Cheap Currencies: Beyond the Japanese Yen | FX Outlook

The Economist’s Big Mac Index for early 2026 signals a critical undervaluation in Asian currencies, specifically the Japanese Yen and Chinese Yuan, creating immediate arbitrage risks for multinational corporations. This purchasing power parity (PPP) divergence suggests Asian assets are trading at historic discounts relative to the US Dollar, forcing CFOs to reassess treasury hedging strategies and supply chain cost bases before Q2 earnings reports.

It isn’t just Japan. The latest iteration of the Big Mac Index, often dismissed as “burgernomics” by retail traders but scrutinized heavily by institutional desks, is flashing a red warning light across the Pacific Rim. While Western markets obsess over the Federal Reserve’s pivot on interest rates, a silent currency crisis is brewing in Asia. The Yen remains deeply undervalued against the greenback, but the ripple effect has dragged neighboring currencies into a deflationary spiral that threatens to erode the EBITDA margins of any US-based firm with significant exposure to Asian manufacturing.

This isn’t theoretical. When a currency trades 40% below its PPP fair value, it distorts global pricing models. For the unprepared corporate treasurer, this looks like a bargain. for the seasoned analyst, it looks like a liquidity trap waiting to snap shut. The disparity indicates that capital is fleeing Asian markets faster than local central banks can intervene, creating a volatility environment where standard hedging instruments may fail.

The Arbitrage Trap and Supply Chain Realities

Corporate giants relying on Asian supply chains are currently seeing inflated top-line revenue numbers that mask underlying margin compression. A cheaper Yen makes Japanese exports attractive, yes, but it also increases the cost of imported raw materials for factories located in Osaka or Tokyo. This input cost inflation is being passed down the line. We are seeing a decoupling between consumer price indices and wholesale producer prices, a classic sign of supply-side stress.

According to the European Central Bank’s December 2025 Monetary Policy Statement, the divergence in global purchasing power has reached levels unseen since the 2008 financial crisis. The ECB noted that while the Eurozone stabilizes, the Asian bloc is absorbing disproportionate shock from energy commodity fluctuations, exacerbating the currency weakness.

Mid-market manufacturers are scrambling to lock in rates before the volatility spikes further. This has led to a surge in demand for specialized treasury management and forex hedging firms capable of structuring complex derivative products that protect against asymmetric downside risk. Standard forward contracts are no longer sufficient when the basis points swing this wildly.

“We are witnessing a structural break in Asian currency valuation. This isn’t a cyclical dip; it’s a fundamental repricing of risk. Companies that don’t have a dedicated financial risk consulting partner reviewing their exposure weekly are essentially gambling with shareholder capital.”

— Marcus Thorne, Chief Investment Officer, Apex Global Macro Fund

Three Critical Shifts for the Fiscal Year

The implications of this “Asian Warning” extend beyond simple currency conversion. It fundamentally alters the competitive landscape for the upcoming fiscal quarters. We are moving from a period of stability to one of aggressive repositioning. Here is how the macro environment shifts for Q2 and Q3 2026:

- Aggressive M&A Activity: Undervalued Asian assets become prime targets for Western private equity. We expect a wave of hostile takeovers or distressed asset sales as local liquidity dries up. Companies need to engage M&A advisory firms immediately to identify defensive buyout opportunities or to prepare for acquisition.

- Supply Chain Re-shoring Acceleration: The cost benefit of manufacturing in Asia is evaporating when factored against currency volatility and logistics insurance premiums. CFOs are running new models that favor near-shoring to Mexico or Eastern Europe, requiring immediate supply chain logistics overhauls.

- Tax Efficiency Restructuring: Transfer pricing models built on 2024 exchange rates are now obsolete and potentially non-compliant. Multinationals must consult with international tax law experts to adjust inter-company pricing before the next audit cycle begins.

The Data: Where the Margins Are Bleeding

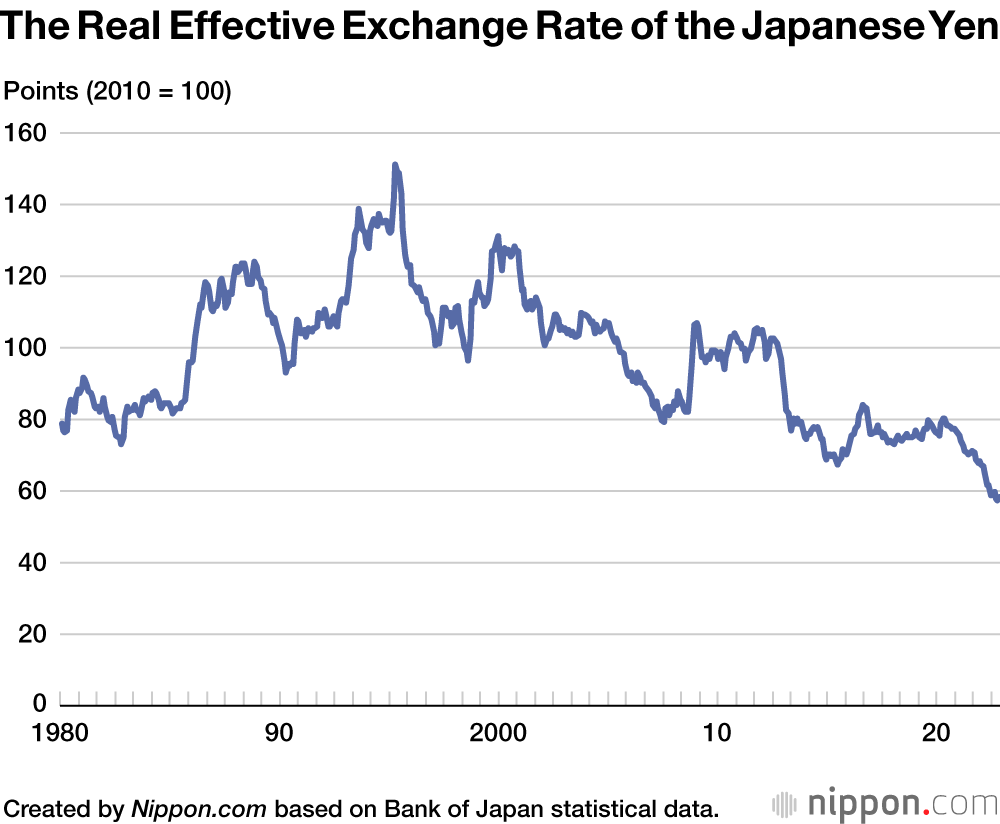

To understand the severity, one must look at the implied PPP versus the actual market rate. The gap has widened to over 35% for the Yen and nearly 28% for the Yuan. In practical terms, a Big Mac in Tokyo costs significantly less in dollar terms than in New York, but the local wage pressure and energy costs in Japan have risen by 12% year-over-year. This squeeze is unsustainable.

Consider the impact on a hypothetical US tech firm with 40% of its COGS (Cost of Goods Sold) denominated in JPY. If the Yen weakens another 5% against the Dollar due to Bank of Japan policy inertia, that firm’s gross margin could contract by 200 basis points overnight. Here’s not a risk that can be absorbed; it must be hedged.

| Metric | Q4 2025 Actual | Q1 2026 Forecast | Impact on USD-Based Firms |

|---|---|---|---|

| USD/JPY Exchange Rate | 158.40 | 165.00 (Projected) | Increased import costs for Japanese components |

| Asian Manufacturing PMI | 48.2 (Contraction) | 47.5 (Deepening Contraction) | Supply chain delays and inventory bottlenecks |

| Energy Import Cost (Asia) | +8.5% YoY | +14.2% YoY | Margin compression for local suppliers |

The data paints a grim picture for passive investors. The “cheap” currency narrative is a value trap. As the Bank of Japan continues its sluggish normalization of yield curves, the volatility will only increase. We are seeing a flight to quality, where capital leaves emerging Asian markets for the safety of US Treasuries, further depressing Asian currency values.

Strategic Imperatives for the Boardroom

The boardroom conversation has shifted from “growth at all costs” to “capital preservation.” In this environment, agility is the only currency that matters. Firms that can pivot their supply chains or restructure their debt obligations in local currencies will survive. Those that remain static will spot their valuations punished by the market.

This proves crucial to note that this isn’t just about currencies; it is about the cost of capital. As Asian rates remain suppressed while US rates hold steady, the carry trade becomes dangerous. Institutional investors are pulling back on exposure to Asian equities, preferring domestic plays with clear regulatory frameworks. This capital flight creates a vacuum that only sophisticated corporate restructuring experts can navigate effectively.

The window to act is closing. By the time Q2 earnings calls begin in April 2026, the market will have priced in these currency shifts. The companies that thrive will be those that treated the Big Mac Index not as a novelty, but as a leading indicator of a massive macroeconomic dislocation. The warning has been issued. The question now is whether your balance sheet is ready for the impact.