The Importance of Thorough Financial Planning

What does effective financial planning truly entail? It begins with a clear understanding of a family’s needs and goals throughout its entire lifecycle – from securing a home and protecting against risks, too supplemental pension planning and funding children’s higher education. It extends to realizing both small and critically important aspirations, such as purchasing a second home. Crucially, this planning must be aligned with one’s savings capacity, based on current and projected income and expenses. it involves identifying the most efficient solutions to address these diverse needs, recognizing that the plan will require periodic adjustments as circumstances change and initial assumptions evolve.

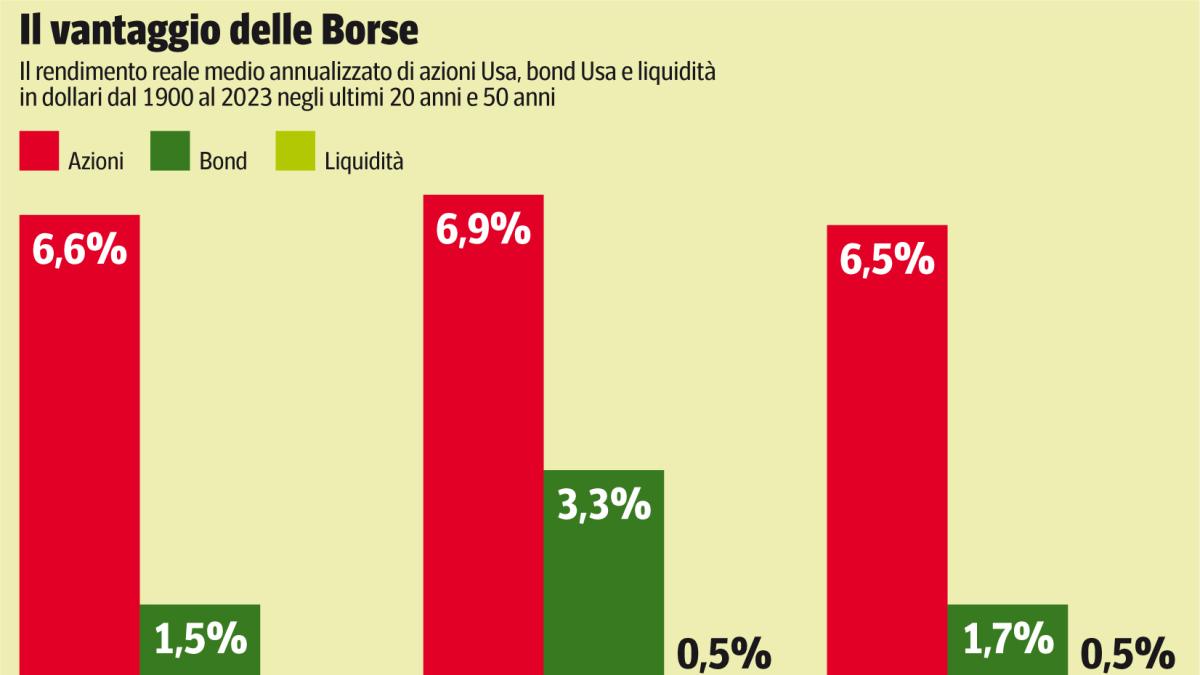

As highlighted in a recent analysis by Corriere Economia, with support from Progetica, understanding these principles is vital for navigating financial complexities.The analysis examined three distinct scenarios: a 35-year-old single individual, a family of four consisting of two 40-year-old parents and two children, and a couple aged 55 with no heirs. this case study illustrates the tailored approach necessary for each situation.

Key Components of a Robust Financial Plan

A well-structured financial plan isn’t a static document; it’s a dynamic roadmap that adapts to life’s changes. Here’s a breakdown of the core elements:

- Needs Assessment: Identifying both short-term and long-term financial needs. This includes essential expenses like housing, healthcare, and education, and also aspirational goals like travel or early retirement.

- Goal Setting: Defining specific,measurable,achievable,relevant,and time-bound (SMART) financial goals. for example, rather of “save for retirement,” a SMART goal would be “save €500 per month for 30 years to accumulate a retirement fund of €300,000.”

- Budgeting and Cash Flow Management: Tracking income and expenses to understand where money is going and identify areas for potential savings. Utilizing budgeting tools and apps can streamline this process.

- Debt Management: Developing a strategy to manage and reduce debt, prioritizing high-interest debts like credit cards.

- Investment Planning: Creating a diversified investment portfolio aligned with risk tolerance and financial goals. This may include stocks, bonds, mutual funds, and real estate.

- Risk Management: Protecting against unforeseen events through insurance (life, health, property, disability).

- Retirement Planning: Estimating retirement income needs and developing a plan to accumulate sufficient savings.

- Estate Planning: preparing for the transfer of assets upon death, including wills, trusts, and power of attorney.

Financial Planning for Different Life Stages

financial planning needs evolve as individuals and families progress through different life stages. Here’s how the approach might differ:

Young Adults (20s & 30s)

Focus: Building a financial foundation. Prioritize paying off student loans, establishing an emergency fund (3-6 months of living expenses), and starting to invest for retirement, even with small amounts.taking advantage of employer-sponsored retirement plans with matching contributions is crucial. Consider early career investments in skill development to increase earning potential.

families with Young Children (40s & 50s)

Focus: Balancing current expenses with long-term goals. This stage often involves significant expenses like childcare, education, and a mortgage. Prioritize saving for college, increasing retirement contributions, and ensuring adequate life and disability insurance.Regularly review and adjust the financial plan to accommodate changing family needs.

Pre-Retirees & Retirees (55+)

Focus: Preserving and growing wealth for retirement. Shift investment strategy towards a more conservative approach to protect accumulated savings. Develop a retirement income plan to ensure a lasting income stream. Consider long-term care insurance and estate planning.

The Role of Professional Financial Advice

While self-directed financial planning is possible, seeking guidance from a qualified financial advisor can be invaluable. A financial advisor can provide:

- Objective Advice: An unbiased outlook on your financial situation.

- Expertise: Knowledge of complex financial products and strategies.

- Personalized Planning: A customized plan tailored to your specific needs and goals.

- Ongoing Support: Regular reviews and adjustments to the plan as your circumstances change.

When choosing a financial advisor, look for credentials such as Certified Financial Planner (CFP) and ensure they are a fiduciary, meaning they are legally obligated to act in your best interest.

Adapting to Change: The Importance of Plan Review

Life is unpredictable. Changes in income, employment, family status, or market conditions can all impact a financial plan. It’s essential to review and adjust the plan at least annually, or more frequently if significant life events occur. This ensures the plan remains aligned with your goals and continues to provide a clear path to financial security.

Published: 2024/01/11 18:01:35