As 2025 draws to a close, millions of Americans enrolled in Affordable Care Act (ACA) Marketplace plans are facing a critical decision: pay higher monthly premiums or accept plans with substantially higher deductibles. This challenging choice stems from the impending expiration of enhanced premium tax credits, a temporary measure implemented to make health insurance more affordable during the pandemic. A recent analysis by the Health System Tracker highlights the potential financial implications of these tradeoffs, urging enrollees to carefully consider thier healthcare needs when selecting a plan for 2026.

The Looming End of Enhanced Tax Credits

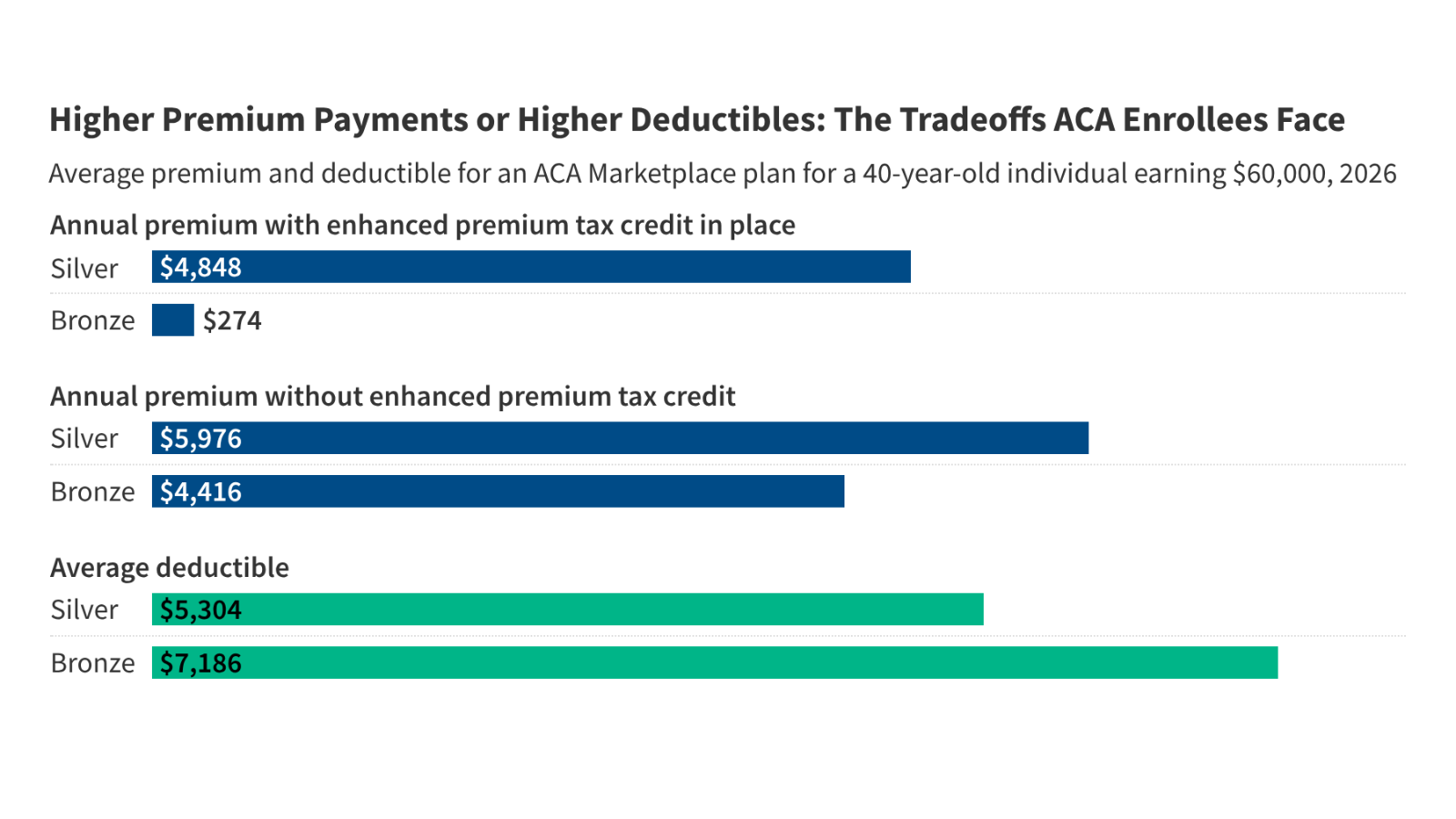

The American Rescue Plan Act of 2021 temporarily increased the size of premium tax credits, making health insurance more accessible for a wider range of income levels. These enhanced credits were extended through 2025, but without further congressional action, they are set to expire. This expiration will disproportionately impact those who currently receive substantial financial assistance, potentially leading to significant premium increases.

According to the Kaiser Family Foundation (KFF), approximately 85% of ACA Marketplace enrollees receive premium tax credits. The loss of these credits could price many individuals and families out of the market, or force them to choose less comprehensive coverage.

Silver vs. Bronze: Understanding the Tradeoffs

Faced with rising premiums, many enrollees are considering switching from “Silver” plans to “Bronze” plans. Bronze plans generally have the lowest monthly premiums but come with higher deductibles, copayments, and coinsurance. While a lower premium might seem attractive upfront, it’s crucial to understand the potential financial burden if you require significant medical care.

Here’s a breakdown of the key differences:

- Silver Plans: Offer a balance between premiums and out-of-pocket costs. They also qualify for “cost-sharing reductions” for individuals with lower incomes, further reducing deductibles and copays.

- Bronze Plans: Have the lowest premiums but the highest out-of-pocket costs. They do not qualify for cost-sharing reductions.

The Health System Tracker analysis emphasizes that switching to a Bronze plan isn’t always the best financial move. Individuals who frequently use healthcare services – those with chronic conditions,such as – could end up paying more overall due to the higher deductibles and cost-sharing.

The Impact of Cost-Sharing Reductions

Cost-sharing reductions (CSRs) are a vital component of the ACA, providing financial assistance to eligible individuals to lower their out-of-pocket costs. These reductions are only available with Silver plans and are based on income level. The loss of CSRs when switching to a Bronze plan can significantly increase the financial burden of healthcare.

For example, someone eligible for a high level of CSRs in a Silver plan might have a deductible of just a few hundred dollars. The same individual in a Bronze plan could face a deductible of several thousand dollars.

Navigating Open Enrollment and Making the Right Choice

The ACA Marketplace Open Enrollment period typically runs from November 1st to January 15th in most states. During this time, individuals can enroll in or change their health insurance plans. It’s crucial to carefully evaluate your options and consider your healthcare needs before making a decision.

Tips for Choosing a plan:

- Estimate Your Healthcare Usage: Consider how often you typically visit the doctor, fill prescriptions, or require other medical services.

- Calculate Potential Out-of-Pocket Costs: Factor in deductibles, copays, and coinsurance when comparing plans.

- Check if You Qualify for Cost-Sharing Reductions: If you have a low income, explore Silver plans to see if you’re eligible for CSRs.

- Use the healthcare.gov Plan Finder: Healthcare.gov offers a plan finder tool that can help you compare plans and estimate your costs.

- Seek Assistance from a Navigator or Broker: Local navigators and brokers can provide free, unbiased assistance with the enrollment process.

Looking Ahead: Potential Policy Changes

The expiration of the enhanced premium tax credits is a significant concern for many ACA enrollees.Congress could take action to extend or make permanent these credits, mitigating the potential for premium increases. Though, the political landscape remains uncertain.

The future of the ACA and its affordability will likely be a key issue in upcoming policy debates. Ongoing monitoring of legislative developments and enrollment trends will be crucial to understanding the long-term impact of these changes.

Key Takeaways

- Enhanced premium tax credits are set to expire at the end of 2025, potentially leading to higher premiums for ACA Marketplace enrollees.

- Switching from a Silver plan to a Bronze plan can lower premiums but may result in higher out-of-pocket costs, especially for those who frequently use healthcare services.

- Cost-sharing reductions are only available with Silver plans and can significantly reduce out-of-pocket costs for eligible individuals.

- Carefully evaluate your healthcare needs and compare plans during Open Enrollment to make the best choice for your situation.

The Peterson-KFF Health System Tracker remains a valuable resource for staying informed about health policy and healthcare costs: Peterson-KFF Health System Tracker.