Okay, hereS a breakdown of the key takeaways from the provided text, focusing on the implications of recent and upcoming changes to the Affordable Care Act (ACA) Marketplace, notably concerning consumer impact:

1. Premium Increases & Subsidy Changes (2026):

* Significant Premium Hikes: Without the extension of enhanced premium tax credits, premiums for Marketplace enrollees are projected to more than double in 2026.

* Subsidy Loss: Individuals with incomes above 400% of the Federal Poverty Level (FPL) will lose premium tax credits, making coverage much more expensive. This could lead some to leave the Marketplace altogether.

* Plan Switching: To cope with higher costs, some consumers may opt for plans with higher deductibles.

2. HSA Expansion & Impact:

* Increased HSA Eligibility: A larger percentage of Marketplace plans (35% in 2026 vs. 4% in 2025) will be Health savings Account (HSA)-eligible, including all Bronze and Catastrophic plans.

* HSA Benefits: HSAs offer tax advantages (tax-deductible contributions, tax-free withdrawals for qualified medical expenses, tax-free growth).

* Income Disparity: Higher-income individuals are more likely to be able to contribute considerably to HSAs due to greater disposable income and higher tax brackets, maximizing the tax benefits.

* Marketing Concerns: Expansion of HSA eligibility to off-Marketplace plans may incentivize HSA vendors to market individual plans outside the Marketplace, possibly leading to confusion.

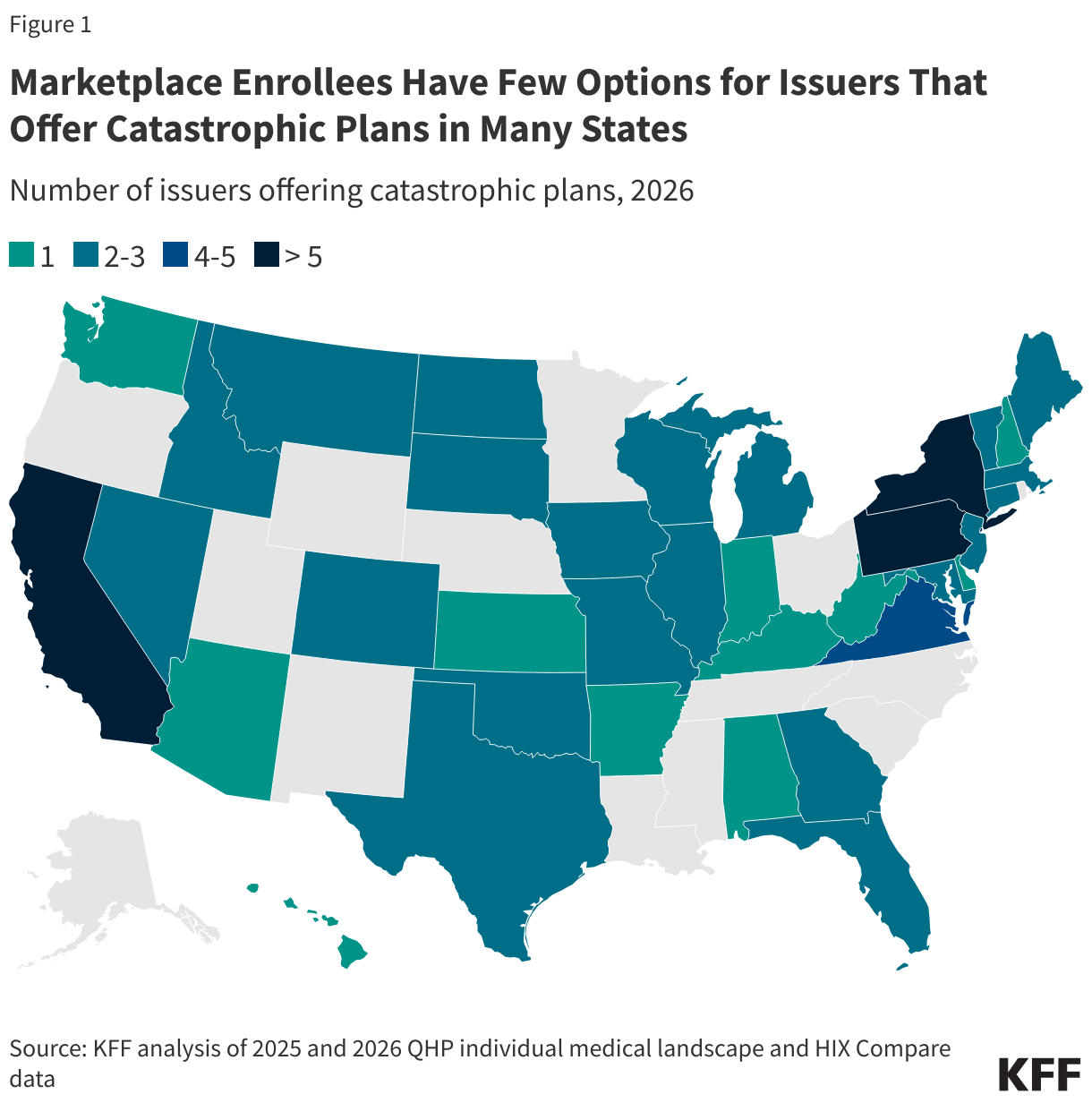

3. Catastrophic Plan Changes & Risk Pools:

* Expanded Hardship Exemptions: Easier access to hardship exemptions will likely increase enrollment in catastrophic plans.

* Increased Visibility: New display options on HealthCare.gov will make catastrophic plans more visible to shoppers.

* Risk Pool Concerns: If healthy individuals flock to catastrophic plans (or leave the Marketplace), the risk pools for metal-level plans (Bronze, Silver, Gold, Platinum) could become sicker, potentially driving up premiums for those plans.

* Separate risk Adjustment: catastrophic plans are in a separate risk pool for risk adjustment, meaning funds aren’t directly transferred between them and metal-level plans.

4. Consumer understanding & Challenges:

* Complexity: The health insurance system is already complex, and these changes add another layer.

* Lack of understanding: Many consumers struggle to understand health insurance concepts (cost-sharing, premiums, plan differences). A significant portion find it difficult to compare plans.

* Marketing Confusion: Consumers are bombarded with marketing from various sources, including off-Marketplace plans that can be difficult to distinguish from on-marketplace options. Off-Marketplace plans may not be ACA-compliant or offer tax credits.

* Limited Impartial Resources: There’s a lack of readily available, unbiased resources to help consumers navigate these choices.

5. Financial Burden & High Deductibles:

* Affordability Issues: Many Marketplace enrollees already struggle to afford out-of-pocket healthcare costs.

* High deductibles: Bronze and catastrophic plans have lower premiums but significantly higher deductibles.

* Cost-Sharing Reductions: These are only available on Silver plans, making them potentially more cost-effective for those who qualify.

* Financial Vulnerability: A ample percentage of U.S. adults lack the cash to cover even a moderate medical expense (e.g., $400), making high deductibles a significant risk.

data Sources & Methodology:

* The analysis uses data from CMS (Centers for Medicare & medicaid Services) and HIX Compare.

* Data is weighted by 2025 plan selections to reflect real-world enrollment patterns.

* Plan eligibility for HSAs is based on data from the plan attributes public use file (HealthCare.gov plans only).

In essence, the article paints a picture of a Marketplace facing potential instability due to policy changes. While some changes (like HSA expansion) offer benefits, they are likely to disproportionately benefit higher-income individuals. The biggest concern is the potential for significant premium increases and the challenges consumers will face in navigating a more complex and potentially less affordable system.