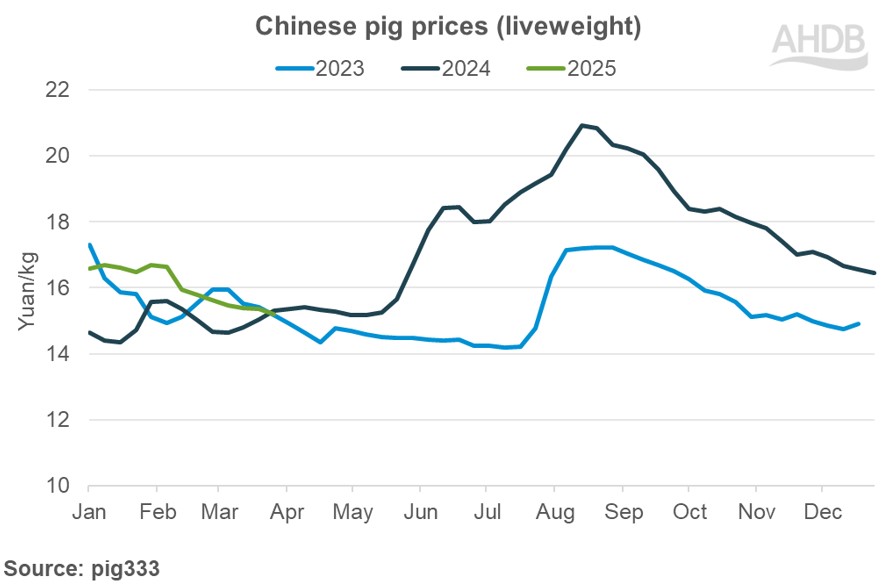

Chinese Pig Prices Hit 15-Year Low as Feed Costs Surge

Chinese live pig prices have collapsed to 10 yuan per kilogram, marking a 16-year low driven by severe oversupply and geopolitical feed cost surges. As the Iran conflict disrupts grain logistics, major agribusinesses face a liquidity crisis, forcing immediate capacity adjustments and defensive restructuring across the Asia-Pacific protein sector.

The numbers on the trading floor are brutal. We are witnessing a compression of margins that threatens to wipe out the equity value of mid-tier producers who leveraged up during the 2024 boom cycle. When the floor drops out of the protein market, the first casualty is working capital. Farmers are currently taking loans just to purchase feed, a classic sign of a distressed industry entering a liquidation phase. This isn’t just a cyclical downturn; it is a structural break in the supply chain economics of the world’s largest pork consumer.

The Geopolitical Squeeze on Feed Costs

The narrative coming out of Beijing is one of forced austerity. While domestic oversupply is the primary driver of the price crash, the secondary shockwave comes from the escalating conflict in the Middle East. Soybean and corn futures have spiked as logistics through the Strait of Hormuz face intermittent blockades, directly inflating the cost basis for Chinese hog farmers. This creates a fiscal pincer movement: revenue is at historic lows while input costs are at war-time highs.

According to data released by the National Bureau of Statistics of China, the average breeding sow inventory remains dangerously high, despite government pleas for output management. The Ministry of Agriculture and Rural Affairs has vowed timely reserve adjustments, but state intervention often lags behind market velocity. For the private equity firms holding stakes in these agri-giants, the EBITDA outlook for Q2 and Q3 2026 looks grim. The spread between live hog prices and feed costs has inverted, meaning every animal sold represents a net cash burn.

“We are seeing a classic distress signal where operational cash flow turns negative before balance sheet insolvency hits. The firms that survive this won’t be the biggest; they will be the ones with the most agile supply chain hedging strategies.”

This sentiment echoes the warnings from Marcus Thorne, Managing Partner at Apex Global Commodities, a firm that tracks agricultural derivatives. Thorne notes that the volatility in the hog futures curve suggests the market is pricing in a prolonged period of consolidation. “The 10-yuan mark is psychological, but financially, it’s the death knell for anyone without vertical integration,” Thorne stated during a recent investor briefing. “If you are buying feed on the spot market and selling hogs at 2026 lows, you are bleeding liquidity daily.”

Corporate Restructuring and the M&A Wave

As margins evaporate, the boardroom dynamic shifts from growth to survival. We expect a surge in distressed asset sales as larger conglomerates look to scoop up capacity at fire-sale prices. This environment creates a specific demand for specialized legal and financial counsel. Companies facing covenant breaches on their term loans will inevitably turn to corporate restructuring advisors to negotiate with creditors before triggering default clauses. The window for voluntary reorganization is closing swift as credit ratings agencies begin downgrading exposure to the Chinese agri-sector.

The pain is not isolated to the farms. It ripples up to the processors and exporters. WH Group, the world’s largest pork producer, has already signaled caution in its recent guidance, highlighting the need for rigorous cost control. For mid-market competitors who lack the balance sheet depth of the giants, the path forward involves aggressive operational pruning. This often requires engaging supply chain optimization firms to renegotiate logistics contracts and secure alternative feed sources outside the conflict zones.

- Liquidity Crunch: Farmers are leveraging personal loans for feed, indicating a breakdown in commercial credit lines.

- Inventory Glut: Breeding sow numbers remain 8% above the government’s green zone, delaying price recovery.

- Geopolitical Risk: The Iran conflict has added a 15% premium to imported soybean costs, eroding gross margins.

The Road to Recovery: A B2B Perspective

Recovery in this sector will not be V-shaped. It will be a grind. The market needs to see a significant culling of the breeding herd—estimates suggest a 10% reduction is necessary to stabilize prices above the cost of production. Until then, cash preservation is the only strategy that matters. For international investors looking at this space, the opportunity lies in the distress. Though, navigating the regulatory landscape of Chinese bankruptcy law requires local expertise.

Smart capital is already positioning itself. We are seeing increased activity from hedge funds specializing in distressed debt, looking to acquire non-performing loans tied to agricultural assets. For the companies trying to stay afloat, the focus must shift to efficiency. This is where the value of M&A advisory firms becomes critical. Consolidation is inevitable. Smaller players will be absorbed, and the transaction volume in the agri-food sector is poised to spike in the second half of 2026 as weak hands are forced to the exit.

The lesson for the broader market is clear: geopolitical instability acts as a multiplier for cyclical downturns. When the baseline economics of a commodity break, the ancillary service providers become the lifeline. Whether it is securing alternative grain logistics or restructuring debt obligations, the firms that facilitate these pivots will define the next cycle of the global food economy. As we move into the second quarter, watch the credit spreads on agri-bonds; they will tell you who survives and who gets liquidated.