HELOCs Fuel Rise in Serious Mortgage Delinquencies and Foreclosures in Q3 2025

washington D.C. – A surge in Home Equity Line of Credit (HELOC) delinquencies is contributing to a broader uptick in serious mortgage delinquencies and foreclosures, according to new data released today. While overall foreclosure rates remain historically low, the trend signals a potential shift as pandemic-era protections expire and household finances are increasingly strained by persistent inflation and rising interest rates.

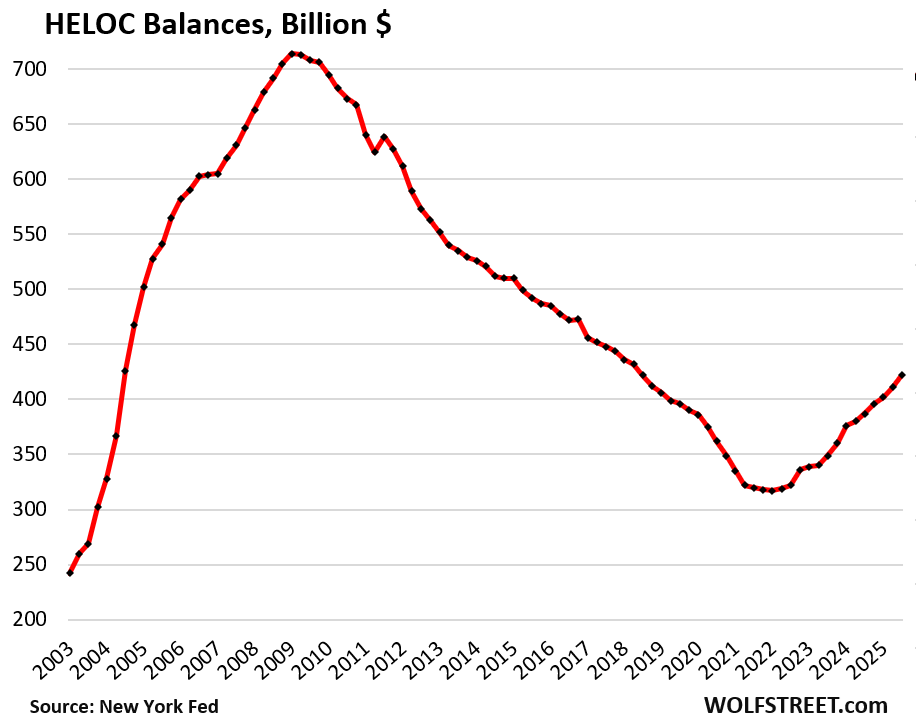

The data reveals that 66,000 U.S. homes were in some stage of foreclosure in Q3 2025, a 12% increase from the prior quarter.Serious delinquencies (90+ days late or in foreclosure) rose to 2.2% of all mortgages, up from 1.8% in Q2 2025. Notably, HELOC delinquencies are climbing faster than first-lien mortgages, indicating borrowers are tapping into home equity and later struggling to keep up with payments. This rise in delinquencies and foreclosures, while still below pre-pandemic levels, represents a meaningful departure from the artificially suppressed numbers seen during the height of mortgage forbearance programs.

The increase in delinquencies and foreclosures is particularly pronounced among borrowers with high debt-to-income (DTI) ratios. The average DTI for mortgage holders rose to 41.6% in Q3 2025, further squeezing household budgets. The data also shows a concentration of rising delinquencies in certain metropolitan areas, suggesting regional economic vulnerabilities are playing a role.

Foreclosure completions in Q3 2025 totaled 20,000, remaining within the 20,000-to-90,000 range observed in 2018-2019, and significantly below the levels seen in prior years. Analysts describe the recent foreclosure trajectory as forming a “frying-pan pattern” - a sharp drop to near-zero during the pandemic followed by a gradual increase as restrictions lifted. This pattern is also visible in broader delinquency charts.

The situation warrants close monitoring as the full impact of rising interest rates and economic uncertainty unfolds. Further increases in HELOC delinquencies and overall mortgage distress could put downward pressure on housing prices and contribute to broader financial instability.