Estate Planning 101 for Blended Families

As aging parents enter new romantic relationships, the intersection of personal life and intergenerational wealth transfer creates significant fiscal risk for family estates. Proactive communication and formal legal restructuring are essential to prevent unintended asset dilution, ensuring that legacy planning remains insulated from the complexities of new spousal claims or cohabitation liabilities.

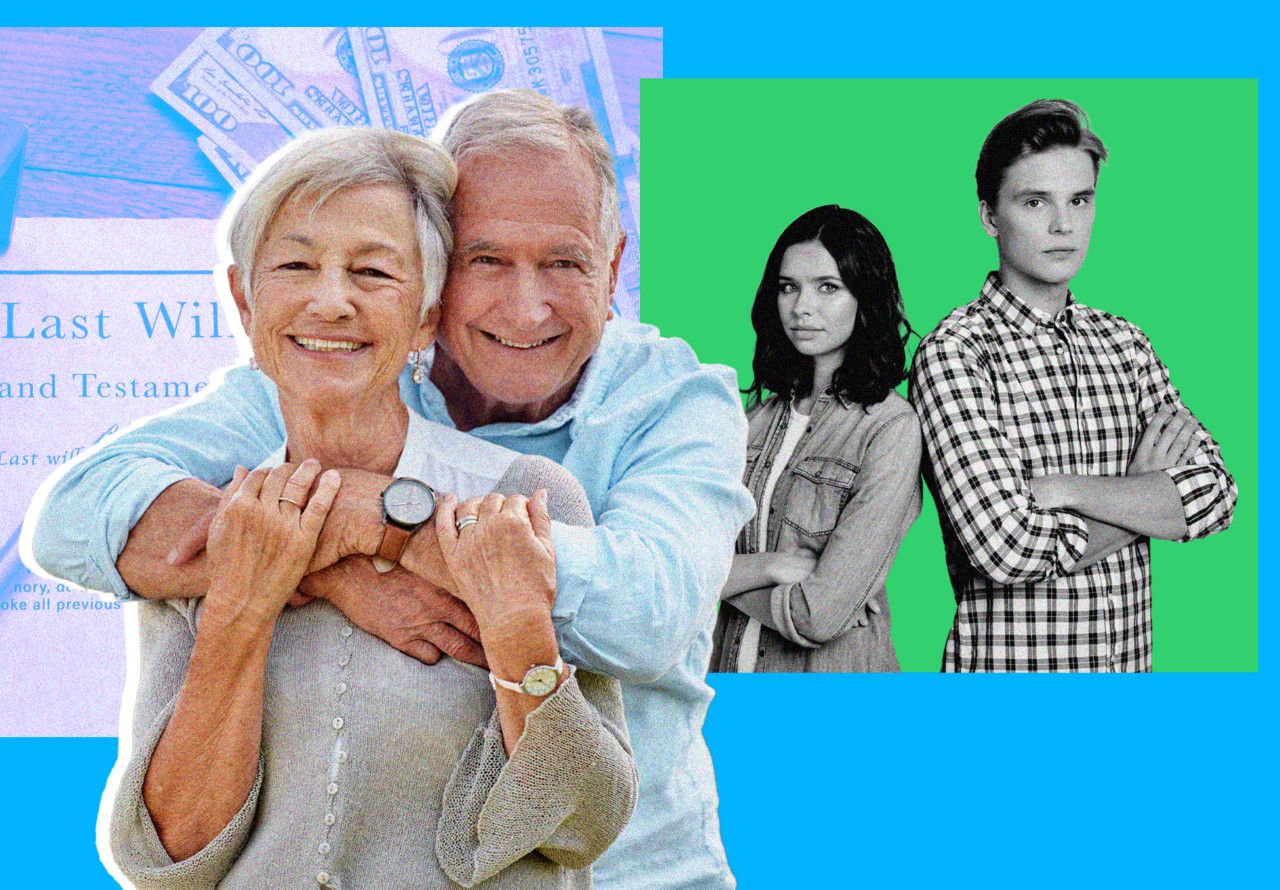

The Fiscal Risk of Unplanned Nuptials

When an aging parent remarries, the legal landscape of their estate shifts immediately. According to the American Bar Association’s Section of Real Property, Trust and Estate Law, marriage often triggers statutory rights—such as elective share laws—that can override existing estate plans. These laws may grant a new spouse a mandatory portion of the estate, regardless of what is written in a will or trust.

This creates a liquidity event for the heirs. If the estate’s assets are illiquid—such as family-owned real estate or private equity holdings—a court-mandated payout to a new spouse can force a fire sale of assets to generate the necessary cash. To mitigate these risks, high-net-worth families frequently engage [Top-Tier Estate Planning Law Firms] to draft prenuptial agreements or implement irrevocable trusts that ring-fence legacy assets from future claims.

Quantifying the Impact on Asset Preservation

The financial stakes are high. Data from the IRS Statistics of Income Division shows that estate tax returns involving complex, multi-layered beneficiary structures require precise coordination to avoid adverse tax consequences. Without formal intervention, a parent’s new romance can inadvertently trigger a taxable event or disrupt the governance of a family office.

Investment professionals emphasize that the goal is not to control the parent’s personal life, but to manage the balance sheet. “The friction between personal autonomy and fiduciary responsibility is where most wealth erosion occurs,” notes Marcus Thorne, a senior wealth strategist at Sterling Global Capital. “Families that fail to formalize these boundaries early often find themselves in protracted probate litigation that consumes a significant percentage of the total estate value.”

Strategic Implementation of Protective Trusts

Trust structures provide the most robust defense against the dilution of inheritance. By moving assets into a discretionary trust, the parent maintains control while placing the assets outside the reach of a new spouse’s statutory claims. This requires a sophisticated understanding of current Investment Advisers Act regulations and tax codes.

When restructuring, it is vital to perform a comprehensive audit of all existing beneficiary designations. Many individuals forget to update life insurance policies or retirement accounts, which remain tied to the primary account holder regardless of their will. Engaging [Independent Wealth Management Consultants] ensures that these administrative details are aligned with the broader estate strategy.

Why Preemptive Documentation Matters

Transparency is the primary defense against the perception of greed. When children initiate conversations about estate planning, framing the discussion around administrative efficiency and tax optimization—rather than the parent’s relationship—softens the dynamic. According to the Trusts & Estates industry publication, the highest success rates for asset preservation occur when these conversations happen well before the date of a wedding.

The core issue is volatility. Relationships introduce unpredictable variables into a long-term financial plan. By addressing these variables through legal instruments, heirs protect the principal, while the parent continues to manage their income flow without interference. Consider the following structural adjustments to protect the portfolio:

- Prenuptial Agreements: Defining the separation of pre-marital assets as non-marital property.

- Irrevocable Trusts: Removing assets from the taxable estate and shielding them from future spousal claims.

- Governance Charters: Establishing clear guidelines for how family businesses or assets are managed during and after a transition.

As the market cycle shifts and liquidity becomes more expensive, the cost of failing to plan grows exponentially. Protecting the integrity of a multi-generational legacy requires more than sentiment; it requires professional intervention. Families should prioritize consulting with [Fiduciary Advisory Services] to ensure that their current estate architecture can withstand the pressures of shifting family dynamics in the coming fiscal quarters.