Arkisys (in partnership with Odin Space) is now at the center of a structural shift involving space‑debris risk and commercial insurance. The immediate implication is the creation of a price‑signal mechanism that can lower entry barriers for on‑orbit logistics and enable a broader in‑space circular economy.

The strategic Context

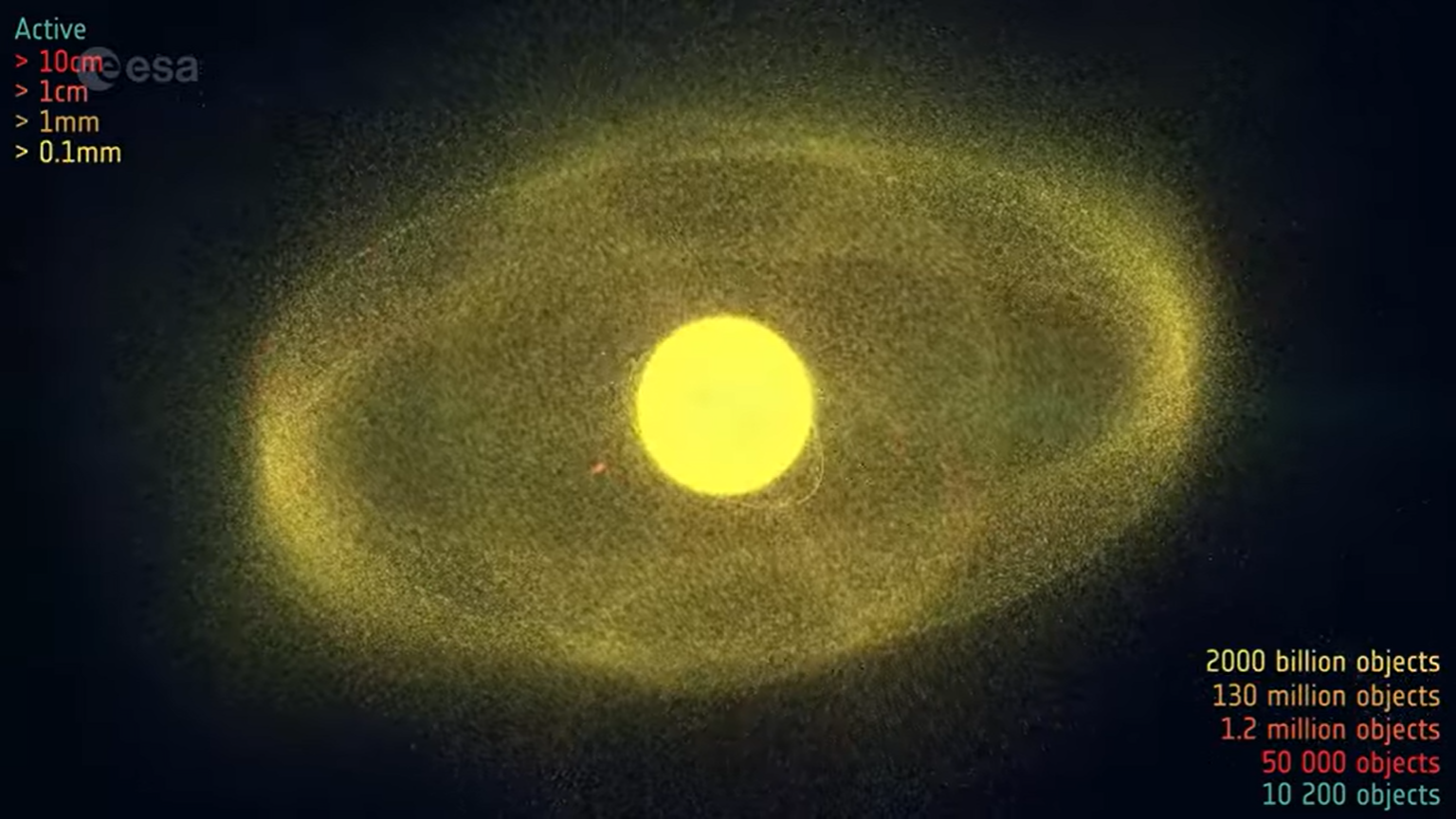

Over the past decade, low‑Earth orbit (LEO) has transitioned from a government‑dominated arena to a densely populated commercial ecosystem. The launch of mega‑constellations, on‑orbit servicing platforms, and “last‑mile” delivery concepts has multiplied the number of active assets while the orbital debris population-especially sub‑centimeter fragments-has grown faster than tracking capabilities. Conventional space‑insurance products bundle mission‑wide coverage and satellite replacement, resulting in high premiums that deter smaller operators. Together, the insurance market lacks granular data to price collision risk on a per‑event basis, creating a feedback loop that inflates costs and slows market entry.

Core analysis: Incentives & Constraints

Source Signals: The source confirms that arkisys and Odin Space are launching a joint offering of collision‑specific insurance backed by Odin’s nano‑sensor “black‑box” technology, which can detect and timestamp sub‑centimeter debris impacts. Arkisys plans to use the sensors on its Cutter mission, a “last‑mile” transport vehicle for delivering payloads to its Port modules. Odin Space has recently secured $3 million in seed funding to expand its debris‑tracking sensors and scout satellites.

WTN Interpretation: The partnership leverages two complementary assets: Arkisys’ emerging on‑orbit logistics platform and Odin’s data‑rich debris detection capability. By providing verifiable impact evidence, the insurers can underwrite narrowly scoped collision policies, reducing premium levels and aligning risk pricing with actual exposure.This addresses a structural market inefficiency-facts asymmetry-by turning previously unobservable micro‑debris events into insurable data points.Arkisys gains a competitive edge in attracting cost‑sensitive customers, while Odin secures a commercial pathway for its sensor technology, justifying its recent funding round. Constraints include the nascent regulatory environment for on‑orbit services,the technical challenge of scaling sensor deployment across diverse platforms,and the limited past loss data for sub‑centimeter debris,which may temper insurer appetite until sufficient claim experience accrues.

WTN Strategic Insight

“Transforming invisible micro‑debris into quantifiable insurance risk is the first step toward a self‑regulating commercial orbital economy.”

Future Outlook: Scenario Paths & Key Indicators

Baseline Path: If the sensor data proves reliable and insurers adopt the collision‑specific model, premiums for on‑orbit logistics will decline, spurring a wave of new entrants into LEO services. This will accelerate the growth of a modular, reusable orbital infrastructure and increase capital flows into ancillary technologies such as autonomous docking and in‑space manufacturing.

Risk Path: If sensor performance is questioned or a high‑profile debris‑induced loss occurs without clear attribution, insurers may revert to broader, higher‑cost policies, preserving the premium barrier.Coupled with potential regulatory tightening on on‑orbit activities, this could slow market entry and concentrate capabilities among a few well‑capitalized players.

- Indicator 1: Publication of the first verified collision claim under the new policy (expected within 3‑4 months of Cutter’s launch).

- Indicator 2: Regulatory filings or guidance from national space agencies concerning on‑orbit insurance standards (anticipated in the next 6 months).