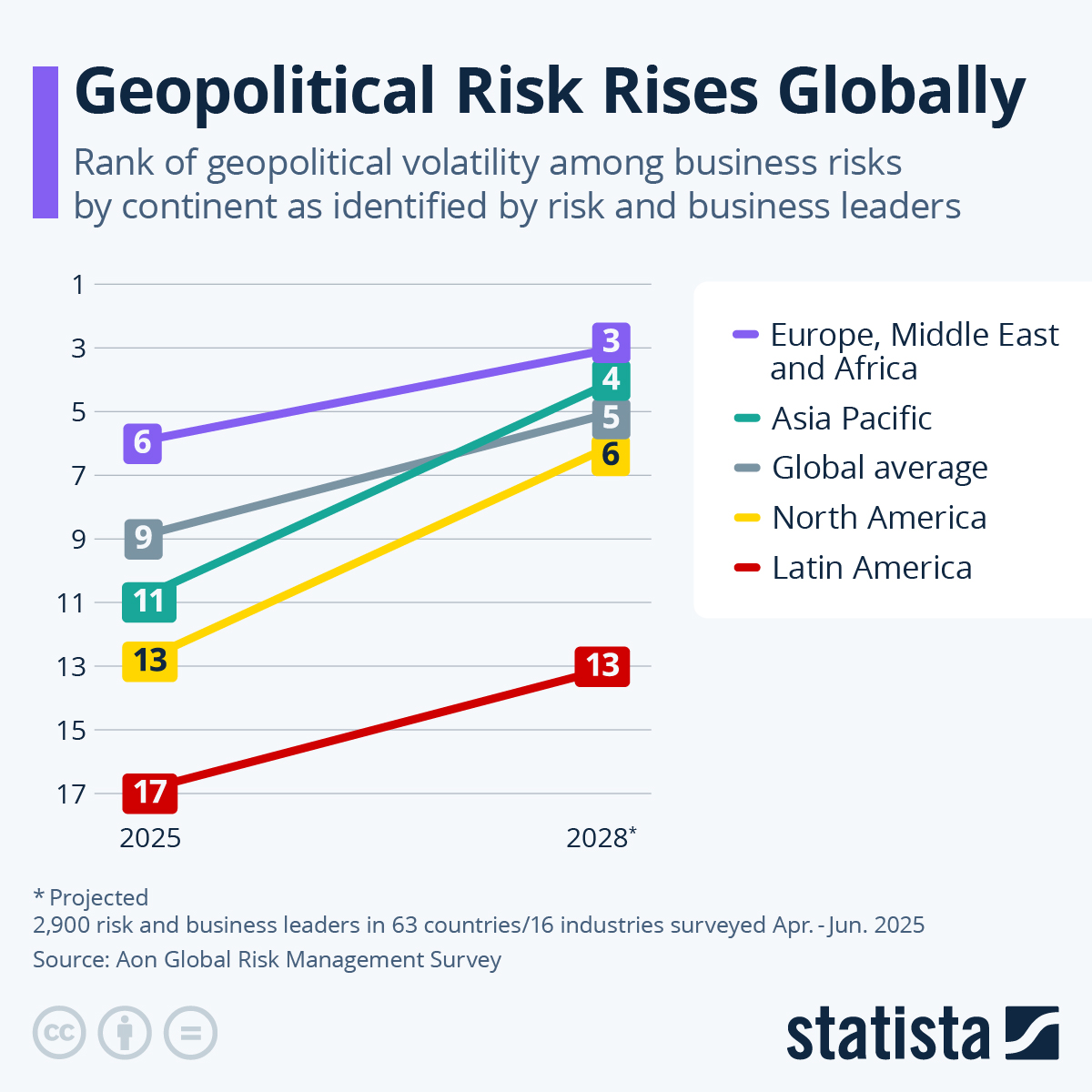

The Geopolitical Risk Premium and Corporate Earnings

The initial spike in the DAX, mirroring similar movements across European indices, was predicated on reports – originating from Egyptian sources and amplified by Reuters [Reuters Report on Ceasefire Talks] – of progress in negotiations for a ceasefire in Gaza. However, these reports lacked definitive confirmation, and the market quickly recalibrated as skepticism mounted. This illustrates a critical point: markets are currently pricing in a significant “geopolitical risk premium,” meaning valuations are heavily influenced by perceived threats to global stability. The problem isn’t simply the immediate market reaction; it’s the cascading effect on corporate planning. Companies are delaying capital expenditures, re-evaluating sourcing strategies, and bracing for potential disruptions. This uncertainty necessitates sophisticated financial modeling and scenario planning, areas where specialized financial modeling and risk analysis firms are seeing a surge in demand. The cost of inaction – misjudging the duration or severity of geopolitical instability – far outweighs the investment in proactive risk mitigation.

Supply Chain Resilience Under Scrutiny

The DAX’s composition – heavily weighted towards industrial giants like Volkswagen, Siemens, and BASF – makes it particularly vulnerable to supply chain disruptions. The Red Sea crisis, ongoing since late 2023, has already added significant costs and delays to shipments between Asia, and Europe. According to the Kiel Institute for the World Economy’s Global Supply Chain Monitor [Kiel Institute Supply Chain Monitor], shipping costs have increased by over 20% since January, and delivery times have extended by an average of 15 days. This isn’t a temporary blip. The trend towards “friend-shoring” and diversification of supply chains – while strategically sound in the long term – requires substantial upfront investment and logistical complexity. Companies are actively seeking partners to navigate these challenges, turning to supply chain consulting and logistics providers to optimize their networks and build resilience. The focus is shifting from simply minimizing costs to maximizing reliability, even if it means accepting higher short-term expenses.

Inflationary Pressures and the ECB’s Dilemma

Beyond geopolitical risks, persistent inflationary pressures continue to weigh on investor sentiment. While Eurozone inflation has moderated from its peak of 10.6% in October 2022, it remains stubbornly above the European Central Bank’s (ECB) 2% target. The latest data, released on March 22nd, showed a headline inflation rate of 2.4%, with core inflation (excluding energy and food) at 3.1%. [ECB Monetary Policy Statement – March 2024] This complicates the ECB’s monetary policy stance. Further interest rate cuts are unlikely until there is clear evidence that inflation is sustainably converging towards the 2% target. This creates a challenging environment for businesses, as higher borrowing costs squeeze margins and dampen investment.

“We’re seeing a bifurcation in the market. Companies with strong balance sheets and pricing power are weathering the storm, while those heavily reliant on debt are facing significant headwinds. The key is to proactively manage liquidity and optimize capital structure.” – Dr. Klaus Schmidt, Head of European Equity Research, DWS Group (March 2024)

The need for robust financial restructuring and debt management is driving demand for specialized corporate restructuring and insolvency advisory services. Companies are proactively seeking to optimize their capital structures and prepare for potential economic downturns.

The DAX’s Technical Outlook and Q2 Expectations

From a technical perspective, the DAX’s failure to sustain gains above 23,000 points suggests a potential short-term correction. The 50-day moving average currently sits at around 17,800 points, providing a key support level. However, the underlying trend remains bullish, driven by Germany’s relatively strong economic fundamentals and the potential for a rebound in global demand. Looking ahead to the second quarter, earnings expectations are mixed. The automotive sector, in particular, faces headwinds from slowing demand in China and the ongoing transition to electric vehicles. However, the technology and healthcare sectors are expected to outperform, driven by innovation and demographic trends. The current environment demands a nuanced investment strategy, focusing on companies with strong fundamentals, resilient supply chains, and pricing power. It also underscores the importance of proactive risk management and access to expert financial advice.

The volatility we’re witnessing isn’t an anomaly; it’s the new normal. Navigating this complex landscape requires more than just market analysis – it demands a strategic partnership with vetted B2B providers who can deliver tangible solutions. Explore the World Today News Directory today to connect with leading firms in financial modeling, supply chain management, and corporate restructuring, and position your business for success in the quarters ahead.